The Filecoin community celebrated the first anniversary of the Filecoin Virtual Machine (FVM) launch on March 14, 2024. The FVM has brought programmability to Filecoin’s verifiable storage and opened up a unique DeFi ecosystem anchored around improving on-chain collateral markets. Liquid Staking, for example, as a subset of Filecoin DeFi, has hit over $500 million in TVL. As the network grows, several critical infrastructures across AMMs, Bridges, Oracles, and Collateral Debt Positions (CDPs) are coming together to propel DeFi expansion in 2024.

In this blog post, let’s take a look at the latest DeFi projects launched on top of FVM and provide a view into future areas of activity.

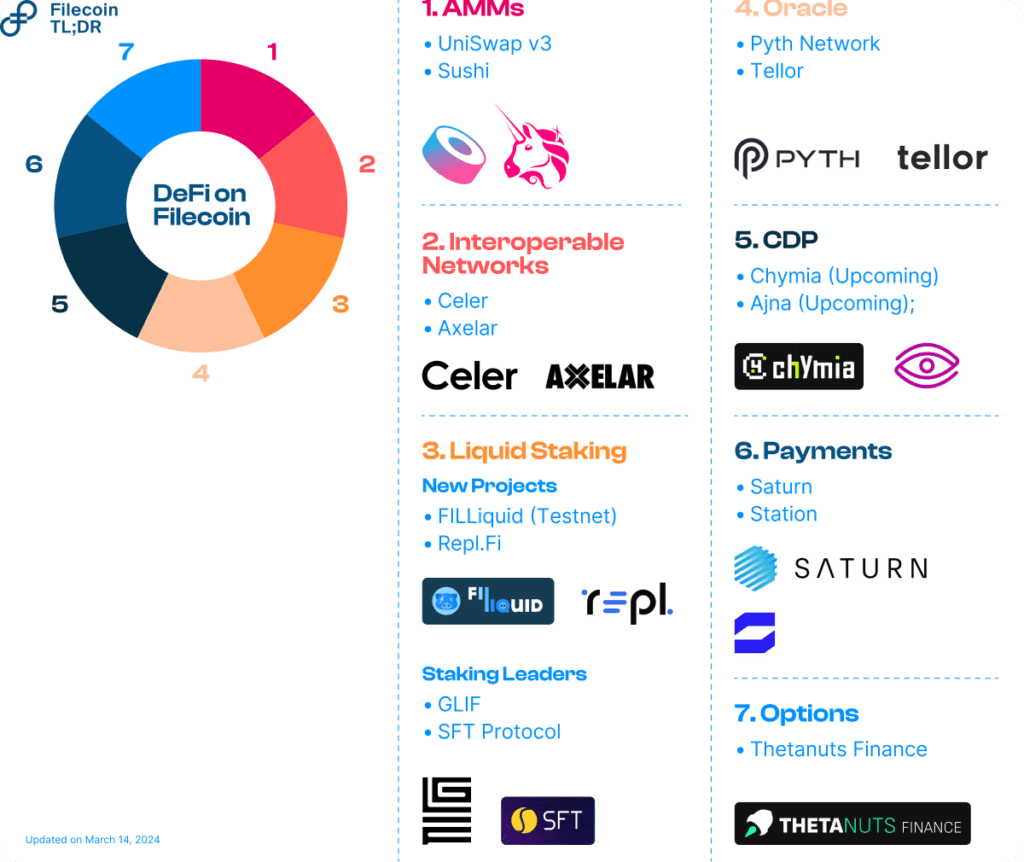

DeFi Developments on FVM

Automated Market Makers

Automated Market Makers (AMMs) connect Filecoin with other Web3 ecosystems, enabling on-chain swaps, deeper liquidity, and fresh LP opportunities.

Decentralized Exchanges: ✅

Recently, leading Decentralized Exchanges Uniswap v3 (via Oku.trade) and Sushi integrated with Filecoin by deploying on the FVM. Oku Trade’s interface enables Uniswap users to easily exchange assets and provide liquidity on Filecoin. With this, FVM developers can effortlessly access bridged USDC and ETH assets natively on the Filecoin network, broadening Filecoin’s reach. As a foundational DeFi primitive, DEXes also opens the floodgates for non-native applications to leverage Filecoin’s robust storage and compute hardware.

Interoperability Networks

Bridges: ✅

Bridges help bring liquidity into DEXs and AMMs on FVM. For developers building on FVM, Bridges connects Filecoin’s verifiable data with tokens, users, and applications on any chain, ensuring maximum composability for DeFi protocols. For this purpose, messaging, and token bridging solutions by Axelar and Celer were added to the Filecoin network immediately post-FVM launch.

Today, AMMs Uniswap v3 and Sushi along with several other DeFi applications are natively bridged to Filecoin with the help of cross-chain infrastructure enabled by Axelar and Celer.

Liquid Staking

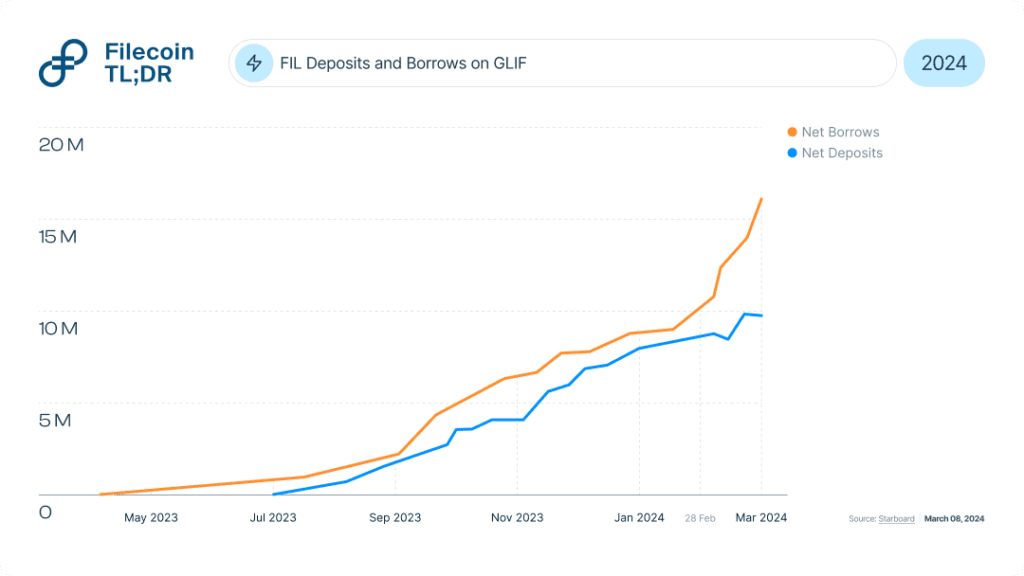

Liquid Staking protocols have been the prime mover within Filecoin DeFi. They’ve played a vital role in growing and improving on-chain collateral markets. Today, nearly 17% of the total locked collateral (approx. 30 million FIL) by storage providers comes from FVM-based protocols such as GLIF (52%), SFT Protocol (10%), Repl (9%) and the rest (29%). These protocols have increased capital access to storage providers while simultaneously enabling better yield access to token holders. Read more to learn how Filecoin staking works.

GLIF Points: 🔜

GLIF, the leading protocol on Filecoin, has a TVL of over $250 million. To put this into context, this surpasses the largest Liquid Staking protocols on L1 chains like Avalanche. As of writing this (March 06, 2024), 32% of all FIL stakes into GLIF liquidity pools were deposited shortly after its announcement to launch GLIF points (on Feb. 28, 2024), a likely precursor to a governance token.

Typically, to participate in the rewards program, GLIF users will have to deposit FIL and mint GLIF’s native token, iFIL. Similarly, the SFT protocollaunched a points program in 2023 based on its governance token to incentivize community participation.

Overall, we look forward to how the gameplay of points, popular among DApps in Web3 ecosystems, will act as a catalyst to decentralize governance and incentivize participation for Filecoin’s DeFi DApps.

New Staking Models: 👀

The influx of protocols experimenting with new models to inject liquidity into the ecosystem hasn’t slowed down. Two projects worth mentioning are Repl and FILLiquid.

Repl.fiintroduces the concept of “repledging.” Under repledging, SP’s pledged FIL are tokenized into pFIL, Repl’s native token, and used for other purposes including earning rewards. Repleding essentially increases the utility of locked assets thereby reducing opportunity costs for SPs. In just a few months after launch, Repl’s TVL has soared past $30 million.

FILLiquid, currently on testnet, models the business of FIL lending for SPs on algorithm-based fixed fees instead of traditional interest rates. The separation of payouts from the duration of deposits is expected to nudge long-term pledging and borrowing activities from token holders and SPs respectively, saving costs and increasing efficiency.

Price Oracles

Oracles, services that feed external data to smart contracts, are critical blockchain infrastructure essential for DeFi applications to grow and interact with the real world.

Pyth Network: ✅

Pyth recently launched its Price Feeds on the FVM. The integration allows FVM developers to access more than 400 real-time market data feeds while exploring opportunities to build on top of Filecoin’s storage layer. DeFi apps benefit from Pyth’s low-latency, high-fidelity financial data coming directly from global institutional participants such as exchanges, market makers, and trading firms.

Filecoin is also supported by Tellor, an optimistic oracle that gives FVM-based applications access to price feed data.

Collateralized Debt Positions

As DeFi activity on Filecoin is climbing, Collateralized Debt Positions (CDPs) will add more dimensions for other decentralized applications to build on FVM.

Chymia.Finance: 🔜

Chymia is an upcoming DeFi protocol on FVM. With a growing number of Liquid Staking Tokens (LST) on Filecoin, CDPs will extend the utility of locked tokens by generating stablecoins. Through Chymia, holders of LST can generate higher yields while using it as collateral for deeper liquidity.

Ajna: 🔜

Ajna is a noncustodial, peer-to-pool, permissionless lending, borrowing, and trading system requiring no governance or external price feed to function. As a result, any ERC20 on the FVM will be able to set up its own borrow or lend pools, making it easier for new developers to build a utility for their protocols.

Payments

Adjacent to storage offering on Filecoin, the FVM allows developers to bind DeFi payments to real-world primitives on the network. Built intuitively, Filecoin’s core economic flows enable paid services to settle on-chain. Station and Saturn are two notable Filecoin services to have successfully leveraged FVM for payments.

Filecoin Station: ✅

Station is a downloadable desktop application that uses idle computing resources on Station’s DePIN network to run small jobs. Participants in the network are rewarded with FIL earnings. Currently, Station operates the Spark and the Voyager modules, both aimed at improving retrievability on the network. In February, roughly 1,900 Station operators were rewarded with FIL for their participation.

