At the latest Filecoin Developer Summit (FDS), Nicola Greco(of FilOz) introduced a vision to evolve Filecoin’s decentralized cloud services: Filecoin Web Services (FWS). FWS aims to provide a framework for deploying composable cloud services – allowing new protocols to bootstrap into a shared marketplace of offerings, all composable with each other.

Expanding Beyond Proof of Replication: Expanding the functionality of Filecoin

To understand FWS, it’s useful to first recap how the existing service offerings exist inside the Filecoin network.

The core storage offering, Proof of Replication (PoRep), allows storage providers to use proofs over uniquely encoded data to show that they are still in possession of specific pieces of data. Filecoin uses PoRep both for storage and for consensus – this requires higher security parameters, and therefore makes Filecoin’s base storage offering akin to cold storage. This makes Filecoin’s base offering ideal for datasets that might have a need for strong guarantees around uniqueness and existence but can accept slower access times.

Furthermore, because Filecoin launched prior to the FVM, much of the onchain tooling (e.g. to set up and maintain storage deals, to enable payments) exist as “system actors” or non-programmable functions on the network. This means many of those functions were built to support the original storage functions on the network – but for any evolution would require a full network upgrade in order to modify or support new functionality.

However, as more storage on-ramp’s pushed into building storage solutions for customers, it became clear that there was a need for more storage offerings over and above the base offering from Filecoin. As a result, new types of proofs (such as proof of data possession) have been proposed to run on the Filecoin network – allowing for more use cases to be natively supported.

In designing these new offerings to sit on top of Filecoin, it became clear that many of these new proof offerings would need generalized versions of the onchain tooling that exists as “system actors” – such as payment rails. Rather than having many systems independently evolve their own architecture (and risk losing composability), a new proposal was put forward to focus on building modular, composable systems via FWS.

Introducing Filecoin Web Services: A Modular Approach to Cloud Services

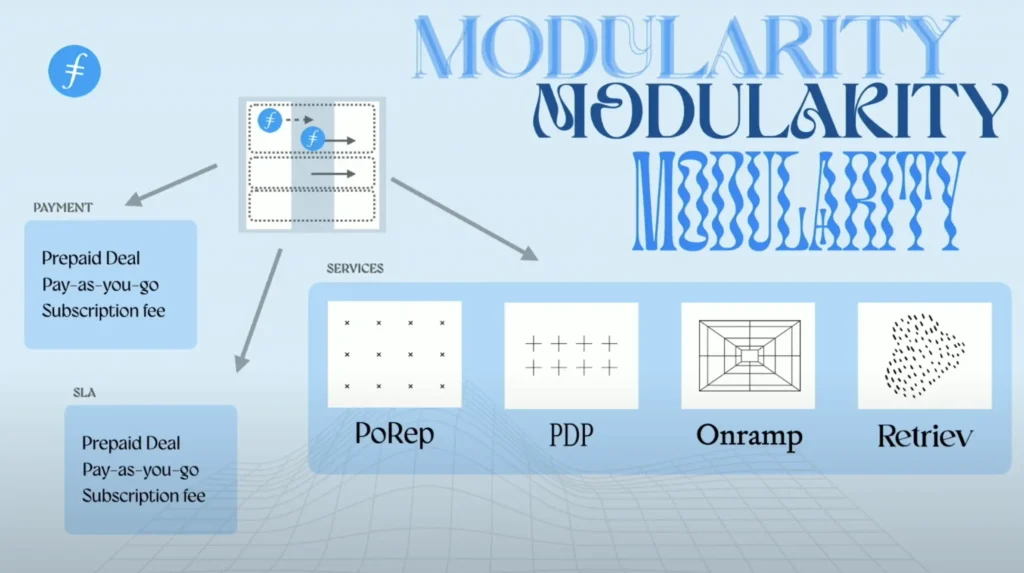

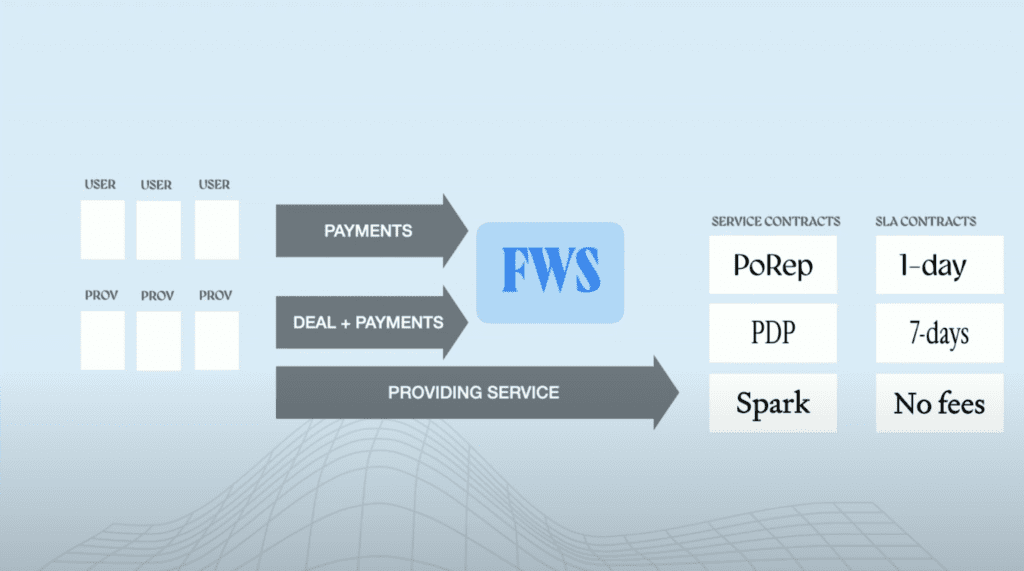

At the core of Greco’s vision is the concepts of modularity and reuse. If each new service were to build their entire protocol from scratch, they’d need to develop work ranging from deal management to escrow and SLA enforcement – which would lead to a high barrier to entry for new services. FWS proposes a unified protocol that standardizes these components, allowing developers to focus on building specific services rather than recreating the entire stack.

FWS would serve as a thin, opinionated layer that manages payments, collateral, deal structuring, and SLA enforcement across various services. This standardization would enable seamless integration of new services, whether they are storage-related like PDP and retrieval services or entirely new offerings like markets for zk-SNARK proofs or AI-based computations. By providing a common framework, FWS would reduce complexity, lower development costs, and increase the rate of development for building within the Filecoin ecosystem.

The Power of a Unified Marketplace: Enhancing Efficiency and Accessibility

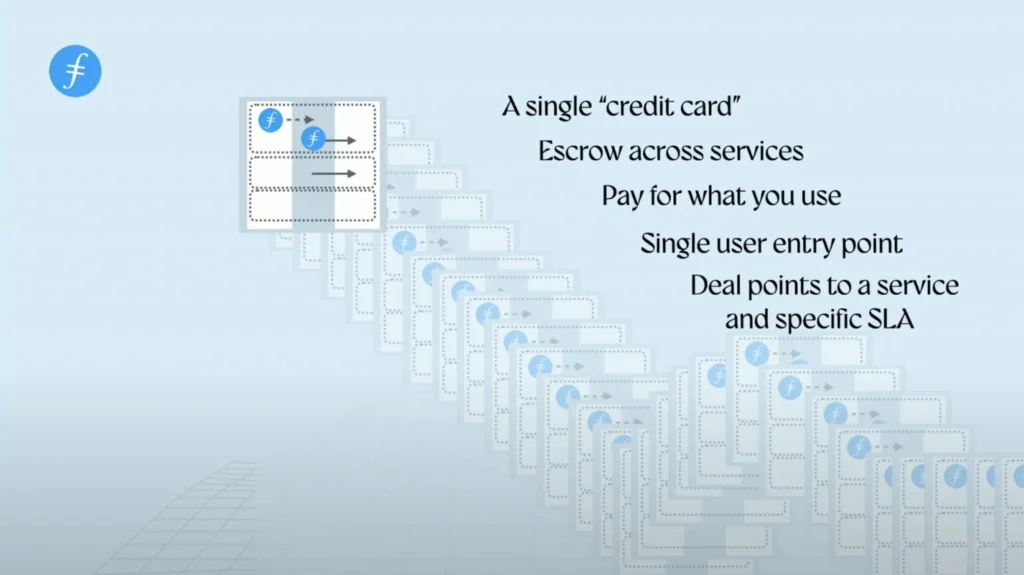

One of the key benefits of FWS is its potential to streamline the user experience. Without FWS, users would need to lock tokens in multiple smart contracts to access different services, leading to inefficiencies in collateral management and prepayment and increase users’ cost. FWS envisions a single entry point where users can determine how they’d like to pay – prepaid or pay-as-you-go – with the same rails being usable by multiple services. This model mirrors the convenience of traditional cloud services, where users simply provide a payment method and are periodically billed.