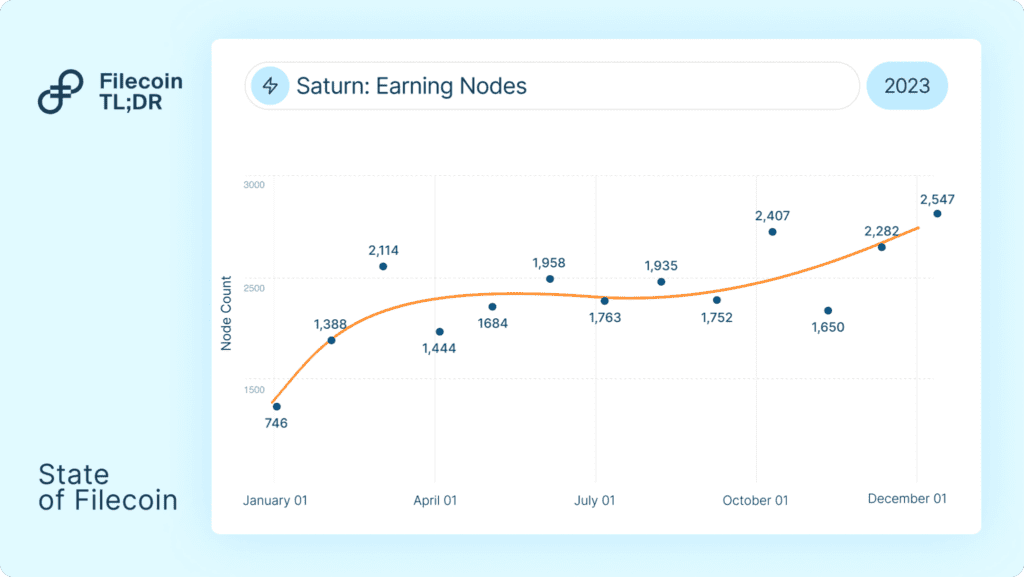

Filecoin Saturn: ✅

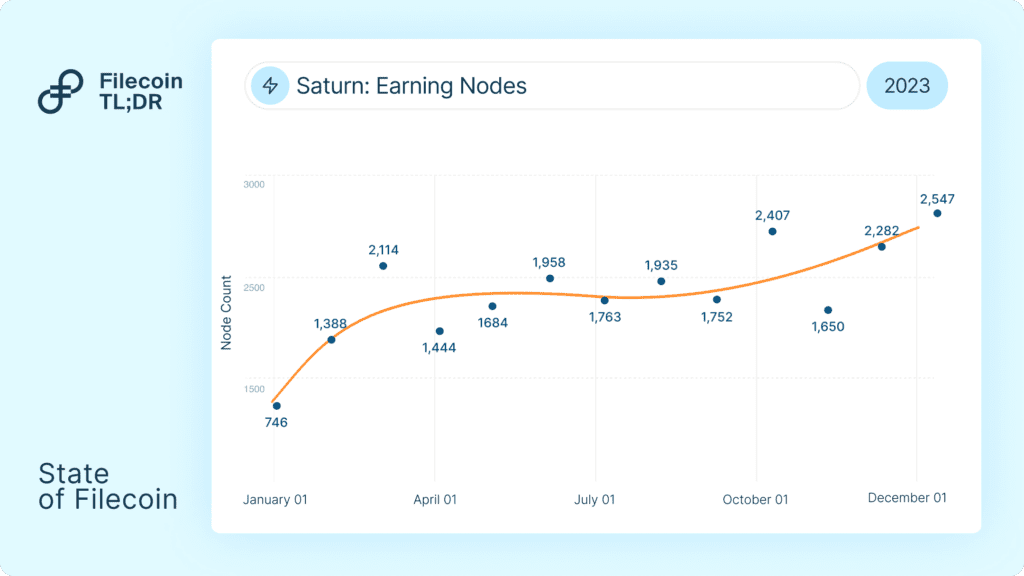

Saturn, a decentralized CDN network built on Filecoin, also leverages FVM for disbursing FIL payments to retrieval nodes on the network. In 2023, Saturn averaged over 2,000 earning nodes (retrieval providers on the network receiving FIL) for their services.

Decentralized Options

With growing liquidity, options are yet another emerging product in DeFi. Options facilitate the buying or selling of assets at a predetermined price on a future date, giving token holders protection against price volatility and an opportunity to speculate on market moves.

Thetanuts:✅

Currently, Thetanuts Finance, a decentralized on-chain options protocol supports Filecoin. The platform allows FIL holders to earn yield on their holdings via the covered call strategy. Thetanuts FIL-covered call vaults are cash-settled and work on a bi-weekly tenor.

Wallets

To use dApps on the FVM, users would be required to hold FIL in a f410 or 0x type wallet address. Over time, many Web3 wallets such as MetaMask, FoxWallet, and Brave have started supporting 0x/f410 addresses. MetaMask also supports Ledger. With this, it is possible to hold funds in a Ledger wallet and interact with FVM directly.

In addition, exchanges like Binance natively supporting the FEVM drastically reduce complexities for FVM builders. To learn more about the most recent wallet upgrades, visit the Filecoin TLDR webpage.

What’s Next?

The obvious near-term impact of various integrations across AMMs, Bridges, and CDPs is a fresh influx of liquidity into the Filecoin ecosystem. Liquidity begets deeper liquidity with an increase in the number and diversity of DeFi protocols on Filecoin. DeFi’s growing economy clubbed with more services coming on-chain and utilizing FVM for payments will overall increase the revenue and utility of the network. We expect this strong DeFi traction to scale Filecoin as an L1 ecosystem, with core services of storage and compute becoming the backbone of the decentralized internet.

To stay updated on the latest Filecoin happenings, follow the @Filecointldr handle.

Many thanks to HQ Han and Jonathan Victor for reviewing and providing valuable insights and to all the ecosystem partners and teams for their timely input.

Disclaimer: This information is for informational purposes only and is not intended to constitute investment, financial, legal, or other advice. This information is not an endorsement, offer, or recommendation to use any particular service, product, or application.

2023 marked significant shifts in technology and adoption for the Filecoin network. From the launch of the Filecoin Virtual Machine, to other developments across Retrievals and Compute, 2023 lay the foundation for Filecoin’s continued expansion. This blogpost will provide a summary of the notable milestones the Filecoin ecosystem reached in 2023, and in the later portion, growth drivers to watch for 2024.

TL;DR

2023 Retrospective:

Storage: Active deals reached 1,800 PiB, and storage utilization grew to 20%

FVM: FVM launch in March 2023 enabled FIL Lending (Staking) which supplied 11% of total collateral locked by Storage Providers; TVL broke USD 200M

Retrievals: Retrievability of Filecoin data improved, alongside notable releases from Saturn (3,000+ nodes, sub 60ms TTFB) and Station

Compute, AI and DePIN networks: Synergistic growth of Filecoin together with physical resource & compute networks

Web2 Enterprise Data Storage: Led by strengthened offerings by teams such as Banyan, Seal Storage, and Steeldome

Continued DeFi growth: DEXes, Oracles, CDPs, spurred by service revenue coming on-chain

2023 Retrospective

To recap, Filecoin enables open services for data, built on top of IPFS. While Filecoin initially focused on storage, its vision includes the infrastructure to store, distribute, and transform data. The State & Direction of Filecoin, Summarized blog post shared an initial framework for Filecoin’s key components. This framework will serve as an anchor for discussing 2023’s traction.

1) Storage Markets: Active storage deals reached 1,800 PiB with storage utilization of 20%

In 2023, Filecoin’s stored data volume grew dramatically to 1,800 PiB, marking a 3.8x increase from the start of the year. Storage utilization grew to 20% from 3%. Currently, Filecoin represents 99% market share of total data stored across decentralized storage protocols (Filecoin, Storj, Sia, and Arweave).

Growth in Active Storage Deals was driven by two factors:

1) Storing data was easier in 2023. Continued development across on-ramps such as Singularity.Storage, NFT.Storage, and Web3.Storage increased Web3 adoption. Singularity alone onboarded 180 plus clients and 270 PiB of data. This growth was enabled by advances in its S3 compatibility, data preparation, and deal making.

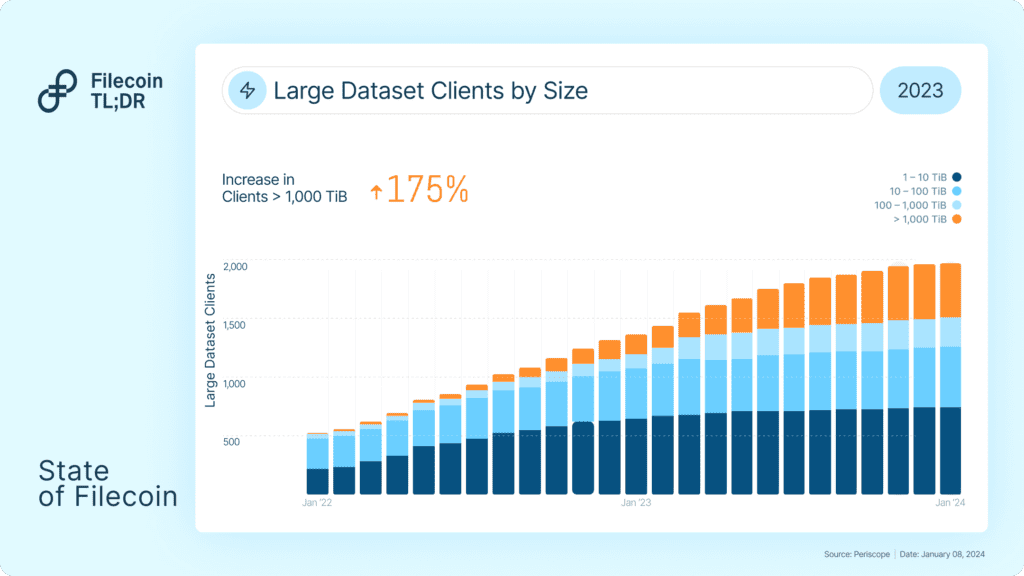

2) Large dataset clients grew exponentially in 2023. Over 1,800 large dataset clients onboarded datasets by the end of 2023, from an initial base of 500 plus clients. 37% of these clients onboarded datasets exceeding 100 TiB in storage size.

2) Retrievals: Greater reliability for Filecoin Retrievals, alongside releases from Saturn & Station

Filecoin’s retrieval capabilities were bolstered by improvements both in its tooling and offerings. Several teams, such as Titan, Banyan, Saturn and Station, are laying the groundwork for new use cases to be anchored into the Filecoin economy, including decentralized CDNs and hot storage.

Saturn: A Decentralized CDN

Saturn is a decentralized CDN network built on Filecoin, that seeks to address the need for application-level retrievals. The Saturn network currently has over 3,000 nodes distributed across the globe, enabling low-latency content regardless of location.

Distribution of Nodes: 35% in North America, 34% in Europe, 24% in Asia, 7% RoW Source: Saturn Explorer as of January 08, 2024

Across 2023, Saturn reduced its effective Time-to-First-Byte (median TTFB) to 60 milliseconds. This makes Saturn the fastest dCDN for content-addressable data, with TTFB remaining consistent across all geographies. Saturn was also capable of supporting 400 million retrieval requests on its busiest day of the year.

At the end of 2023, Saturn launched a private beta for customers (clients include Solana-based NFT platform Metaplex).

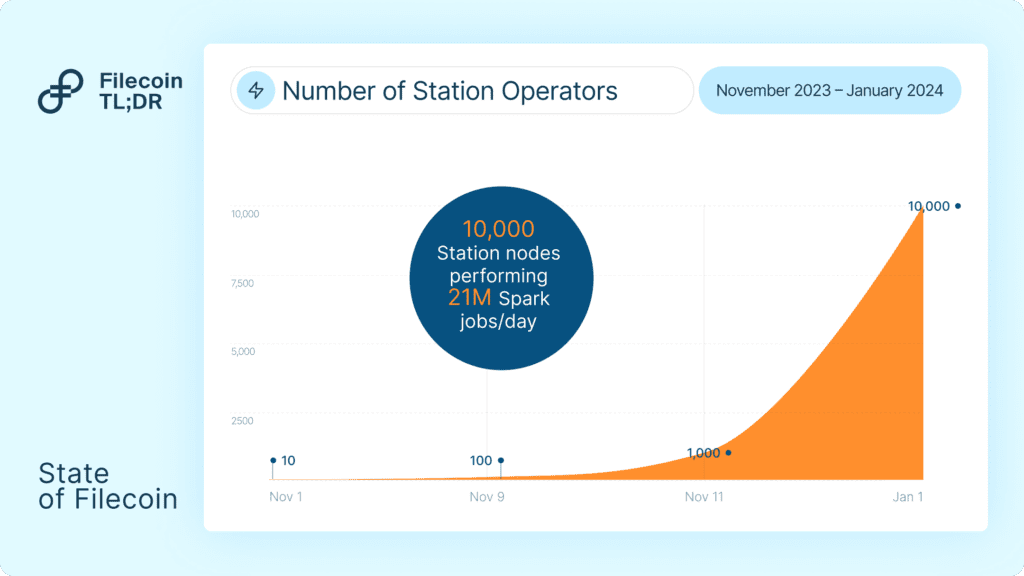

Station: A Deploy Target for Protocols (Enabling Spark Retrieval Checks)

Station, a desktop app for Filecoin, was launched in July 2023. Station is a deployment target for other protocols allowing DePIN networks, DA layers, and others to run on a distributed network of providers.

Station’s first module, Spark, is a protocol for performing retrieval checks on Storage Providers (SPs). Spark helps establish a reputational base for SP data retrievability, and supports teams looking to provide a hot storage cache for Filecoin. Since launch in Nov 2023, Spark has grown to 21 million daily jobs on 10,000 active nodes as of January 2024.

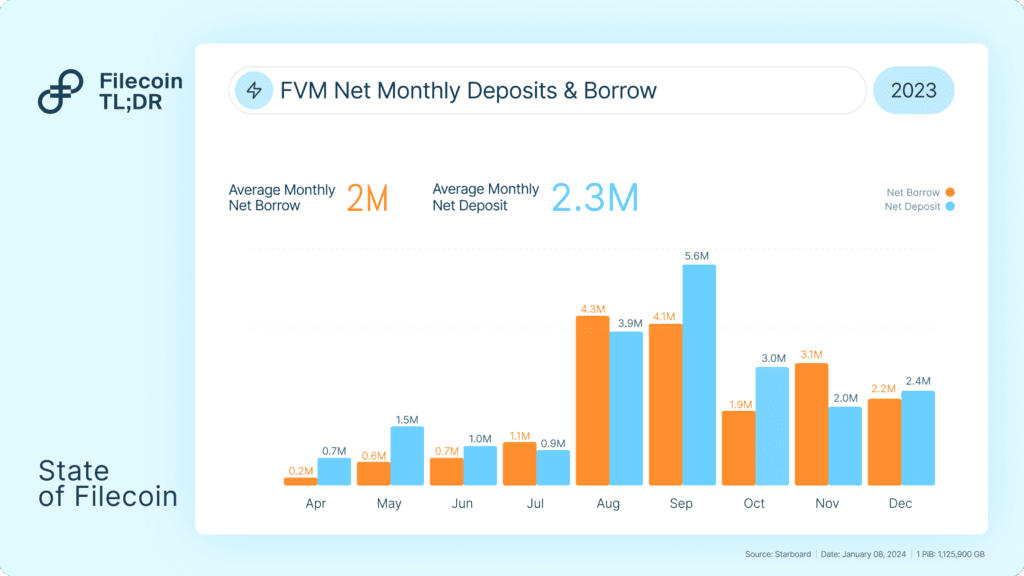

3) Filecoin Virtual Machine: The FVM launch introduced a new class of use cases for the Filecoin Network. Early DeFi adoption broke $200 million in TVL.

The Filecoin Virtual Machine (FVM) launched in March 2023 with the EVM being the first supported VM deployed on top. FVM brought Ethereum-style smart contracts to Filecoin, broadening the slate of services anchoring into Filecoin’s block space. Two areas of early adoption have been in liquid staking services (led by GLIF and other DeFi protocols) and micropayments via the FVM.

Liquid Staking

One of the core economic loops in the Filecoin economy is the process of pledging, where SPs put up collateral to secure capacity and data on the network. Prior to the FVM, borrowed Filecoin collateral was sourced through managed offerings from operators like Darma Capital, Anchorage, and CoinList. Post-FVM, roughly a dozen staking protocols have launched to grow Filecoin’s on-chain capital markets.

In aggregate, FVM-based protocols supply almost 11% of the total locked collateral (approx. 19 million FIL) on the network, giving yield access to token holders, and increasing the access to capital for hundreds of Filecoin SPs. From Filecoin’s collateral markets alone, the ecosystem has broken past 200 million in TVL.

Payments

Adjacent to the core storage offering on Filecoin, new services are being built that anchor into Filecoin’s block space. As mentioned in the Retrieval Markets section, two notable services (Station and Saturn) have actually started leveraging FVM for payments in 2023.

To date, Station users have completed 161 million jobs with more than 400 addresses receiving FIL rewards. Saturn averaged over 2,000 earning nodes in 2023 with 448,905 FIL disbursed to date.

4) Compute: Traction for Decentralized Compute Networks

Filecoin’s design enables compute networks to run synergistically on Filecoin’s Storage Providers. Sharing hardware with compute networks is also valuable to the Filecoin network: (1) sharing allows Filecoin to offer the cheapest storage by running side-by-side with compute operations, and (2) it brings additional revenue streams into the Filecoin economy.

Two key developments made running compute jobs on Filecoin nodes:

Sealing-as-a-service: Sealing-as-a-service is the process by which Storage Providers (SPs) can outsource production of sealed sectors to third-party marketplaces. This gives SPs greater flexibility in operations and reduces costs of sector production. One marketplace, Web3mine, has thousands of machines participating in its protocol offering cost savings to SPs of up to 70%. On top of the cost savings, the infrastructure built may also eventually benefit SPs by allowing them to leverage their GPUs for synergistic workloads (e.g. compute jobs)

Reduced Onboarding Costs:Supranational shipped proof optimizations reducing sealing server cost by 90% and overall cost of storage by 40%

On top of these developments, 2023 saw emerging compute protocols building in the Filecoin ecosystem. Two notable examples:

Distributed compute platform Bacalhau demonstrated real-world utility among Web2 and DeSci clients. Most recently, the U.S. Navy chose Bacalhau to assist them in deploying AI capabilities in undersea operations. Bacalhau is a platform agnostic compute platform intended to run on Web3 and Web2 infrastructure alike. Launched in November 2022, Bacalhau’s public network surpassed 1.5 million jobs and in some cases slashed compute costs by up to 99%

Source: Bacalhau

Up-and-coming compute networks likeIo.net allow ML engineers to access a distributed network of GPUs at a fractional cost of individual cloud providers. Io.net recently incorporated 1,500 GPUs from Filecoin SPs — positioning Filecoin providers to offer their services to Io.net’s customer base. Io.net has over 7,400 users since its launch in November 2023, serving 15,000 hours of compute to users.

2024 will be a critical growth year for Filecoin as groundwork laid in 2023 comes to fruition. Native improvements to storage markets, greater speed of retrievals, new levels of customizability & scalability brought by FVM and Interplanetary Consensus (IPC), all expand the universe of use cases that Filecoin can address.

In a Web3 climate where there is substantial attention on DePIN (and the tying of real world services with Web3 capabilities) these changes will be critical building blocks for even better services. Here are three themes to look for in 2024:

1) Synergies with Compute, AI and other DePIN networks

In 2024, foundational improvements to the network will substantially improve Filecoin’s ability to compose with other ecosystems.

Fast finality allows better cross-network interactions with app chains in other ecosystems (e.g. Cosmos, Ethereum, Solana).

Customizable subnets allow for novel types of networks to form on top of Filecoin such as general purpose compute subnets (e.g. Fluence) and storage pools (e.g. Seal Storage).

Hot storage allows for broader use case support including serving data assets for physical resource networks (e.g. WeatherXM/Tableland), caching data for compute networks (e.g. Bacalhau), and more.

This is all scratching the surface. As the Web3 space and DePIN category grows, Filecoin is well positioned to support new communities that form given its 9 EiB of network capacity and flexibility. There exists a sizable opportunity within physical resource networks producing high amounts of data, such as Hivemapper (over 100M km mapped), and Helium (1 million hotspots globally). Compute networks are also a likely growth area, given the backdrop of a GPU shortage (particularly for AI purposes) in traditional cloud markets.

Source: Messari

2) Focused Growth in Web2 Enterprise Data Storage

Web2 enterprise storage is a unique challenge for decentralized networks – requirements from these customers are not easily supported by most networks. Typical requirements from enterprise clients can include end-to-end encryption, certification for data centers, fast retrievals, access controls, S3 compatibility, and data provenance/compliance. Crucially, these requirements tend to differ across segments and verticals, which means that a level of adaptability is required. Filecoin’s architecture enables it to layer on support for the features these customers need.

A few teams worth keeping an eye on:

Banyan: Banyan simplifies how enterprise clients integrate with decentralized infrastructure by bundling hot storage, end-to-end encryption, and access controls, on top of a pool of high-performing storage providers. With the Filecoin network, Banyan provides content-addressable storage, which it plans to complement with hot storage proofs by utilizing FVM. This implementation makes Banyan compatible not only for enterprise, but DePIN and compute networks.