Moreover, by consolidating financial management into a single contract, FWS would improve collateral efficiency and reduce the overhead associated with managing multiple service contracts. This would also allow utilization of one service to enable credit in other services – allowing a credit history to be built up across disparate protocols. This approach not only simplifies the user experience but also enhances the overall liquidity and flexibility of the Filecoin ecosystem.

A Vision for the Future: FWS as a Distribution Layer for Decentralized Services

Looking ahead, Greco envisions FWS not just as a tool for enhancing Filecoin’s storage capabilities but as a broader distribution layer for decentralized services. As the ecosystem grows, FWS could facilitate the integration of multiple networks and protocols, creating a cohesive marketplace for storage, compute, bandwidth, and other services. This would position Filecoin at the center of a vibrant, interconnected ecosystem, driving innovation and adoption across the decentralized web. By offering a marketplace for diverse services such as zero-knowledge proof generation, decentralized compute, FWS could position Filecoin as a leading platform in the decentralized web, supporting a wide array of applications beyond storage.

To understand more about FWS, watch the full keynote by Nicola Greco on Youtube

Many thanks to Jonathan Victor for reviewing and providing valuable insights to this piece.

Disclaimer: This information is for informational purposes only and is not intended to constitute investment, financial, legal, or other advice. This information is not an endorsement, offer, or recommendation to use any particular service, product, or application.

Editor’s Note: This blogpost is a repost of the original content published on 5 March 2024, by Bidhan Roy and Marcos Villagra from Bagel. Founded in 2023 by CEO Bidhan Roy, Bagel is a machine learning and cryptography research lab building a permissionless, privacy-preserving machine learning ecosystem. This blogpost represents the independent view of these authors, whom have given their permission for this re-publication.

Trillion-dollar industries are unable to leverage their immensely valuable data for AI training and inference due to privacy concerns. The potential for AI-driven breakthroughs—genomic secrets that could cure diseases, predictive insights to eliminate supply chain waste, and chevrons of untapped energy sources—remain locked away. Privacy regulations also closely guard this valuable and sensitive information.

To propel human civilization forward in energy, healthcare, and collaboration, it is crucial to enable AI systems that train and generate inference on data while maintaining full end-to-end privacy. At Bagel, pioneering this capability is our mission. We believe accessing a fundamental resource like knowledge, for both human-driven and autonomous AI, should not entail a compromise on privacy.

We have applied and experimented with almost all the major privacy-preserving machine learning (PPML) mechanisms. Below, we share our insights, our approach, and some research breakthroughs.

And if you’re in a rush, we have a TLDR at the end.

Privacy-preserving Machine Learning (PPML)

Recent advances in academia and industry have focused on incorporating privacy mechanisms into machine learning models, highlighting a significant move towards privacy-preserving machine learning (PPML). At Bagel, we have experimented with all the major PPML techniques, particularly those post differential privacy. Our work, positioned at the intersection of AI and cryptography, draws from the cutting edge in both domains.

First, we will delve into each of these, examining their advantages and drawbacks. In subsequent posts, we will describe Bagel’s approach to data privacy, which addresses and resolves the challenges associated with the existing solutions.

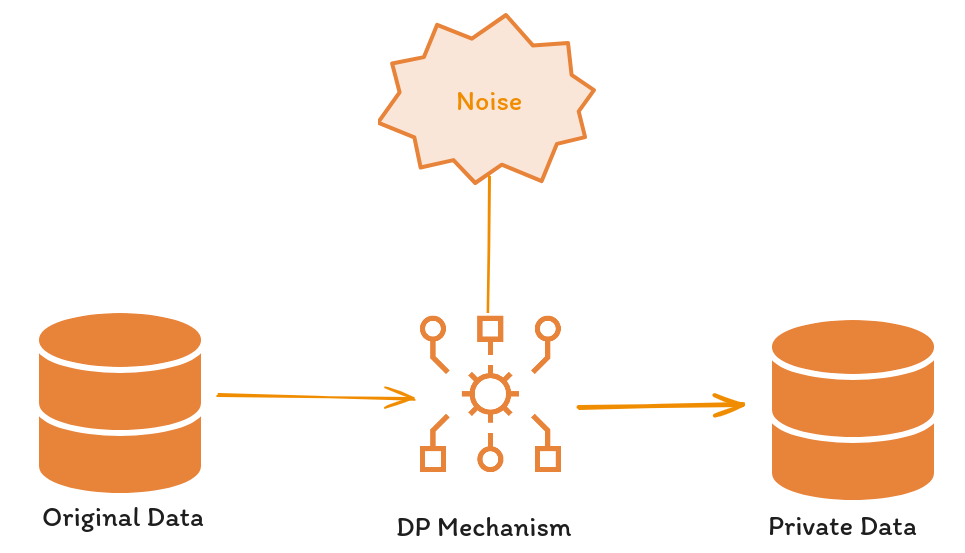

Differential Privacy (DP)

One of the first and most important techniques with a mathematical guarantee for incorporating privacy into data is differential privacy or DP (Dwork et al. 2006), addressing the challenges faced by earlier methods with a quantifiable privacy definition.

DP ensures that a randomized algorithm, A, maintains privacy across datasets D1 and D2—which differ by a single record—by keeping the probability of A(D1) and A(D2) generating identical outcomes relatively unchanged. This principle implies that minor dataset modifications do not significantly alter outcome probabilities, marking a pivotal advancement in data privacy.

The application of DP in machine learning, particularly in neural network training and inference, demonstrates its versatility and effectiveness. Notable implementations include adapting DP for supervised learning algorithms by integrating random noise at various phases: directly onto the data, within the training process, or during inference, as highlighted by Ponomareva et al. (2023) and further references.

The balance between privacy and accuracy in DP is influenced by the noise level: greater noise enhances privacy at the cost of accuracy, affecting both inference and training stages. This relationship was explored by Abadi et al. in (2016) through the introduction of Gaussian noise to the stochastic gradient descent (DP-SGD) algorithm, observing the noise’s impact on accuracy across the MNIST and CIFAR-10 datasets.

An innovative DP application, Private Aggregation of Teacher Ensembles (PATE) by Papernot et al. in (2016), divides a dataset into disjoint subsets, training networks on each without privacy, termed as teachers. These networks’ aggregated inferences, subjected to added noise for privacy, inform the training of a student model to emulate the teacher ensemble. This method also underscores the trade-off between privacy enhancement through noise addition and the resultant accuracy reduction.

Further studies affirm that while privacy can be secured with little impact on execution times (Li et a. 2015), stringent privacy measures can obscure discernible patterns essential for learning (Abadi et al. 2016). Consequently, a certain level of privacy must be relinquished in DP to facilitate effective machine learning model training, illustrating the nuanced balance between privacy preservation and learning efficiency.

Pros of Differential Privacy

The advantages of using DP are:

Effortless. Easy to implement into algorithms and code.

Algorithm independence. Schemes can be made independent of the training or inference algorithm.

Fast. Some DP mechanisms have shown to have little impact on the execution times of algorithms.

Tunable privacy. The degree of desired privacy can be chosen by the algorithm designer.

Cons of Differential Privacy

Access to private data is still necessary. Teachers in the PATE scheme must have full access to the private data (Papernot et al. 2016) in order to train a neural network. Also, the stochastic gradient descent algorithm based on DP only adds noise to the weight updates and needs access to private data for training (Abadi et al. 2016).

Privacy-Accuracy-Speed trade-off on data. All implementations must sacrifice some privacy in order to get good results. If there is no discernable pattern in the input, then there is nothing to train (Feyisetan et al. 2020). The implementation of some noise mechanisms can impact execution times, necessitating a balance between speed and the goals of privacy and accuracy.

Zero-Knowledge Machine Learning (ZKML)

A zero-knowledge proof system (ZKP) is a method allowing a prover P to convince a verifier V about the truth of a statement without disclosing any information apart from the statement’s veracity. To affirm the statement’s truth, P produces a proof π for V to review, enabling V to be convinced of the statement’s truthfulness.