Seal: Seal has established itself as one of the best storage onramps in the Filecoin ecosystem, and is responsible for onboarding several key clients onto the network, such as UC Berkeley, Starling Labs, the Atlas Experiment, and the Casper Network. The team has been one of the driving forces in enterprise adoption to date, and most recently has achieved SOC 2 Compliance. In 2024, they plan on launching a subnet to enable a market for enterprise deals. On the back of their enterprise deal flow, they are positioned to bring petabytes of data into the network over the coming year via their new market.

Steeldome: Steeldome offers enterprise clients seeking data archival, backup and recovery with an alternative that is cost-competitive, efficiently deployed and scalable. It does so by combining Filecoin in its stack with Web2 technologies, allowing a fuller feature set to complement Filecoin’s cost-effective and secure archival storage. The Steeldome team has succeeded in onboarding clients across insurance, manufacturing, and media. In 2024, they plan to continue that trajectory, while offering a managed service for Storage Providers.

3) Greater On-chain DeFi activity

There is likely to be continued activity in the on-chain economy with an increase in the number and type of DeFi protocols on Filecoin.

The first protocols will increase service revenues (from Storage, to Retrievals, and Compute) coming on-chain. As previously described, more services are coming online in the Filecoin network, and are utilizing FVM for payments (e.g. Saturn, Station).

Key releases in 2023, including SushiSwap going live in Nov 2023, and the UniSwap community’s approval of integrating on FVM will lead to more diverse DeFi services coming on-chain. This will include CDPs (Collateralized Debt Positions), and Price Oracles (e.g. Pyth), among others.

Final Thoughts

In 2024, the Filecoin network will experience greater adoption, particularly by Compute, AI and DePIN networks, as well as targeted enterprise verticals. This adoption brings on-chain service revenue and supports the growth of DeFi activity beyond collateral markets. Continued improvements on storage markets, retrievability driven by hot storage proofs and CDN networks, as well as releases by FVM and IPC will enable the teams building on Filecoin to drive this next stage of growth.

To stay updated on the latest in DePIN and the Filecoin ecosystem, follow the @Filecointldr handle.

This blogpost is co-authored by Savan Chokkalingam and Nathaniel Kok on behalf of FilecoinTLDR. Many thanks to HQ Han and Jonathan Victor for reviewing and providing valuable insights and to all the ecosystem partners and teams for their timely input.

Disclaimer: This information is for informational purposes only and is not intended to constitute investment, financial, legal, or other advice. This information is not an endorsement, offer, or recommendation to use any particular service, product, or application.

Editor’s Note: This blog is a repost of original content from IOSG Ventures. IOSG Ventures is a community-friendly and research-driven early-stage venture firm. This blog post represents the independent views of the author, who has given permission for re-publication.

The programmable layer on FIL, the FVM, allows for trustless marketplaces to be built

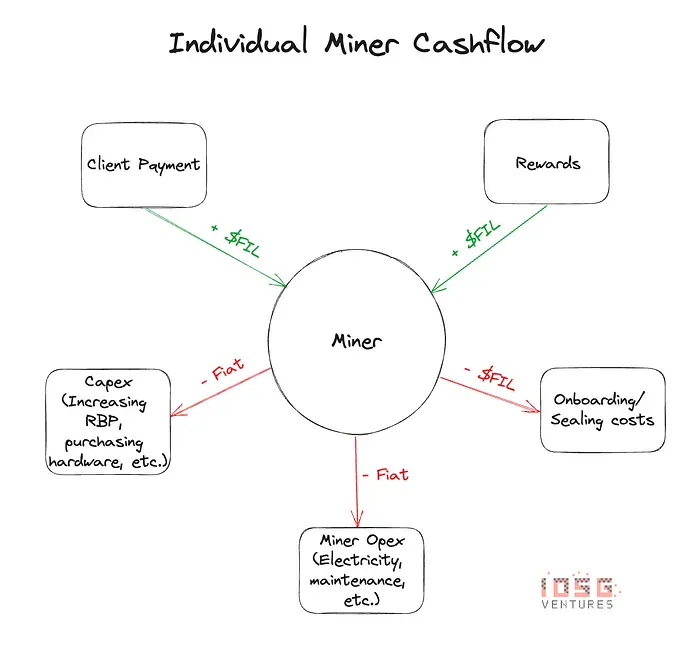

This calls for a need for a marketplace that currently exists off-chain, i.e. FIL borrowing to be brought on-chain, where FIL token holders lease their FIL to Storage Providers (which some call “miners”) who borrow FIL from the pool(s)

FIL borrowing is essentially taking cash forward on the future block rewards accrued by the Storage Providers, and this makes FIL block rewards from data storage more capital-efficient

There are obvious trade-offs to be made between centralization-capital efficiency- and security in protocol design

The market size for borrowing FIL is reducing over time but the introduction of stablecoins, etc. Can unlock unique projects to be built on top of these protocols

The launch of a programmability layer on a seasoned blockchain generally comes with a lot of excitement. The launch of Stacks (STX) on the Bitcoin blockchain brought a new paradigm of thinking amongst the community built around it.

A very similar narrative happened with the launch of the FVM on Filecoin. The robust Filecoin community now has to see its vision through a completely different lens. A lot of open problems that the ecosystem had could now be addressed. Creating trustless marketplaces via programmability was a key piece of the puzzle.

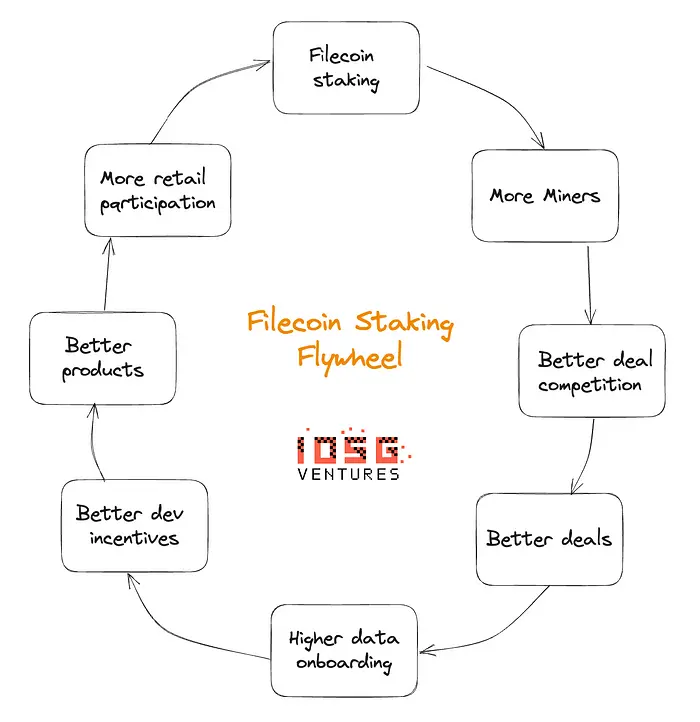

Liquid staking on Filecoin was the first “Request-for-build” from the Filecoin ecosystem during the launch of FVM and was given high importance. To understand why this is, let us first understand how the economics of Filecoin work.

How Filecoin Incentives Work

Unlike an Ethereum validator, there is no one-time staking in Filecoin. Every time a Storage Provider (SP) provides services, they need to put up a pledge amount in FIL. This pledge is required to seal the sectors and store the sealed sector in the SP. Such a structure ensures that the SP is going to store data for their clients for the period of the deal that they agree to, in exchange for rewards. Rewards are distributed via PoSt (Proof of Space-Time), where the SPs are rewarded for proving that they have the right client data stored.

SPs are selected via a leader selection mechanism called DRAND. DRAND chooses the leader with some initial requirements and also the % of raw byte power of the network controlled by the SPs.

SPs will have to keep ramping up raw byte power (RBP) to be chosen as the leader to “mine” a block and receive incentives. This helps the SP subsidize their storage costs.

Although there are many more factors that govern the supply rate of these incentives, the baseline is that for storage providers/miners, to maximize their bottom line will have to try to maximize RBP and onboard (and renew) more deals.

This creates a positive loop for the Filecoin network

Economics of a Storage Provider

When an SP receives block rewards, these rewards are not liquid. Only 25% of the rewards are liquid, and the remaining 75% of the block rewards vest linearly over 180 days (~ 6 months). This poses a problem for SPs. The rewards, which are supposed to be an SP’s operating income, are now delayed payments for as long as the SP onboards/renews deals.

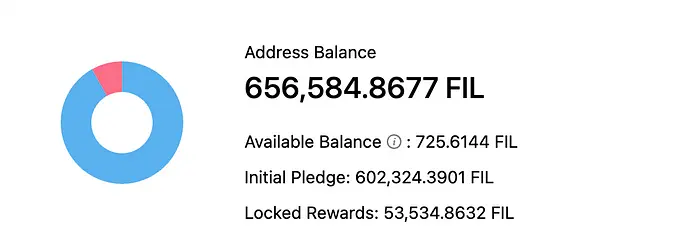

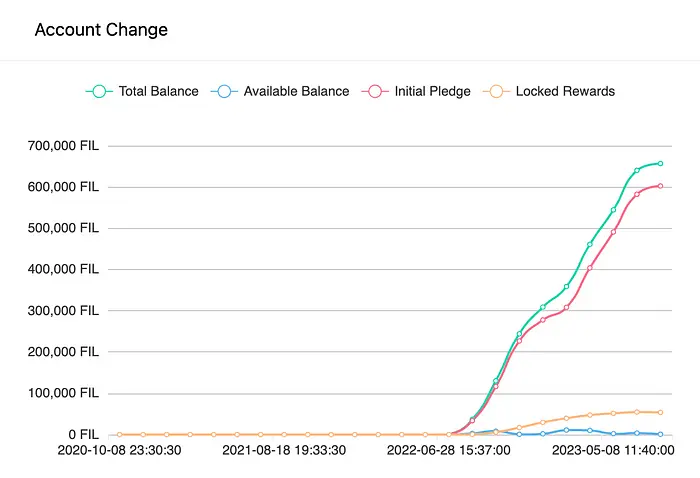

Let us look at the SP balance of the top miner in the network (as of 6th August 2023)

When you look at the graph, one can see that only about 1% of the rewards (or operating income) of the SP is actually liquid. If this SP now wants to either:

Pay for operating income

Upgrade hardware

Pay for maintenance

Or onboard/ renew deals

The SP will have to either borrow fiat currency or borrow FIL from third parties just to make up for these “delayed” payments.