Zero-Knowledge Machine Learning (ZKML) is an approach that combines the principles of zero-knowledge proofs (ZKPs) with machine learning. This integration allows machine learning models to be trained and to infer with verifiability.

For an in-depth examination of ZKML, refer to the work by Xin et al. in (2023). Below we provide a brief explanation that focuses on the utilization of ZKPs for neural network training and inference.

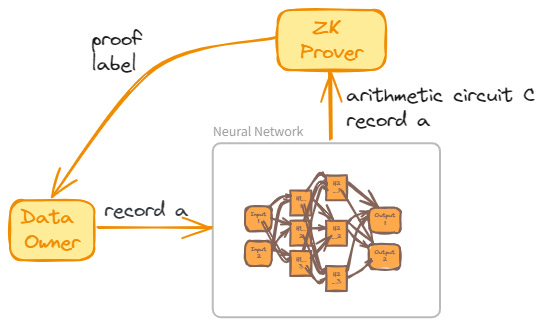

ZKML Inference

Consider an unlabeled dataset A and a pretrained neural network N tasked with labeling each record in A. To generate a ZK proof of N‘s computation during labeling, an arithmetic circuit C representing N is required, including circuits for each neuron’s activation function. Assuming such a circuit C exists and is publicly accessible, the network’s weights and a dataset record become the private and public inputs, respectively. For any record a of A, N‘s output is denoted by a pair (l,π), where l is the label and π is a zero-knowledge argument asserting the existence of specific weights that facilitated the labeling.

This model illustrates how ZK proves the accurate execution of a neural network on data, concealing the network’s weights within a ZK proof. Consequently, any verifier can be assured that the executing agent possesses the necessary weights.

ZKML Training

ZKPs are applicable during training to validate N‘s correct execution on a labeled dataset A. Here, A serves as the public input, with an arithmetic circuit C depicting the neural network N. The training process requires an additional arithmetic circuit to implement the optimization function, minimizing the loss function. For each training epoch i, a proof π_i is generated, confirming the algorithm’s accurate execution through epochs 1 to i-1, including the validity of the preceding epoch’s proof. The training culminates with a compressed proof π, proving the correct training over dataset A.

The explanation above illustrates that during training, the network’s weights are concealed to ensure that the training is correctly executed on the given dataset A. Additionally, all internal states of the network remain undisclosed throughout the training process.

Pros of ZKML

The advantages of using ZKPs with neural networks are:

Privacy of model weights. The weights of the neural network are never revealed during training or inference in any way. The weights and the internal states of the network algorithm are private inputs for the ZKP.

Verifiability. The proof certifies the proper execution of training or inference processes and guarantees the accurate computation of weights.

Trustlessness. The proof and its verification properties ensure that the data owner is not required to place trust in the agent operating the neural network. Instead, the data owner can rely on the proof to confirm the accuracy of both the computation and the existence of correct weights.

Cons of ZKML

The disadvantages of using ZKPs with neural networks are:

No data privacy. The agent running the neural network needs access to the data in order to train or do inference. Data is considered a parameter that is publicly known to the data owner and the prover running the neural network (Xing et al. 2023).

No privacy for the model’s algorithm. In order to create a ZK proof, the algorithm of the entire neural network should be publicly known. This includes the activation functions, the loss function, optimization algorithm used, etc (Xing et al. 2023).

Proof generation of an expensive computation. Presently, the process of generating a ZK proof is computationally demanding—-see for example this report on the computation times of ZK provers. Creating a proof for each epoch within a training algorithm can exacerbate the computational burden of an already resource-intensive task.

Federated Learning (FL)

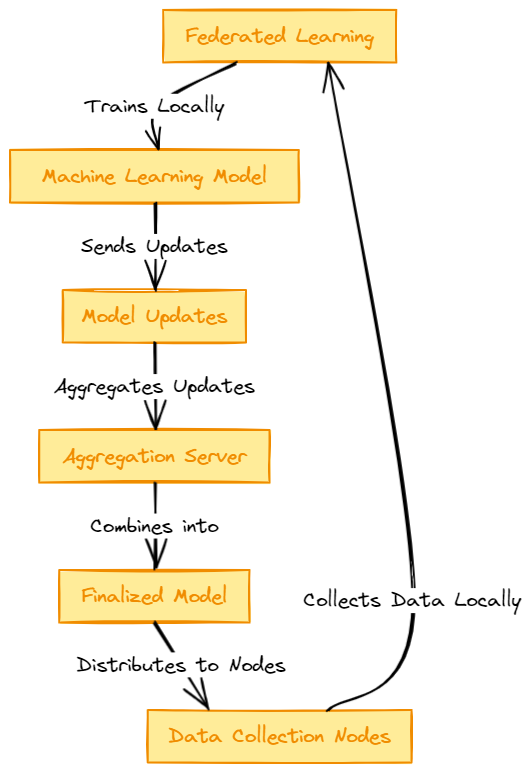

In Federated Learning or FL we look to train a global model using a dataset that is distributed in multiple servers with local data samples but without each server sharing their local data.

In FL there is a global objective function that is being optimized which is defined as

𝑓(𝑥1,…,𝑥𝑛)=1𝑛∑𝑖=1𝑛𝑓𝑖(𝑥𝑖),\(f(x_1,\dots,x_n)=\frac 1 n \sum_{i=1}^n f_i(x_i),\)

where n is the number of servers, each variables is the set of parameter as viewed by the server i, and each function is a local objective function of server i. FL tries to find the best set of values that optimizes f.

The figure below shows the general process in FL.

Initialization. An initial global model is created and distributed by a central server to all other servers.

Local training. Each server trains the model using their local data. This ensures data privacy and security.

Model update. After training, each server shares with the central server their local updates like gradients and parameters.

Aggregation. The central server receives all local updates and aggregates them into the global model, for example, using averaging.

Model distribution. The updated model is distributed again with local servers and the previous steps are repeated until a desired level of performance is achieve by the global model.

Since local servers never share their local data, FL guarantees privacy over that data. However, the model being constructed is shared among all parties, and hence, its structure and set of parameters are not hidden.

Pros of FL

The advantages of using FL are:

Data privacy. The local data on the local servers are never shared. All computations are done locally, and there is no need of communication between them.

Distributed computing. The creation of the global model is distributed among local servers, thereby parallelizing a resource-intensive computation. Thus, FL is considered a distributed machine learning framework (Xu et al. 2021).

Cons of FL

The disadvantages of using FL are:

Model is not private. The global model is shared among each local server in order to do their computations locally. This includes the aggregated weights and gradients at each step of the FL process. Thus, each local server is aware of the entire architecture of the global model (Konečný et al. 2016).

Data leakage. Recent research indicates that data leakage remains a persistent issue, notably through mechanisms such as gradient sharing—see for example Jin et al. (2022). Consequently, FL cannot provide complete assurances of data privacy.

Trust. Since no proofs are generated in FL, every party involved in the process need to be trusted that their computation and parameters were computed as expected (Gao et al. 2023).

Fully Homomorphic Encryption (FHE)

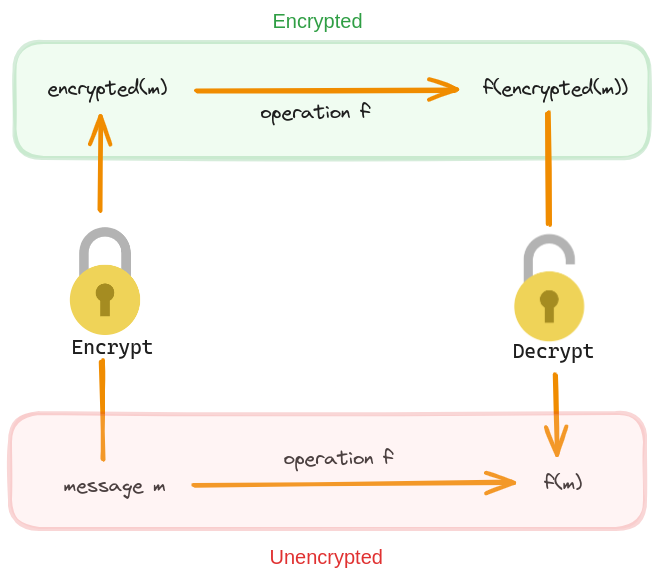

At its core, homomorphic encryption permits computations on encrypted data. By “homomorphic,” we refer to the capacity of an encryption scheme to allow specific operations on ciphertexts that, when decrypted, yield the same result as operations performed directly on the plaintexts.