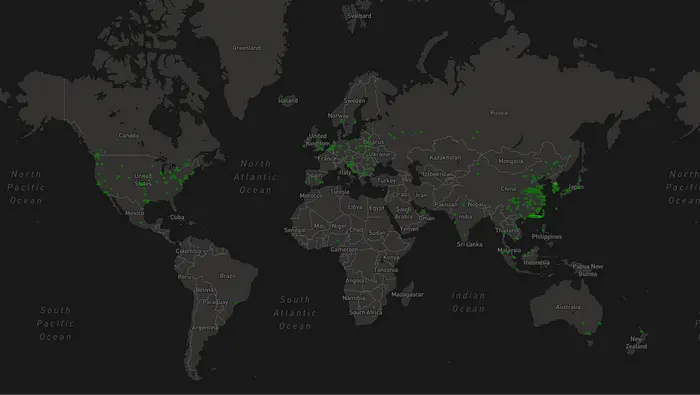

At the moment many storage providers (miners) in the network rely on CeFi lenders such as DARMA Capital, Coinlist, and a few others. As these are loan products, storage providers will have to go through KYC and a strict audit process to be able to borrow FIL. When we look at the map below, we can see a very high concentration of Filecoin SPs in Asia, and with centralized providers being mostly in the West, it is very hard for them to underwrite FIL loans to Asian miners with favorable terms, and most Asian miners/ SPs don’t have access to such providers.

This becomes a hindrance for new SPs to come in and participate in the system, and existing SPs can scale their business only as much as the total FIL pool size of these CeFi lenders

So why not just borrow fiat currency from a bank? With FIL being a volatile asset, it will pose additional capital management challenges for SPs who borrow.

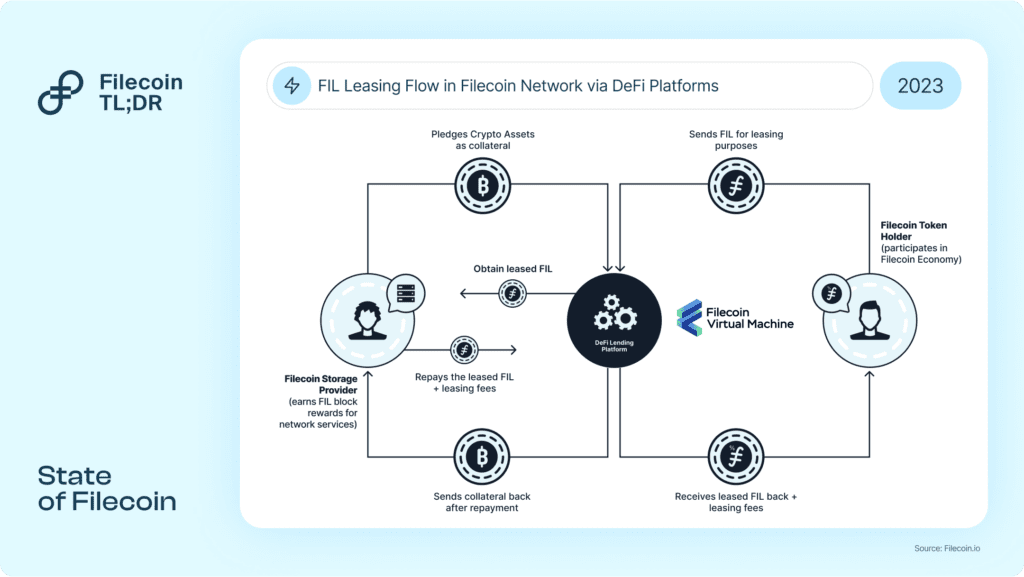

To solve this problem, there needs to be a marketplace for FIL lenders (who could be holders of FIL) and FIL borrowers (SPs)

Filecoin Staking

With the launch of the FVM, this marketplace idea can come to fruition. FIL lenders/stakers can now put their FIL to work and SPs can borrow from this pool (either in a permissioned or permissionless manner) all governed by smart contracts.

There are many players in the ecosystem who are already building this and waiting to launch in the coming months.

More than calling such marketplaces staking protocols, it is a lot closer to a lending protocol by the nature of this business.

Some base features of such a FIL lending product would be:

Lenders deposit idle FIL and receive a “liquid staking” token

Borrowers (SPs) can borrow from the pool against collateral that exists in the SP actor (Essentially Initial Pledge + Locked Rewards)

Borrowers will make interest payments every week, or any specified time period, by signing over the “OwnerID” of the SP to a smart contract

Lenders receive the interest (minus protocol fees) as APY either via a rebase token or a value accrual token

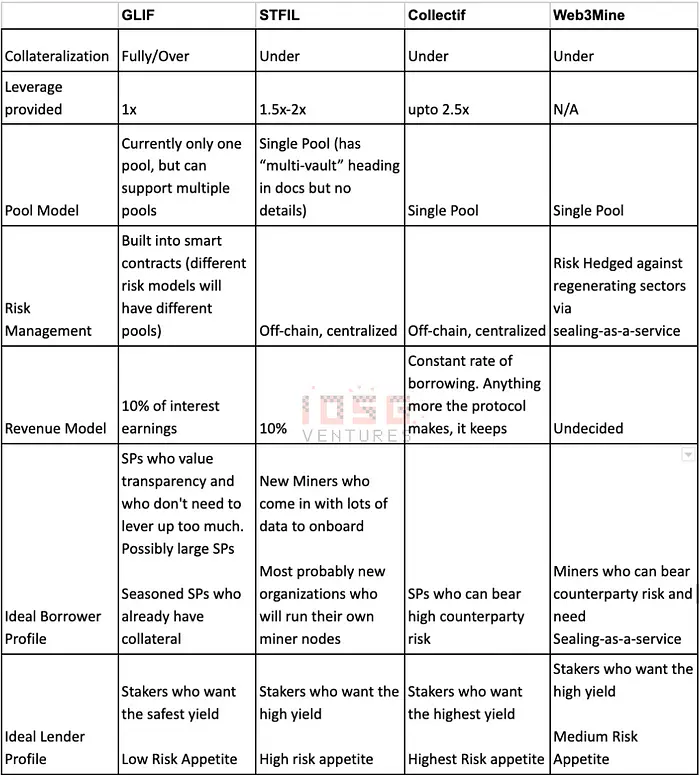

Different liquid staking protocols have different schools of thought when it comes to borrowing:

Over/ Fully collateralized vs. Undercollateralized

In Over-collateralized or fully collateralized models, the debt-to-equity ratio is always going to be less than or equal to 100%. This means that if my SP balance is say 1000 FIL, I can only borrow up to 1000 FIL (depending on the protocol rules as well). This can easily be coded into smart contracts and default risk is built in. This allows for greater transparency and also security to the stakers (lenders). Another advantage of such a model is that it allows for permissionless borrowing as well. This is where the product blocks more like Aave/ Compound rather than a Lido or RocketPool.

In an uncollateralized model, the lenders are bearing risk while the risk is being managed by the protocol. In such a model, risk modeling is complex math that cannot be baked into smart contracts, and needs to be off-chain which sacrifices transparency. But, since there is leverage involved, it makes the system a lot more capital-efficient for the borrower. The more permissionless a leveraged system will get, the more risk the lenders bear and this would call for a very robust and dynamic risk management model that is run by the protocol developers

The trade-offs being made are:

Capital efficiency vs. staker risk

Capital efficiency vs. transparency

Lender risk vs. borrower entry to the system

Single Pool vs Multi-Pool

Protocols can also opt to build a multi-pool model where lenders can choose to stake FIL in different pools with different risk parameters. This allows for risk to be managed on-chain, but liquidity will be fragmented. In a single-pool model, risk will have to be maintained off-chain. Overall the trade-offs will still remain the same as the ones mentioned above.

Trade-off: Liquidity fragmentation vs Risk management transparency

Risks

In an overcollateralized model, even if the miner gets slashed multiple times, as soon as the Debt-to-equity ratio hits 100% the miner will get liquidated and the stakers will be comparatively safe

In an undercollateralized model, the borrowers can be penalized for failing to prove sectors. There are many more faults in failing to prove data storage rather faults in the consensus itself. This is more common in Filecoin than in other general-purpose blockchains because there is an actual commodity that is being stored from an off-chain entity. This will affect the collateral value and lever the borrower more. Liquidation thresholds will have to be set very carefully in such a model.

What about Ethereum Staking/Lending protocols entering the market?

In the Filecoin ecosystem, unlike the Ethereum ecosystem, the nodes (Miners/Validators/SPs) are responsible for much more than general uptime. They are supposed to market themselves to be chosen as SPs, and regularly upgrade their hardware to support more storage, seal, store, maintain, and retrieve data. Filecoin storage and reward mining for SPs is a full-time job.

Unlike an Ethereum validator, there is no one-time staking in Filecoin. Every time an SP provides storage to a client, they need to put up a pledge. This pledge is required to seal the sectors and store the sealed sector in the SP. Storage provision on Filecoin is a very capital-intensive process and this discourages many new SPs from participating in the network and existing SPs from staying and contributing to the network.

Since the participants on the borrow side are SPs only it is also going to be intensive for newcomers in the Filecoin ecosystem to bootstrap borrower trust.

The mechanics of Filecoin alone don’t allow Ethereum staking or even lending protocols to deploy easily on the FVM.

Economics of the Protocol

Is there enough FIL in the market to supply for lending?

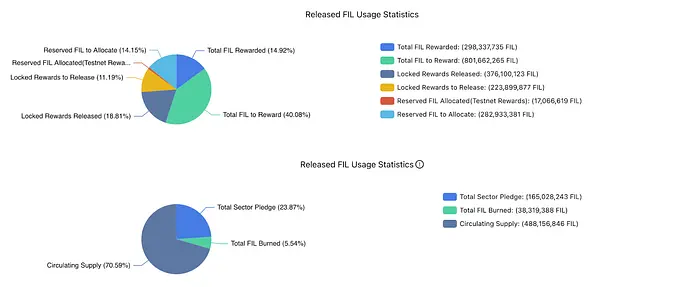

As of August 6th, 2023, there are about 264.2 million FIL circulating that are not committed as sector pledges or rewards that are to be released. This can be counted as the total amount of FIL that can be staked by the lenders into the pool

While FIL borrowing is essential to SPs, what are they actually borrowing? They are taking a forward payment on their locked-up rewards in an overcollateralized model, and in the undercollateralized model, they are taking a forward payment on future rewards.

Looking at the graphs above, we can see that the total locked rewards are about 223M FIL, and the supply can match the demand. The demand-to-supply ratio is almost 84%. This shows even power dynamics on either side, and either side cannot squeeze the other on interest rates/ APY.

What does the future look like?

Estimating the market for future demand of FIL for borrowing is essentially the amount of FIL that will be released in the future as rewards.

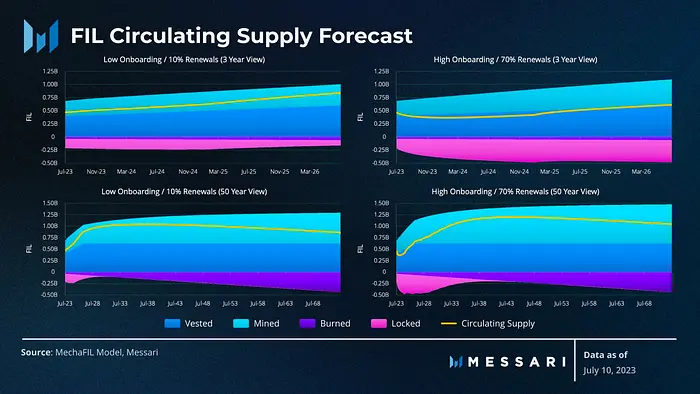

The good folks at Messari ran a simulation of FIL circulating supply with a 3-year and a 50-year forecast using different cases.

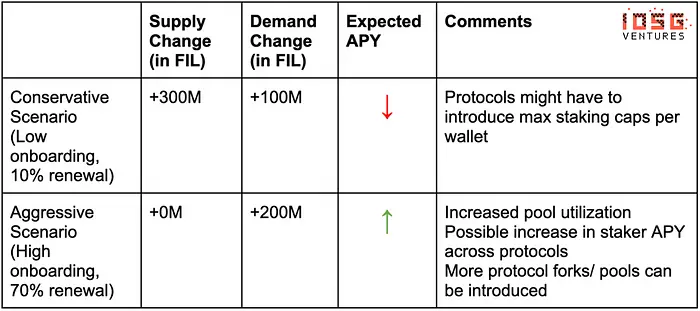

According to the top left graph, considering a conservative scenario where there is low onboarding of data and only 10% of the total deals are renewed, the new reward emissions over 3 years are close to around 100M FIL and in an aggressive scenario where there is a high amount of data onboarding and 70% of existing deals renewed, the extra rewards come to about 200M FIL

So one can expect a market size of somewhere between 100M — 200M FIL over the next 3 years. At the current price of FIL (Aug 6th), which is $4.16, there could be a borrowing TAM of about $400M — $800M. This could be counted as the TAM of the product’s borrow side.

On the supply side, in the conservative estimate, there can be about 300M FIL that will be emitted, and in a more aggressive scenario, the circulating supply is simulated to be around the same as it is today. Why? It is because if more deals are being onboarded and renewed, there will be a lot more FIL locked-in sector pledges.

In the more aggressive scenario, the demand is going to outweigh the supply and the interest charged can be higher in this competitive market.

Where I think this can go

Amongst the different designs, there need not be a winner-takes-all type of model. Intuitively, the long-term winner (by TVL) is generally the protocol that is built most safely. Very much like Lido in the Ethereum ecosystem. I for one am biased towards safer structures more than optimizing for 2–3% more yield, and I think FIL whales would also prioritize capital safety over a slightly higher yield.

This is after considering the amount of penalties miners pay for not being able to prove space-time.

From the borrower (SP) end, the SP could borrow from different protocols for different purposes. If the SP already has a lot of collateral and doesn’t need to lever up to pay for opex, then the safer, overcollateralized model will work better, since it is safer. Whereas if I am a newer SP with a lot of sectors to be pledged I would borrow with leverage from an undercollateralized pool.

After studying the above models, we can see:

Staking in Filecoin is important to bridge the supply and demand for FIL in the ecosystem. The FVM has recently been released allowing for a lending marketplace to exist. Although the problem is real, the FVM release was probably too late for most FIL staking/lending protocols as the pie (mining rewards) is decreasing over time making it a niche market.

However, a few fascinating use cases can emerge on top of these staking protocols. With the introduction of stablecoins, the rewards can be taken as cash forwards. Something similar to what Alkimiya is building on Ethereum. This can result in the injection of new capital into the Filecoin ecosystem and also increase the TVL in these protocols.

Ethereum’s and Filecoin’s tech is different, their miners are different, their developers are different, their apps are different, and hence their communities. And for staking in particular, with every miner being “non-fungible” bootstrapping the demand side becomes a BD exercise and the success of it is directly proportional to the protocol’s reputation in the community.

Filecoin staking is a critical solution that needs to be built to get more SPs in the system, for retail to put their capital to work, create greater economic incentives as an ecosystem to attract more developers, and build useful products to build a positive flywheel. To know more beyond staking in the Filecoin ecosystem and the criticality of the FVM you can read this previous piece we published.

There are many more open problems to be solved in the Filecoin ecosystem, but we are positive that the Filecoin Ecosystem is working in the right direction to achieve its vision of storing humanity’s data in an efficient system.

This blog post explains what Filecoin’s Virtual Machine (FVM) is, why it matters, and how one might evaluate and prioritize the opportunities it unlocks.

First, we will explain what the Filecoin Virtual Machine is and how Filecoin becoming programmable lays the foundation for composable products and services in the Filecoin economy.

Secondly, we introduce a framework to categorize the universe of potential FVM-powered use cases into distinct opportunity areas. This section discusses specific opportunities unlocked by the FVM and how venture investors, developers, storage providers and other stakeholders may evaluate and prioritize them.

In the third section, we explore how, by commoditizing cloud services and by allowing anyone to create and monetize products and services around data, the FVM stands to fully unleash and augment the full potential of a trillion dollar open data economy.

We conclude by discussing what has energized many hundreds of teams to start building on the FVM, and by providing information on how you can stay up to date on all things FVM.

1. The FVM brings user programmability to Filecoin creating a watershed moment for innovation

Filecoin’s larger roadmap aims to turn the services of the cloud into permissionless markets on which any provider can offer their services. The launch of smart contracts (also known as ‘actors’) on FVM on March 14 2023 is a critical component of this larger vision as FVM allows for user programmability around the key services of the Filecoin network: Large-scale Storage, Retrieval, and Compute over data.

What’s exciting about FVM is the ability for any developer¹ to deploy smart contracts on the network. One may compare this to the moment that phones became programmable: The ability to write and install apps significantly augmented what people could do with phones and allowed the devices to go far beyond the capabilities of their pre-installed, hard-coded software. It was a watershed moment for innovation.

Similar dynamics stand to unfold when Filecoin becomes programmable by anyone through FVM. Since Filecoin’s storage market is currently the primary service anchored into the Filecoin blockchain today, the first big unlock will likely be programming around the state of Filecoin’s storage deals. Specifically, anyone will be able to (within certain limits) write software on what, how, when and by/for whom data is stored via Filecoin, the world’s largest open access storage network.

The FVM is a state machine that allows users to program around the state of the Filecoin blockchain

While the FVM does not directly interact with the data stored on the Filecoin network (just its metadata!), it will enable automation of storage and related services (e.g. off-chain data indexers, oracles) and settlement of value. This automation unlocks many new use cases. Illustratively, find a few select opportunities (Perpetual Storage, DataDAOs, Filecoin staking) that arise from assembling the different building blocks that the FVM provides access to below.

The FVM enables the settlement of value as well as building smart contracts that can interact with the metadata of services anchoring into the Filecoin blockchain (e.g., storage)

These illustrative recipes for use cases can be endlessly re-combined with each other and other components (e.g., developer tooling, end-user interfaces etc.). Additionally, they may eventually also leverage other building blocks of the Filecoin economy which anchor into the same blockspace (e.g., retrieval of and computation on content-addressed data) as well as those of other economies (e.g., via cross-chain bridges or oracles). These combinations will result in the emergence of ever more sophisticated services.

2. How we see the use cases unlocked by the FVM

The use cases unlocked by the FVM are loosely grouped into the following opportunity areas:

Data onboarding & management: e.g., tools automating storage deal-making to unlock use cases like perpetual storage

Data curation & monetization: e.g., tools facilitating the collective creation, curation and monetization of valuable datasets

Decentralized finance: e.g., to provide access to collateral for the thousands of storage providers offering services on the network and to create new opportunities for token-holders to participate more actively in the Filecoin economy

Network participant discovery and analytics: e.g., storage provider reputation services or data retrievability oracles that create differentiation opportunities and may enhance the reliability of the decentralized cloud for its users

Integration, interoperability and other services: e.g., cross-chain bridges to integrate with other economies or NFT-standards with built-in storage guarantees, developer tooling and more

It is important to note that due to the recombinant nature of FVM-powered use cases and web3 in more broadly, businesses may cut across several of these opportunity areas.

The use cases unlocked by the FVM can be loosely grouped into five opportunity areas, each unlocking sizable markets

One of the unique advantages of FVM-powered services starting up in the Filecoin economy is access to a large number of storage providers seeking to boost their profitability. In February 2023, storage providers on the Filecoin network had collectively locked up 130M+ FIL in collateral to secure their commitments to keeping the network and their clients’ data safe.

Additionally, storage providers have collectively invested millions of dollars to stand up the data centers that provide many exabytes of capacity. Partly due to the absence of DeFi solutions, access to collateral and other financing is relatively difficult today.² As a result, services that lower these costs and reduce complexity for storage providers and/or unlock new revenue streams represent sizable addressable markets. This advantage is also a distinguishing dynamic that makes Filecoin a differentiated L1.

To lower cost, DeFi lending services may provide cheaper access to capital (which is required for collateralizing storage deals) by using storage provider reputation scores to improve underwriting or by using smart contracts to enforce repayment (e.g., by using future block rewards as collateral) directly to those lenders that made them possible. Such services³ also stand to benefit from being able to tap into the large number of token-holders — many of which are eager to participate in the Filecoin economy more actively.⁴ Furthermore, data on-boarding and management services may lower costs for storage providers by lowering storage client acquisition costs (e.g., via deal aggregators) and/or by reducing the overhead of being a Filecoin storage provider (e.g., by modularizing the operations).

FVM-powered services may also increase SP revenue by enabling data access or encryption solutions (e.g., Medusa, Fission, Lit or Lighthouse) which make Filecoin solutions viable for new customer segments, by giving SPs more opportunities to differentiate (e.g., via reputation or compliance-certification tools), increasing the duration of storage deals (potentially in perpetuity) and allocating Fil+ datacap more efficiently.

Cross-chain bridges and messaging to other (web3) ecosystems which facilitate the importing and exporting of services to and from the Filecoin economy also represent large opportunities for growth — both in utility for the Filecoin network (and thus in demand for Filecoin blockspace) and for increasing utility for web3 overall. In the near term, developers may also capitalize on opportunities around the tooling that makes building the services outlined above more feasible.

Collectively, these opportunities represent markets with hundreds of millions of dollars in revenue potential. Different considerations will inform how the stakeholders may prioritize the development of each opportunity area. Additionally, stakeholders may strategically sequence the development of different opportunity areas to maximize impact. The below framework provides an overview of potential dimensions that one may use to assess opportunities unlocked by the FVM.