Consider a scenario with a secret key k and a plaintext m. In an encryption scheme (E,D), where E and D represent encryption and decryption algorithms respectively, the condition D(k,E(k,m))=m must hold. A scheme (E,D) is deemed fully homomorphic if for any key k and messages m, the properties E(k,m+m’)=E(k,m)+E(k,m’) and E(k,m*m’)=E(k,m)* E(k,m’) are satisfied, with addition and multiplication defined over a finite field. If only one operation is supported, the scheme is partially homomorphic. This definition implies that operations on encrypted data mirror those on plaintext, crucial for maintaining data privacy during processing.

In plain words, if we have a fully homomorphic encryption scheme, then operating over the encrypted data is equivalent to operating over the plaintext. We will write FHE to refer to a fully homomorphic encryption scheme. The figure below shows how an arbitrary homomorphic operation works over a plaintext and ciphertext.

The homomorphic property of FHE makes it invaluable in situations where data must remain secure while still being used for computations. For instance, if we possess sensitive data and require a third party to perform data analysis on it, we can rely on FHE to encrypt the data. This allows the third party to conduct analysis on the encrypted data without the need for decryption. The mathematical properties of FHE guarantee the accuracy of the analysis results.

FHE Inference

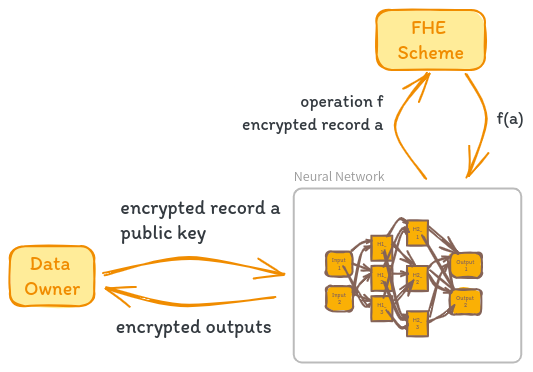

Fully Homomorphic Encryption (FHE) can be used to perform inference in neural networks while preserving data privacy. Let’s consider a scenario where N is a pretrained neural network, A is a dataset, and (E,D) is an asymmetric FHE scheme. The goal is to perform inference on a record a of A without revealing the sensitive information contained in a to the neural network.

The inference process using FHE begins with encryption. The data owner encrypts the record a using the encryption algorithm E with the public key public_key, obtaining the encrypted record a’ = E(public_key, a).

Next, the data owner sends the encrypted record a’ along with public_key to the neural network N. The neural network N must have knowledge of the encryption scheme (E,D) and its parameters to correctly apply homomorphic operations over the encrypted data a’. Any arithmetic operation performed by N can be safely applied to a’ due to the homomorphic properties of the encryption scheme.

One challenge in using FHE for neural network inference is handling non-linear activation functions, such as sigmoid and ReLU, which involve non-arithmetic computations. To compute these functions homomorphically, they need to be approximated by low-degree polynomials. The approximations allow the activation functions to be computed using homomorphic operations on the encrypted data a’.

After applying the necessary homomorphic operations and approximated activation functions, the neural network N obtains the inference result. It’s important to note that the inference result is still in encrypted form, as all computations were performed on encrypted data.

Finally, the encrypted inference result is sent back to the data owner, who uses the private key associated with the FHE scheme to decrypt the result using the decryption algorithm D. The decrypted inference result is obtained, which can be interpreted and utilized by the data owner.

By following this inference process, the neural network N can perform computations on the encrypted data a’ without having access to the original sensitive information. The FHE scheme ensures that the data remains encrypted throughout the inference process, and only the data owner with the private key can decrypt the final result.

It’s important to note that the neural network N must be designed and trained to work with the specific FHE scheme and its parameters. Additionally, the approximation of non-linear activation functions by low-degree polynomials may introduce some level of approximation error, which should be considered and evaluated based on the specific application and accuracy requirements.

FHE Training

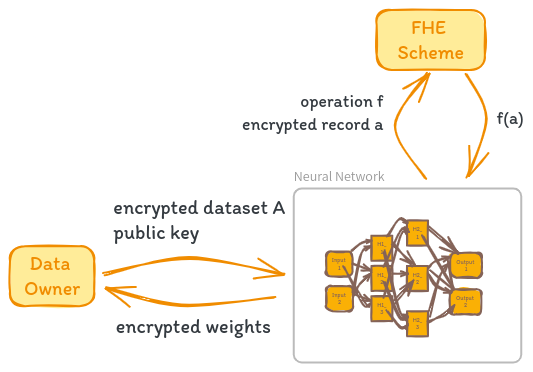

The process of training a neural network using Fully Homomorphic Encryption (FHE) is conceptually similar to performing inference, but with a few key differences. Let’s dive into the details.

Imagine we have an untrained neural network N and an encrypted dataset A’ = E(public_key, A), where E is the encryption function and public_key is the public key of an asymmetric FHE scheme. Our goal is to train N on the encrypted data A’ while preserving the privacy of the original dataset A.

The training process unfolds as follows. Each operation performed by the network and the training algorithm is executed on each encrypted record a’ of A'. This includes both the forward and backward passes of the network. As with inference, any non-arithmetic operations like activation functions need to be approximated using low-degree polynomials to be compatible with the homomorphic properties of FHE.

A fascinating aspect of this approach is that the weights obtained during training are themselves encrypted. They can only be decrypted using the private key of the FHE scheme, which is held exclusively by the data owner. This means that even the agent executing the neural network training never has access to the actual weight values, only their encrypted counterparts.

Think about the implications of this. The data owner can outsource the computational heavy lifting of training to a third party, like a cloud provider with powerful GPUs, without ever revealing their sensitive data. The training process operates on encrypted data and produces encrypted weights, ensuring end-to-end privacy.

Once training is complete, the neural network sends the collection of encrypted weights w’ back to the data owner. The data owner can then decrypt the weights using his private key, obtaining the final trained model. He is the sole party capable of accessing the unencrypted weights and using the model for inference on plaintext data.

There are a few caveats to keep in mind. FHE operations are computationally expensive, so training a neural network with FHE will generally be slower than training on unencrypted data.

Pros of FHE

The advantages of using FHE are:

Data privacy. Third-party access to encrypted private data is effectively prevented, a security guarantee upheld by the assurances of FHE and lattice-based cryptography(Gentry 2009).

Model privacy. Training and inference processes are carried out on encrypted data, eliminating the need to share or publicize the neural network’s parameters for accurate data analysis.

Effectiveness. Previous studies have demonstrated that neural networks operating on encrypted data using FHE maintain their accuracy—see for example Nandakumar et al. (2019) and Xu et al. (2019). Therefore, we can be assured that employing FHE for training and inference processes will achieve the anticipated outcomes.

Quantum resistance. The security of FHE, unlike other encryption schemes, is grounded in difficult problems derived from Lattice theory. These problems are considered to be hard even for quantum computers (Regev 2005), thus offering enhanced protection against potential quantum threats in the future.

Cons of FHE

The disadvantages of using FHE are:

Verifiability. FHE does not offer proofs of correct encryption nor correct computation. Hence, we must rely on trust that the data intended for encryption is indeed the correct data (Viand et al. 2023).

Speed. Relative to conventional encryption schemes, FHE is still considered to be slow during parameter setups, encryption and decryption algorithms (Gorantala et al. 2023).

Memory requirements. The number of weights that need to be encrypted are proportional to the size of the network. Even for small networks, the RAM memory requirements are in the order of gigabytes (Chen et al. 2018), (Nandakumar et al. 2019).

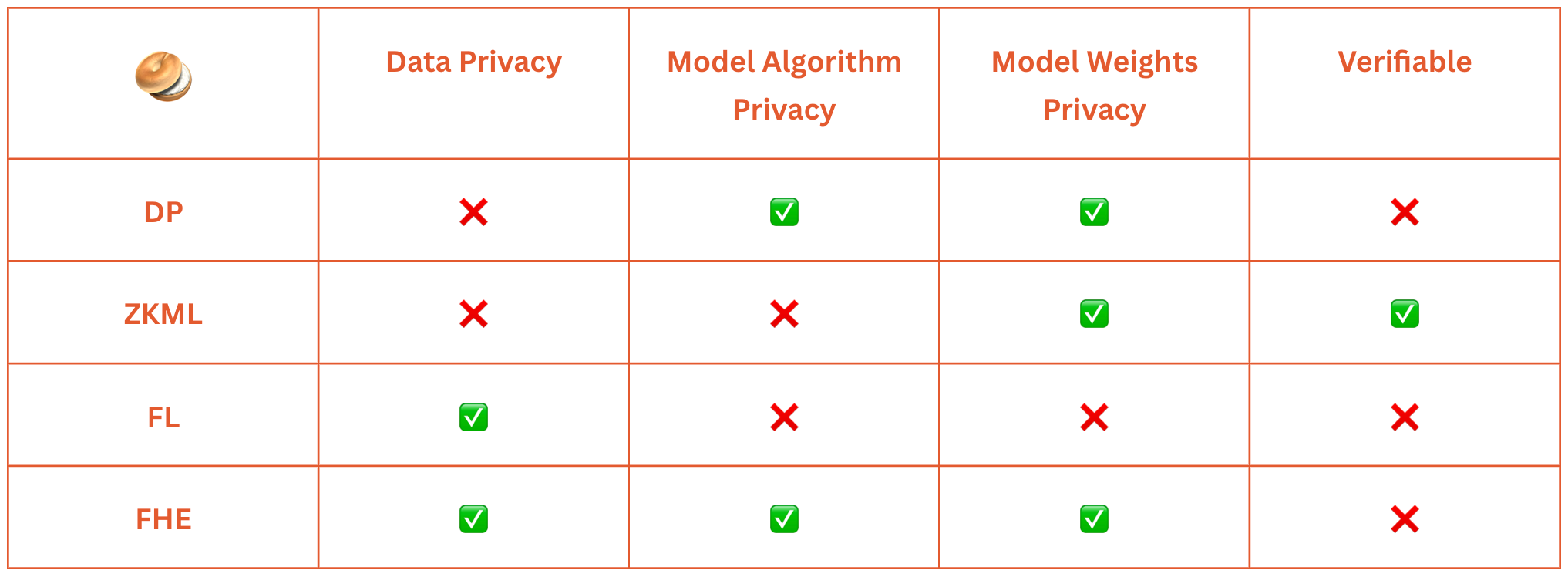

We examined the four most widely used privacy-preserving techniques in machine learning, focusing on neural network training and inference. We evaluated these techniques across four dimensions: data privacy, model algorithm privacy, model weights privacy, and verifiability.

Data privacy considers the model owner’s access to private data. Differential privacy (DP) and zero-knowledge machine learning (ZKML) require access to private data for training and proof generation, respectively. Federated learning (FL) enables training and inference without revealing data, while fully homomorphic encryption (FHE) allows computations on encrypted data.

Model algorithm privacy refers to the data owner’s access to the model’s algorithms. DP does not require algorithm disclosure, while ZKML necessitates it for proof generation. FL distributes algorithms among local servers, and FHE operates without accessing the model’s algorithms.

Model weights privacy concerns the data owner’s access to the model’s weights. DP and ZKML keep weights undisclosed or provide proofs of existence without revealing values. FL involves exchanging weights among servers for decentralized learning, contrasting with DP and ZKML’s privacy-preserving mechanisms. FHE enables training and inference on encrypted data, eliminating the need for model owners to know the weights.

Verifiability refers to the inherent capabilities for verifiable computation. ZKML inherently provides this capability. DP, FL, and FHE would not provide similar levels of integrity assurance.

The table below summarizes our findings:

What’s Next 🥯

At Bagel, we recognize that existing privacy-preserving machine learning solutions fall short in providing end-to-end privacy, scalability, and strong trust assumptions. To address these limitations, our team has developed a novel approach based on a modified version of homomorphic encryption (FHE).

Our pilot results are extremely promising, indicating that our solution has the potential to revolutionize the field of privacy-preserving machine learning. By leveraging the strengths of homomorphic encryption and optimizing its performance, we aim to deliver a scalable, trustworthy, and truly private machine learning framework.

We believe that our work represents a paradigm shift in the way machine learning is conducted, ensuring that the benefits of AI can be harnessed without compromising user privacy or data security. As we continue to share more about our approach, we invite you to follow our progress by subscribing to the Bagel blog.

For more thought pieces from Bagel, follow out their blog here.

To stay updated on the latest Filecoin happenings, follow the @Filecointldr handle.

Disclaimer: This information is for informational purposes only and is not intended to constitute investment, financial, legal, or other advice. This information is not an endorsement, offer, or recommendation to use any particular service, product, or application.

The Decentralized Storage space is rapidly evolving. Filecoin is at an important moment – and in this blog we propose both areas for the ecosystem to double down on and ways we can track that progress. It is by no means exhaustive, but written from the vantage point of having been embedded in the Filecoin ecosystem for many years, gathering feedback from users, builders and the community, and having thought deeply about what is needed as the network moves forward.

The blog is organized in the following sections:

What matters for Filecoin in 2024

Why these matter and how to measure progress

It is our hope that with the right north star, teams will be able to better coordinate and identify convergences between project-level interests & ecosystem interests. The proposed framework and metrics should make it easier for capital and resource allocators in the ecosystem to evaluate the level of impact each team is creating, and distribute capital and resources accordingly. For startups, this can help frame where broader ecosystem efforts may dovetail into your roadmap and releases.

WHAT MATTERS IN 2024

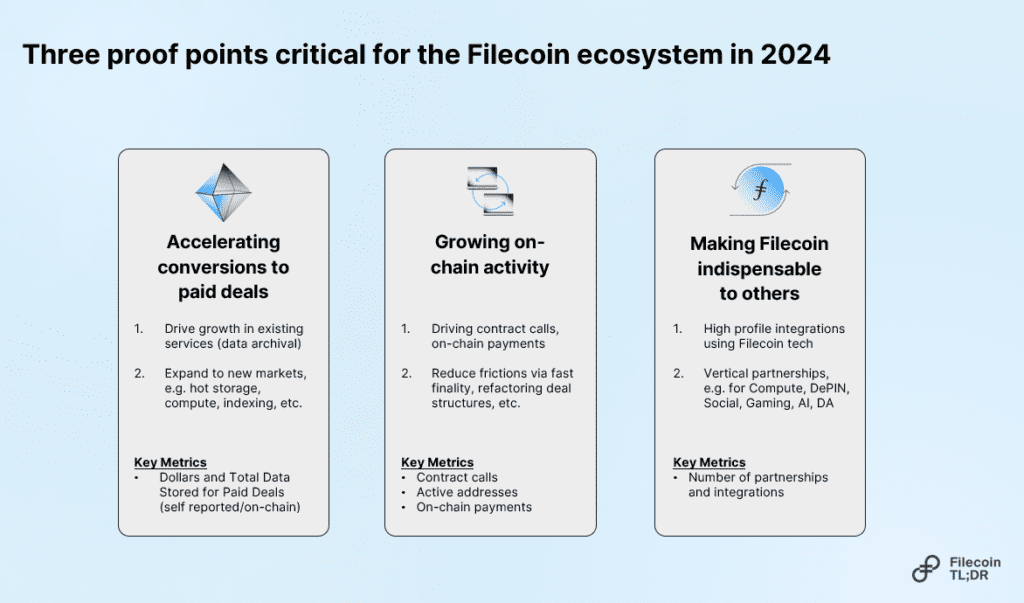

Accelerating conversions to paid deals: Helping Filecoin providers increase their paid services (storage, retrieval, compute) is critical for driving cashflows into Filecoin and to support sustainable funding of its hardware outside of token incentives.

Growing on-chain activity: Filecoin is not aiming to be just another L1 fighting over the same use cases. But it does have a unique value proposition as a base layer with “real world” services anchored into it. This enables new use cases (programmable services, DeFi around cash flows, etc.) that are unique to Filecoin. Building out and growing adoption of these services can help prove that Filecoin is not just “a storage layer”, but an economy with a stable set of cash flows.

Making Filecoin indispensable to others: Bull cycles mean velocity is critical – as is making Filecoin an indispensable part of the stack for more teams. There are many emerging themes to capitalize on (Chain Archival, Compute, AI) – and Filecoin positioning itself matters. The ecosystem collectively wins when more participants leverage Filecoin as a core part of their story. For individual teams, this means that shipping to your users matters. At the ecosystem level, it means orienting efforts to unblock the teams closest to driving integrations and building services on Filecoin.