Different considerations, such as the ones provided in this non-exhaustive list, will inform how stakeholders may prioritize and sequence the development of use cases in different opportunity areas

3. Empowering more people to create and capture value around data to unleash the full potential of an open data economy

Importantly, Web3 and Filecoin, and the FVM specifically, will continue to commoditize the services of the cloud and allow for better value attribution in the data economy. This section explains why this commoditization is needed and how it opens up access to the data economy and augments the ways in which value can be created, captured, and more equitably shared.

Let the data economy be defined broadly as covering businesses around data analytics and transformation (e.g., software for encryption, transcoding and more), data access and monetization (e.g., on-demand streaming services), the financial services facilitating transactions between market participants as well as the sale of hardware required to power these businesses.

Today, the core tenets underpinning this data economy (i.e., cloud storage and compute, content-delivery networks and more) are dominated by a few large companies. These organizations are successfully leveraging economies of scale to moat their businesses. The resulting dominance of a few large players has not only created central points of failure, but also stifled innovation and kept prices artificially high.

Web3, Filecoin, and the FVM stand to challenge these dominant players: The composability and power of crypto-economic incentives allowed the Filecoin community to rapidly bootstrap into existence an ever-expanding and competitively priced network of storage providers. Filecoin’s open access storage network is already the world’s largest of its kind, its capacity eclipsing even some publicly traded centralized storage providers. As Filecoin moves closer to its vision, infrastructure anchoring into the Filecoin network will also commoditize the services around content-delivery (e.g., via Filecoin Saturn) and compute over data (e.g., via Bacalhau).

Secondly, in today’s data economy value creation often stems from collectively generated datasets (think: users creating content for social networks and other signaling interest for that content), the capture of that value is largely privatized in today’s data economy. This is due to the fact that well-functioning mechanisms that would let data originators participate directly in the capture of value around datasets that they collectively create did not successfully emerge in web2. Instead, the most effective in monetizing collectively created datasets turned out to be advertising.

Web3 tech is, however, structurally better positioned to trace and retroactively reward contributors (even for data points with small marginal value) by using its decentralized ledgers. With the FVM, specifically, any number of unaffiliated parties could use the Filecoin token (or a FVM-powered L2 abstraction thereof) to form an incentivized collective around the creation, preservation and monetization of datasets (that otherwise may never emerge):

Imagine individuals monetizing their contributions to the training data of an AI model or to a social graph

Or researchers using the proceeds of selling access to a database of bacterial pathogens (which may be used to inform antibiotic diagnostics or improve drug discovery) to finance the continued curation and maintenance of said database

Or an ever-expanding encyclopedia rewarding its most active contributors directly as opposed to letting the value flow through an intermediary foundation

As projects like these emerge, the ability to capture value will likely depend to an ever greater degree on having access to proprietary datasets. Additionally, the open nature and the composability of such services also allows users to preserve their agency to exit, remain loyalto, or voice their concerns about data-centric services. This agency preservation will force institutions to think about dataset privacy and sharing in more sophisticated ways than “just trust us”. It may also result in allowing users that own their data to keep a (larger) share.

In summary, the trends around commoditization and better value attribution fueled by FVM and Filecoin will not only lead to fiercer competition and more pressure to innovate across all sectors of the data economy, but also solidify Filecoin’s position as the Layer-1 blockchain uniquely poised to power this open data economy.

Conclusion: FVM creates fertile ground for accelerated growth of the Filecoin ecosystem

FVM stands to unlock the development of applications, markets and organizations that will eclipse the scale and breadth of services offered by centralized cloud providers.

This potential has energized the community tremendously: Weeks before the official launch of the FVM, there are hundreds of teams building with the FVM on the testnet. Additionally, FVM-specific hackathons (e.g., Spacewarp) leading up to the launch of the FVM saw the highest registration numbers for a Filecoin-exclusive hackathon ever.

The Filecoin community continues to foster a radically recombinant ecosystem that accelerates the best ideas. FVM is highly cross-compatible thus catalyzing the adoption of Web3 technologies alongside and in partnership with other ecosystems and L1 blockchains.

Similar to how a computer may support multiple operating systems, Filecoin’s Virtual Machine will support multiple runtimes. The first runtime to launch will be the Filecoin Ethereum Virtual Machine (FEVM). This eases the ramp-up for EVM developers who can leverage tried and tested developer tooling infrastructure and port over existing EVM-based smart contracts.

These all are compelling reasons to build with the FVM. If you are interested in following along on what teams are building with the FVM, check out this non-exhaustive list. Also, review the Space Warp initiative to learn more about the program leading up to the launch of Filecoin’s Virtual Machine, including FVM-specific hackathons, grants, community leaderboards and acceleration programs. To familiarize with the technical details around the FVM consider visiting fvm.filecoin.io or watching oneofthemany videos introducing the technology.

Disclaimer: Personal views and not reflective of my employer nor should be treated as “official”. This information is intended to be used for informational purposes only. It is not investment advice. Although we try to ensure all information is accurate and up to date, occasionally unintended errors and misprints may occur.

[1]: Before March 14, the Filecoin Virtual Machine powered only so-called ‘native actors’. These built-in actors powered Filecoin’s core logic (e.g., computing and posting the proofs necessary to on-board and continuously verify storage onto the network) thus enabling storage deals and enforcing good behavior by the storage providers. Amending the functionality of these native actors requires the involvement of many stakeholders in the Filecoin community via the Filecoin Improvement Proposal (FIP) process. The complexity of this process limited the freedom to experiment, develop and deploy new functionalities on the Filecoin network.

[2]: The absence of better opportunities to more optimally allocate FIL in the Filecoin economy, may explain why the locking rate of Filecoin (38%) is lower than that of many other Layer-1 blockchains (often >60%)

As we’ve written about previously, Filecoin is building an economy of open data services. While today, Filecoin’s economy is primarily oriented around storage services, as other services (retrieval, compute) come online, the utility of the Filecoin network will compound as they all anchor in and can be triggeredfrom the same block space.

The Filecoin Virtual Machine (FVM) allows us to compose these services together, along with other on-chain services (e.g. financial services), to create more sophisticated offerings. This is similar to how the composability in Defi enables the construction of key financial markets services in a permissionless manner (e.g. auto investment capabilities (Yearn) which builds on liquidity pools like Curve and lending protocols like Compound). The FVM is an important milestone for Filecoin, as it allows anyone to build protocols to improve the Filecoin network and build valuable services for other participants. Smart contracts on Filecoin are unique in that they pair web3 offerings with real world services like storage and compute, provided by an open market.

In this blogpost, we’ll unpack a sample use case and its supporting components for the FVM, how these services might compose together, and the potential business opportunities behind them. One of the neat artifacts of what the FVM enables is for modularity between solutions, meaning components built for one protocol can be reused for others. While designing these solutions, hopefully builders (potentially you!) keep this in mind to maximize the customer set.

This is only a subset of the opportunities that the broader Filecoin community has put forward here, but the aim is to show how these services might intertwine and how the Filecoin economy might evolve.

Note: Over time, it’s likely that a number of these services will migrate to subnets via Interplanetary Consensus — but for this blogpost we want to paint a more detailed picture of what the Filecoin economy might look like early on.

The rest of the blog is laid out as follows:

Motivating Use Case – Perpetual Storage

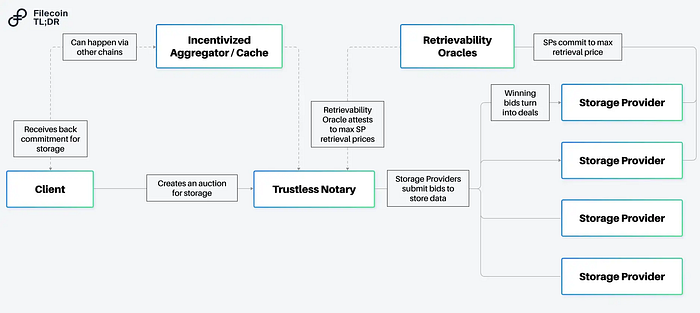

Managing Flows of Data – Aggregator / Caching Nodes – Trustless Notaries – Retrievability Oracles

Perpetual storage is a useful jumping point — as it motivates a number of the other services (both infrastructure and economic) in the network. Permanent storage (which we’ve argued previously is a subset of perpetual storage) is a market valued at ~$300 million.

The basic goal of perpetual storage is straightforward: enable users to specify terms for how their datasets should be stored (e.g. ensure there are always at least 10 copies of this data on the network) — without having to run additional infrastructure to manage repair or renewal of deals. As long as the funds exist to pay for storage services, the perpetual storage protocol should automatically incentivize the repair and restoration of any under-replicated dataset to meet the specified terms.

This tweet thread shares a mental model for how one might create and fund such a contract. In the simplest form, you can boil down a perpetual storage contract to a minimum set of requirements <cid, number of copies, USDC, FIL, rules for an auction>, and the primitives to verify proper execution. Filecoin’s proofs are critical — as they can tell us when data is under-replicated and allow us to trigger auctions to bring replication back to a minimum threshold.

In order to build the above, a number of services are required. While one protocol could try and solve for all the services required in a monolithic architecture, modular solutions would allow for re-use in other protocols. Below we’ll cover some of the middleware services that might exist to help enable the full end-to-end flow.

Managing the Flow of Data

A sample flow for how data may move across the Filecoin economy.

Aggregator / Caching Nodes

In our perpetual storage protocol, the client specifies some data that should be replicated. This leads to an interesting UX question — in many cases, users don’t want to have to wait for storage proofs to land on-chain to know the data will be stored and replicated. Instead, users might prefer to have their data persisted by an incentivized actor with guarantees that all other services will occur, similar to the role that data on-ramps play (like Estuary and NFT.Storage).

Note: One of the nice things about content addressing is that relying on incentivized actors is totally optional! Users wait for their data to land on-chain themselves if they’d like — or send their data to an incentivized network (as described here) that manages this onboarding process for them.

One solution to this UX question might be to design a protocol for an incentivized IPFS nodes operating with weaker storage guarantees to act as incentivized caches. These nodes might lock some collateral (to ensure good behavior, enact penalties if services are not rendered properly), and when data is submitted return a commitment to store the data Filecoin according to the specified requirements of the client. This commitment might include a merkle proof (showing the client’s data was included inside of a larger set of data that might be stored in aggregate), a max block height by which the deal would start, etc.

Revenue Model:One neat feature of this design for aggregator services is they can take small microtransactions on service on both sides — a small fee from clients (pricing the temporary storage costs, compute for aggregation, bandwidth costs, etc), and potentially an onboarding bounty from an auction protocol (an example described in the Trustless Notaries section below).

Trustless Notaries (Auction Protocols)

To actually make the deal on Filecoin, we might want to automate the process of using Filecoin Plus. Filecoin has two types of storage deals — verified deals and unverified deals. Verified deals refer to storage deals done via the Filecoin Plus program, and are advantageous for data clients as it leverages Filecoin’s network incentives to help reduce the cost of storage.

Today, Filecoin Plus uses DataCap (allocated by Notaries) to help imbue individual clients with the ability to store fixed amounts of data on the network. Notaries help add a layer of social trust to publicly verify that clients are authentic and prevent sybils from malicious actors. This works when clients are human — but it leaves an open question on how one can verify non-human (e.g. smart contract!) actors.

One solution would be to design a trustless notary. A trustless notary is a smart contract, where it would be economically irrational to attempt to sybil the deal-making process.

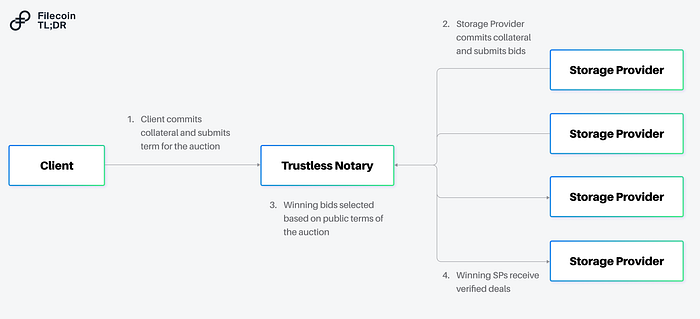

A basic flow of how a trustless notary interact with clients and storage providers.

What might this look like? A trustless notary might be an on-chain auction, where all participants (clients, storage providers) are required to lock some collateral (proportional to the onboarding rate) to participate. When the auction is run, storage providers can submit valid bids (even negative ones!) accommodating the requirements of the client. By running an auction via a smart contract — everyone can verify that the winning bidder(s) came from a transparent process. Economic collateral (both from the clients and storage providers) can be used to disincentivize malicious actors and ensure closed auctions result in on-chain deals. The auction process might also allow for more sophisticated negotiations between a prospective client and storage provider — not just on the terms of the deal, but on the structure of the payment as well. A client looking to control costs might offer a payment in fiat (to cover a storage provider’s opex) along with a loan in Filecoin (and in return expect a large share of the resulting block rewards).

Revenue Model: For running the auction, the notary maintainer might collect some portion of fees for the deal clearing, collect a fee on locked collateral (e.g. if staked FIL is used as the collateral some slice of the yield), or some combination of both. One nice artifact about running a transparent auction is it can also allow for negative prices for storage (which can be used to fund an insurance fund for datasets, bounties for teams that help onboard new clients, distributed to tokenholders who participate in governance of the trustless notary, etc).

Note: Trustless notaries (if designed correctly) have a distinct advantage of being permissionless — where they can support any number of use cases that might not want humans in the loop (e.g. ETL pipelines that want to automatically store derivative datasets). Today, 393 PiB of data have been stored via verified deals.

In our perpetual storage use case, we’d likely want to be able to leverage the trustless notary to trigger the deal renewals and auctions any time a dataset is under replicated. On the first iteration, this means that storage providers might grab the data out of the caching nodes and on subsequent iterations from other storage providers who have copies of the data.

Retrievability Oracles

For both the deals struck by the trustless notaries, as well as for the caching done by the aggregators — we need to ensure data is properly transferred and protect clients against price gouging. One solution to this problem are retrievability oracles.

Retrievability oracles are consortiums that allow a storage provider to commit to a maximum retrieval price for the data stored. The basic mechanism is as follows:

When striking a deal with a client, a storage provider additionally can commit to retrieval terms.

In doing so, the storage provider locks collateral with the retrievability oracle along with relevant commitment (e.g. max price to charge per GiB for some duration).

In normal operation, the client and the storage provider continue to store and retrieve data as normal.

In the event the storage provider refuses to serve data (against whatever terms previously agreed), the client can appeal to the retrievability oracle who can request the data from the storage provider. → If the storage provider serves the data to the oracle, the data is forwarded to the client. → If the storage provider doesn’t serve the data, the storage provider is slashed.

Revenue Model: For running the retrieval oracles, the consortium may collect fees (either from storage providers for using the service, fees for accepting different forms of collateral, yield from staked collateral, or perhaps upon retrieval of data on behalf of the client).

By including a retrievability oracle in this loop, we can ensure incentives exist to proper transfer of data at the relevant points of the lifecycle of our perpetual storage protocol.

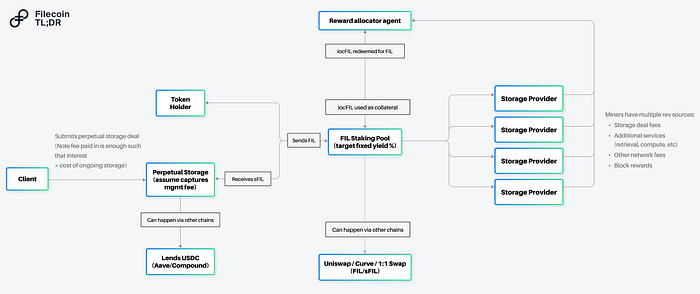

Building the Economic Loop

With all of the above, we’ve effectively created incentivized versions of the relevant components for the dataflows. Now with this out of the way, it’s worthwhile to focus on the economic flows and how we can ensure that our perpetual storage protocol can fully fund the operations above.

A sample view on the economic flows for enabling perpetual storage. Note other DeFi primitives might help mitigate risk and volatility (e.g. options, perpetuals)

Aside from the initial onboarding costs, the remainder of the costs will come down to storage and repairs. While there are many approaches to calculating the upfront “price”, a conservative strategy will likely involve the perpetual storage protocol generating revenue in the same currencies (fiat, Filecoin) as the liabilities incurred due to storage (i.e the all-in costs of storage). This approach relies on the fact that storage on Filecoin has two types of (fairly predictable) expenses:

The Filecoin portion (the cost of a loan in FIL, the FIL required to send messages over the network) and

The fiat portion (the cost of the harddrive, running the proofs, electricity)

A perpetual storage protocol that builds an endowment in the same mix of currencies as its liabilities can ensure that its costs are fully covered despite the volatility of a single token (as might be the case if the endowment was backed by a single currency). In addition, by putting the capital to work and generating yield, the upfront cost for the client can be reduced.

Staking

To generate yield in Filecoin, the natural place to focus would be on the base protocol of Filecoin itself. Storage providers are required to lock FIL as collateral in order to onboard capacity, and by running Filecoin’s consensus, they earn a return in the form of block rewards and transaction fees. The collateral requirements for the now ~4,000 storage providers on the Filecoin network create a high demand to borrow the FIL token. FIL staking would allow a holder of Filecoin to lend FIL — locking their capital with a storage provider and receiving yield by sharing in the rewards of the storage provider.

Today, programs exist with companies like Anchorage, Darma, and Coinlist to deploy Filecoin with some storage providers, but these programs can service only a subset of the storage providers and don’t support protocols (such as our perpetual storage protocol) that might be looking to generate yield.

Staking protocols can uniquely solve this problem — allowing for permissionless aggregation (allowing smart contracts to generate yield), and deployment of Filecoin to all storage providers directly on-chain. Similar to Lido or Rocketpool in Ethereum, these protocols could also create tokenized representations of the yield bearing versions of Filecoin — further allowing these tokenized representations to be used as collateral in other services (e.g. the trustless notary, retrievability oracles listed above).

Revenue Model: Staking protocols can monetize in a number of ways — including taking a percentage of the yield generated from deployed assets.

Note: Today, roughly 34% of the circulating supply of Filecoin is locked as collateral, less than half of some proof of stake networks (e.g. 69% for Solana, 71% for Cardano).

Cross Chain Messaging

The other portion of the storage costs (the fiat denominated portion) will need to generate yield — and while it makes sense that some of these solutions might be deployed on the FVM, it’s worth discussing the areas where DeFi in other ecosystems might be used to fund operations on Filecoin.

Cross chain messaging could connect the Filecoin economy to other ecosystems allowing perpetual storage protocols to create pools for their non-Filecoin assets (e.g. USDC) on other networks. This would allow these protocols to generate yield on stablecoins in deeper markets (e.g. Ethereum) and bridge back portions as needed to Filecoin when renewing deals. Perpetual storage protocols can offer differentiated sources of recurring demand for these lending protocols, as they likely will have a much more stable profile in terms of their deployment capital given their cost structure — similar to pension funds in the traditional economy.

Given an early source of demand for many perpetual storage protocols include communal data assets (e.g. NFTs, DeSci datasets) which primarily involve on-chain entities, it’s likely that over time we’ll see steady demand for these cross chain services. For cross chain messaging protocols, this offers a unique opportunity to capture value between the “trade” of these different economies — as services are rendered on either side.

Automated Market Makers (AMMs)

One last component worth mentioning in the value flow for our perpetual storage protocol is a need for AMMs. The protocols listed above offer solutions for yield generation, but at the moment of payment conversion of assets will likely need to happen (e.g. converting from a staked representation of Filecoin to Filecoin itself). This is where AMMs can help!

Outside of helping convert staked representations of Filecoin to Filecoin, AMMs can also be useful for allowing perpetual storage protocols to accept multiple types of currencies for payment (e.g. allowing ETH or SOL to be swapped into the appropriate amounts of FIL and stablecoins to fund the perpetual storage protocol). These conversions might happen on other chains as well — but similar to the traditional economy, it’s likely that over time we’ll see trade balances emerge between these economies and swaps to happen on both sides.

Conclusion

These examples are a subset of the use cases and business models that the FVM enables. While I focused on tracing the flow of data and value through the Filecoin economy, it’s worth underscoring this is just a single use case — many of these components could be re-used for other data flows as well. Given all services require remuneration, these naturally will tie to economic flows as well.

As Filecoin launches its retrieval markets and compute infrastructure, the network will support more powerful interactions — as well as creating new business opportunities to connect services to support higher order use cases. Furthermore, as more primitives are built out on the base layer of Filecoin (e.g. verifiable credentials around the greenness of storage providers, certifications for HIPAA compliance), you can imagine permutations of each of the base primitives built above allowing for more control at the user level about the service offerings they wish to consume (e.g. a perpetual storage protocol that will only allow green storage providers to participate in storing their data).The FVM dramatically increases the design space for developers looking to build on the hardware and services in the Filecoin economy — and can hopefully also provide tangible benefits for all of web3, allowing for existing protocols and services to now be connected to a broader set of use cases.Disclaimer: Personal views and not reflective of my employer nor should be treated as “official”. This information is intended to be used for informational purposes only. It is not investment advice. Although we try to ensure all information is accurate and up to date, occasionally unintended errors and misprints may occur.Special thanks to @duckie_han for helping shape this.