The verticals in our framework remain relatively high-level – and many of these objectives will have their own set of tasks. But it is more critical first, for the ecosystem to be aligned that this is the right set of verticals to progress against. We dive into each vertical and some tangible metrics that the ecosystem should start tracking against.

WHY THESE MATTER AND HOW TO MEASURE PROGRESS

1) Accelerating conversion to paid deals

As a storage network – Filecoin should maximize the cashflows it can bring into its economy. Having incentives as an accelerant is fine – but without having a steady (and growing ramp) of paid deals Filecoin can’t achieve its maximum potential.

Paid deals (when settled on-chain) are a net capital inflow into the Filecoin economy that can be the substrate for use cases uniquely possible in our ecosystem. DeFi as an example has a real opportunity to provide actual services to businesses (e.g. converting currencies to pay for storage).

There are two main paths that we can drive growth of paid services:

Drive growth in existing services (data archival)

Expand to new markets with additional services (hot storage, compute, indexing, etc.)

In both cases, there’s work to be done to reduce friction for paid on-ramps or ship new features that raise the floor (as informed by on-ramps and projects trying to bring Filecoin services to market). It is critical that the Filecoin ecosystem collectively prioritizes the right efforts to make Filecoin services sellable, and allocate resources accordingly.

There are already a number of teams making substantial progress on this front (CID.Gravity, Seal Storage, Holon, Banyan, Lighthouse.storage, Web3Mine, Basin, among others) – and we can best measure progress by helping reduce their friction and helping drive their success.

We propose measuring success for this vertical in two forms:

Dollars and Total Data Stored for Paid Deals (self reported)

Dollars and Total Data Stored for Paid Deals (on-chain)

There are a number of initiatives from public goods teams along these efforts for the quarter (Q2 2024) which include:

FilOz: is working on a FIP for new proofs to reduce storage costs and dramatically improve retrieval speeds

DeStor: is helping drive enterprise adoption for business ready on-ramps

Ansa Research, Filecoin Foundation, etc.: Web3 BD support for ecosystem builders

Targeted grant funding for efforts that directly support growth of sustainable on-chain paid deal activity

2) Growing on-chain activity

Filecoin, as an L1, has more than just its storage service. Building a robust on-chain economy is critical for accelerating the services and tooling with which others can compose. In the Filecoin ecosystem, we have a unique opportunity in that there are real economic flows to enable via paid on-chain deals.

Centering our on-chain economy around supporting those flows – be it from automating renewals, designing incentives for retrievals, creating endowments for perpetual storage, or building economic efficiency for the operators of the network – can lead to compounding growth as it creates a flywheel.

As Filecoin owns more of its own economic activity on-chain, value will accrue for the token – enabling ecosystem users to use Filecoin in more productive ways, generating real demand for services inside the ecosystem.

We propose the following metrics for us to collectively measure success:

Contract calls

Active Filecoin addresses

Volume of on-chain payments

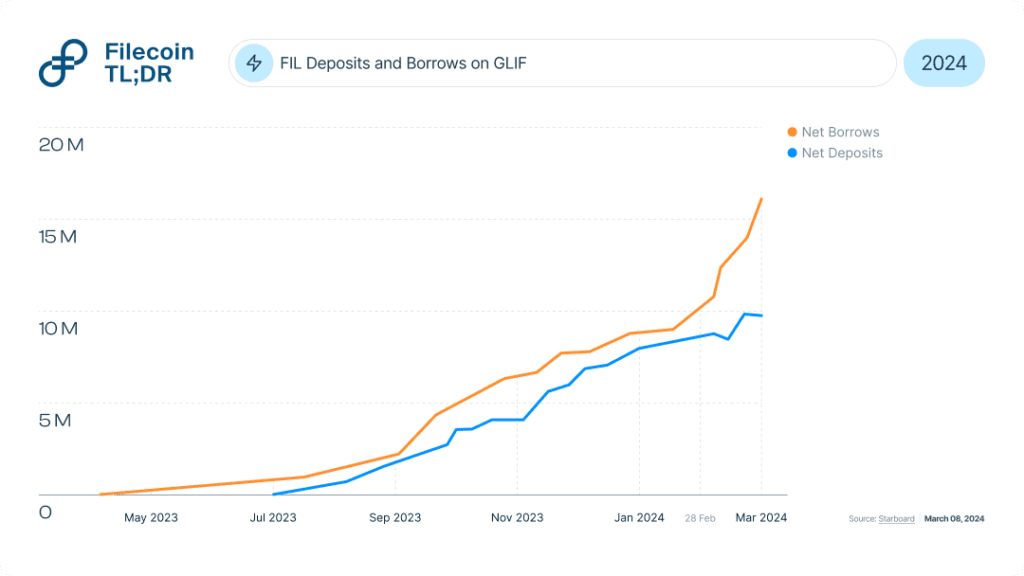

There are notable builders already seeding the on-chain infrastructure to leverage some of these primitives (teams like GLIF working on liquid staking, Lighthouse on storage endowments, and teams like Fluence enabling compute).

There’s a set of improvements that can dramatically reduce friction for driving on-chain activity, and there several efforts prioritized against this for Q2 2024:

FilOz: F3 to bring fast finality to Filecoin can both improve the bridging experience, and enable more “trade” between Filecoin and other economies (e.g. native payments from other ecosystems for services in Filecoin).

FilOz: Refactoring how deals work on Filecoin to enable more flexible payment (e.g. with stablecoins)

FilPonto, FilOz: Reducing EVM tech debt to substantially reduce friction for builders porting Solidity contracts onto Filecoin (and hardening the surrounding infrastructure for more stable services)

3) Making Filecoin indispensable to others

This vertical is broad, but we would argue that there are two key ways to be consider the impact that the Filecoin ecosystem is driving:

The first is along high profile integrations, where Filecoin is critical to the success of the customer and its proposition. It is especially critical for the ecosystem to provide the necessary support for these cross-chain integrations.

The second is along specific verticals, where there is a large and growing trend in activity; Filecoin is uniquely positioned to provide value here, both in terms of the primitives it has, as well as in its cost profile and scale

Opportunities are brimming in Web3 at the moment, and the ecosystem should rally workstreams around on-ramps that are making Filecoin integral to narratives such as Compute, DePIN (sensors), Social, Gaming, AI, and Chain Archival.

We propose that the metrics to evaluate for Filecoin indispensability as:

Number of partnerships and integrations

There are a number of efforts from ecosystem teams aimed at helping onramps succeed on this front in the quarter (Q2 2024):

Ansa Research, Filecoin Foundation, DeStor and others: Forming a new working group to accelerate shared ecosystem BD and marketing resources

Shared BD resources for builders in the Filecoin ecosystem

Shared Marketing resources and amplification (#ecosystem-amplification-requests in the Filecoin slack) to help signal boost ecosystem wins

Community Discord to help expand accessibility, visibility, and drive community engagement

FINAL THOUGHTS

After reading the above, we hope that the direction of Filecoin in the coming year is clearer. Filecoin is at a pivotal moment where many of its pieces are coming together. Protocols and ecosystems naturally evolve and each stage calls for different priorities and strategies for the next leg of growth. By focusing efforts in the ecosystem, we believe that the Filecoin ecosystem can make its resources and support go that much further.

We are excited for what is to come and how Filecoin can continue to expand the pie for what can be done on Web3 rails. Moving forward, Ansa Research will post periodic updates on the key metrics for Filecoin’s ecosystem progress.

To stay updated on the latest Filecoin happenings, follow the @Filecointldr handle.

Disclaimer: This information is for informational purposes only and is not intended to constitute investment, financial, legal, or other advice. This information is not an endorsement, offer, or recommendation to use any particular service, product, or application.

Editor’s Note: This blogpost is a repost of the original content published on 5 April 2024, by Turan VuralYuki Yuminaga from Fenbushi Capital. Established in 2015, Fenbushi Capital holds the distinction of being Asia’s pioneering blockchain-focused asset management firm with an AUM of $1.6 billion. Through research and investment, the firm aims to play a vital role in shaping the future of blockchain tech across diverse sectors.This blogpost is an example of these efforts, and represents the independent view of these authors, whom have given permission for this re-publication.

Data availability (DA) is a core technology in the scaling of Ethereum, allowing a node to efficiently verify that data is available to the network without having to host the data in question. This is essential for the efficient building of rollups and other forms of vertical scaling, allowing execution nodes to ensure that transaction data is available during the settlement period. This is also crucial for sharding and other forms of horizontal scaling, a planned future update to the Ethereum network, as nodes will need to prove that transaction data (or blobs) stored in network shards are indeed available to the network.

Several DA solutions have been discussed and released recently (e.g., Celestia, EigenDA, Avail), all with the intent of providing performant and secure infrastructure for applications to post DA.

The advantage of an external DA solution over an L1 such as Ethereum is that it provides an inexpensive and performant vehicle for on-chain data. DA solutions often consist of their own public chains built to enable cheap and permissionless storage. Even with modifications, the fact remains that hosting data natively from a blockchain is extremely inefficient.

Thus, we find that it is intuitive to explore a storage-optimized solution such as Filecoin for the basis of a DA layer. Filecoin uses its blockchain to coordinate storage deals between clients and storage providers but allows data to be stored off-chain.

In this post, we investigate the viability of a DA solution built on top of a Distributed Storage Network (DSN). We consider Filecoin specifically, as it is the most adopted DSN to date. We outline the opportunities that such a solution would offer, and the challenges that need to be overcome to build it.

A DA layer provides the following to services relying on it:

Client Safety: No node can be convinced that unavailable data is available.

Global Safety: The un/availability of data is agreed upon by all except at most a small minority of nodes.

Efficient data retrievability.

All of this needs to be done efficiently to enable scaling. A DA layer provides higher performance at a lower cost across the three points above. For example, any node can request a full copy of the data to prove custody, but this is inefficient. By having a system that provides all three of these, we achieve a DA layer that provides the security required for L2s to coordinate with an L1, along with stronger lower bounds in the presence of a malicious majority.

Custody of Data

Data posted to a DA solution has a useful lifetime: long enough to settle disputes or verify a state transition. Transaction data needs to be available only long enough to verify a correct state transition or to give validators enough opportunity to construct fraud proofs. As of writing, Ethereum calldata is the most common solution used by projects (rollups) requiring data availability.

Efficient Verification of Data

Data Availability Sampling (DAS) is the standard method of answering the question of DA. It comes with additional security benefits, strengthening network actors’ ability to verify state information from their peers. However, it relies on nodes to perform sampling: DAS requests must be answered to ensure mined transactions won’t be rejected, but there is no positive or negative incentive for a node to request samples. From the perspective of nodes that request samples, there is no negative penalty for not performing DAS. As an example, Celestia provides the first and only light client implementation to perform DAS, delivering stronger security assumptions to users and reducing the cost of data verification.

Efficient Access

A DA needs to provide efficient access to data to the projects using it. A slow DA may become the bottleneck for the services relying on it, causing inefficiencies at best and system failures at worst.

Decentralized Storage Network

A Decentralized Storage Network (DSN, as formalized in the Filecoin Whitepaper¹) is a permissionless network of storage providers that offer storage services for users of the network. Informally, it allows independent storage providers to coordinate storage deals with clients that need storage services and provides cheap and resilient data storage to clients seeking storage services at a low price. This is coordinated through a blockchain that records storage deals and enables the execution of smart contracts.

A DSN scheme is a tuple of three protocols: Put, Get, and Manage. This tuple comes with properties such as fault tolerance guarantees and participation incentives.

Put(data) → key Clients execute Put to store data under a unique key. This is achieved by specifying the duration for which data will be stored on the network, the number of replicas of the data that are to be stored for redundancy, and a negotiated price with storage providers.

Get(key) → data Clients execute Get to retrieve data that is being stored under a key.

Manage() The Manage protocol is called by network participants to coordinate the storage space and services made available by providers and repair faults. In the case of Filecoin, this is managed via a blockchain. This blockchain records data deals being made between clients and data providers and proofs of correctly stored data to ensure that data deals are being upheld. Correctly stored data is proved via the posting of proofs generated by data providers in response to challenges from the network. A storage fault occurs when a storage provider fails to generate a Proof-of-Replication or Proof-of-Spacetime promptly when requested by the Manage protocol, which results in the slashing of the storage provider’s stake. Deals can self-heal in the case of a storage fault if more than one provider is hosting a copy of the data on the network by finding a new storage provider to honor the storage deal.

DSN Opportunities

The work done thus far in DA projects has been to transform a blockchain into a platform for hot storage. Since a DSN is storage-optimized, rather than transforming a blockchain into a storage platform, we can simply transform a storage platform into one that provides data availability. The collateral of storage providers in the form of native FIL token can provide crypto-economic security that guarantees data is stored. Finally, the programmability of storage deals can provide flexibility around the terms of data availability.

The most compelling motivation to transform the capabilities of a DSN to solve DA is the cost reduction in the data storage under the DA solution. As we discuss below, the cost of storing data on Filecoin is significantly cheaper than storing data on Ethereum. Given current Ether/USD prices, it costs over 3 million USD to write 1 GB of calldata to Ethereum, only to be pruned after 21 days. This calldata expense can contribute to over half of the transaction cost of an Ethereum-based rollup. However, 1 GB of storage on Filecoin costs less than .0002 USD per month. Securing DA at this or any similar price would bring transaction costs down for users and contribute to the performance and scalability of Web3.

Economic Security

In Filecoin, collateral is required to make storage space available. This collateral is slashed when a provider fails to honor its deals or uphold network guarantees. A storage provider that fails to provide services faces losing both its posted collateral and any profit that would have been earned from providing storage.

Incentive Alignment

Many of Filecoin’s protocol incentives align with the goals of DA. Filecoin provides disincentives for malicious or lazy behavior: storage providers must actively provide proofs of storage during consensus in the form of Proof-of-Replicas and Proof-of-Spacetime, continuously proving that the storage exists without honest majority assumptions. Failure of a storage provider to provide proof results in stake slashing, and removal from consensus, among other penalties. Current DA solutions lack incentive for nodes to perform DAS, relying on ad-hoc altruistic behavior for proof of DA.

Programmability

The ability to customize data deals also makes a DSN an attractive platform for DA. Data deals can have varying durations, allowing users of a DSN-based DA to pay for only the DA that they need. Fault tolerance can also be tuned by setting the number of copies that are to be stored throughout the network. Further customization is supported via smart contracts on Filecoin (called Actors), which are executed on the FEVM. This leads to Filecoin’s growing ecosystem of DApps, from compute-over-storage solutions such as Bacalhau to DeFi and liquid staking solutions such as Glif. Retriev makes use of Filecoin Actors to provide incentive-aligned retrieval with permissioned referees. Filecoin’s programmability can be used to tailor DA requirements needed for different solutions, so that platforms that rely on DA are not paying for more DA than they need.

Challenges to a DSN-Based DA Architecture

In our investigation, we have identified significant challenges that need to be overcome before a DA service can be built on a DSN. As we now talk about the feasibility of implementation, we will use Filecoin as our main focus of the discussion.

Proof Latency

The cryptographic proofs that ensure the integrity of deals and stored data on Filecoin take time to prove. When data is committed to the network, it is partitioned into 32 gigabyte sectors and “sealed.” The sealing of data is the foundation of both the Proof-of-Replication (PoRep), which proves that a storage provider is storing one or more uniquecopies of the data, and Proof-of-Spacetime (PoST), which proves that a storage provider stored a unique copy continuously throughout the duration of the storage deal. Sealing has to be computationally expensive to ensure that storage providers aren’t sealing data on demand to undermine the required PoReP. When the protocol presents the periodic challenge to a storage provider to provide proof of unique and continuous storage, sealing has to safely take longer than the response window so that a storage provider can’t falsify proofs or replicas on the fly. For this reason, it can take providers approximately three hours to seal a sector of data.

Storage Threshold

Because of the computational expense of the sealing operation, the sector size of the data being sealed has to be economically worthwhile. The price of storage has to justify the cost of sealing to the storage provider, and likewise, the resulting cost of data being stored has to be low enough at scale (in this case, for an approximately 32GB chunk) for a client to want to store data on Filecoin. Although smaller sectors could be sealed, this would drive up the price of storage to compensate storage providers. To get around this, data aggregators collect smaller pieces of data from users to be committed to Filecoin as a chunk close to 32 GB. Data aggregators commit to user’s data via a Proof-of-Data-Segment-Inclusion (PoDSI), which guarantees the inclusion of a user’s data in a sector, and a sub-piece CID (pCID), which the user will be able to use to retrieve the data from the network.

Consensus Constraints

Filecoin’s consensus mechanism, Expected Consensus, has a block time of 30 seconds and finality within hours, which may improve in the near future (see FIP-0086 for fast finality on Filecoin). This is generally too slow to support the transaction throughput needed for a Layer 2 relying on DA for transaction data. Filecoin’s block time is lower-bounded by storage provider hardware; the lower the block time, the more difficult it is for storage providers to generate and provide proofs of storage, and the more storage providers will be falsely penalized for missing the proving window for the proper storage of data. To overcome this, InterPlanetary Consensus (IPC) subnets can be leveraged to take advantage of faster consensus times. IPC uses Tendermint-like consensus and DRAND for randomness: in the case that DRAND is the bottleneck, we would be able to achieve a 3-second block-time with an IPC subnet. In the case of a Tendermint bottleneck, PoCs such as Narwhal have achieved blocktimes in the hundreds of milliseconds.

Retrieval Speed

The final barrier-to-build is retrieval. From the constraints above, we can deduce that Filecoin is suitable for cold or lukewarm storage. However, the DA data is hot and needs to support performant applications. Incentive-aligned retrieval is difficult in Filecoin; data needs to be unsealed before it is served to clients, which adds latency. Currently, rapid retrieval is done via SLAs or the storage of un-sealed data alongside sealed sectors, neither of which can be relied on in the architecture of a secure and permissionless application on Filecoin. Especially with Retriev proving that retrieval can be guaranteed via the FVM, incentive-aligned rapid retrieval on Filecoin remains an area to be further explored.

Cost Analysis

In this section, we consider the cost that comes from these design considerations. We show the cost of storing 32GB as Ethereum calldata, Celestia blobdata, EigenDA blobdata, and as a sector on Filecoin using near-current market prices.

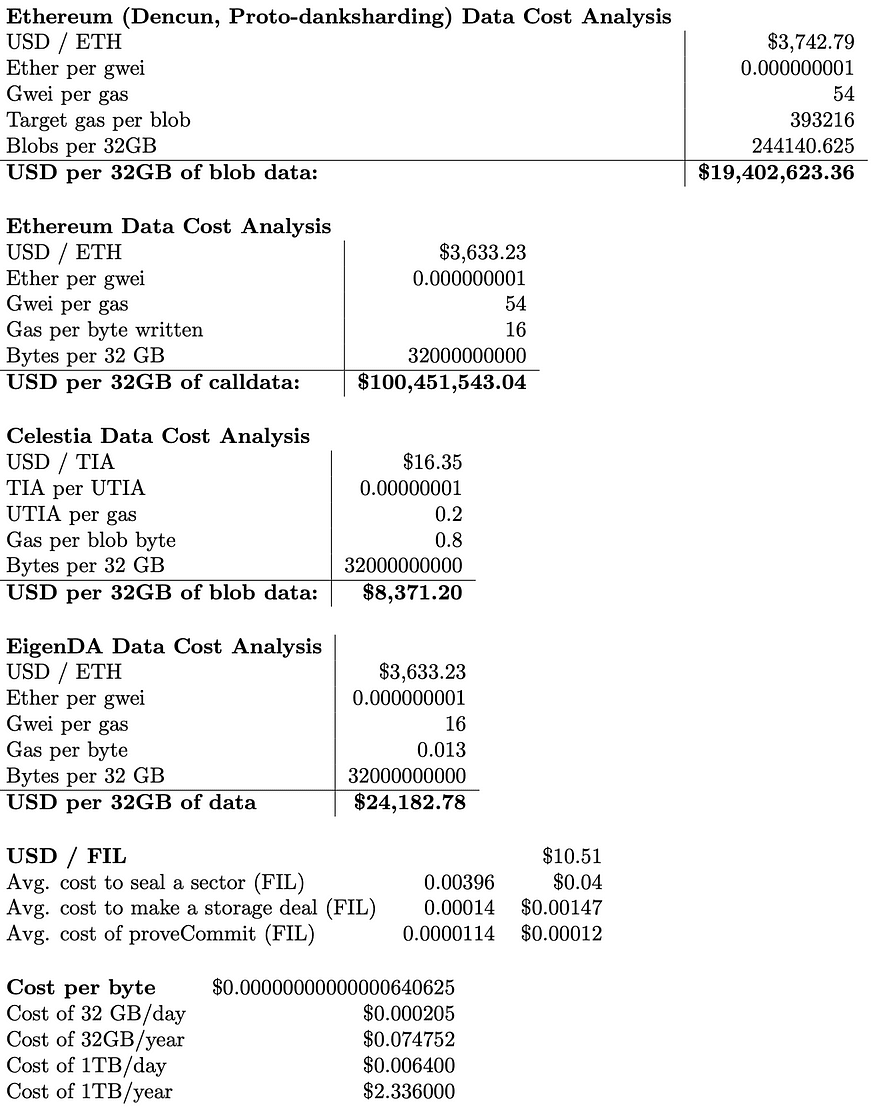

The analysis highlights the price of Ethereum calldata: 100 million USD for 32 GB of data. This price showcases the cost of security behind Ethereum’s consensus, and is subject to the volatility of Ether and gas prices. The Dencun upgrade, which introduced Proto-Danksharding (EIP-4844), introduced blob transactions with a target of 3 blobs per block of approximately 125 KB each, and variable gas blob pricing to maintain the target amount of blobs per block. This upgrade cut the cost of Ethereum DA by ⅕: 20 million USD for 32 GB of blob data.

Celestia and EigenDA provide significant improvements: 8,000 and 26,000 USD for 32 GB of data, respectively. Both are subject to the volatility of market prices and reflect to some extent the cost of consensus securing their data: Celestia with its native TIA token, and EigenDA with Ether.

In all of the above cases, the data stored is not permanent. Ethereum calldata is stored for 3 weeks, with blobs stored for 18 days. EigenDA stores blobs for a default of 14 days. As of the current Celestia implementation, blob data is stored indefinitely by archival nodes but only sampled by light nodes for a maximum of 30 days.

The final two tables are direct comparisons between Filecoin and current DA solutions. Cost equivalence first lists the cost of a single byte of data on the given platform. The amount of Filecoin bytes that can be stored for the same amount of time for the same cost is then shown.

This shows that Filecoin is orders of magnitude cheaper than current DA solutions, costing fractions of a cent to store the same amount of data for the same amount of time. Unlike Ethereum nodes and that of other DA solutions, Filecoin’s nodes are optimized to provide storage services, and its proof system allows nodes to prove storage, rather than replicate storage across every node in the network. Without accounting for the economics of storage providers (such as the energy cost to seal data), it shows that the basic overhead of the storage process on Filecoin is negligible. This shows a market opportunity in the millions of USD per gigabyte compared to Ethereum for a system that can provide secure and performant DA services on Filecoin.

Throughput

Below, we consider the capacity of DA solutions and the demand that is generated by major layer 2 rollups.

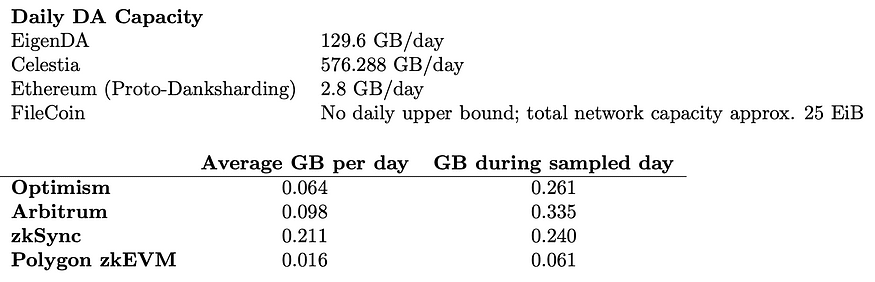

Because Filecoin’s blockchain is organized in tipsets with multiple blocks at every block-height, the number of deals that can be done is not restricted by consensus or block size. The strict data constraint of Filecoin is that of its network-wide storage capacity, not what is allowed via consensus.

For daily DA demand, we pull data from Rollups DA and Execution from Terry Chung and Wei Dai, which includes a daily average across 30 days and a singular sampled day. This allows us to consider average demand while not overlooking aberrations from the average (for example, Optimism’s demand on 8/15/2023 of approximately 261,000,000 bytes was over 4x its 30 day average of 64,000,000 bytes).

From this selection, we see that despite the opportunity of lower DA cost, we would need a dramatic increase in DA demand to make efficient use of the 32 GB sector size of Filecoin. Although sealing 32 GB sectors with less than 32 GB of data would be a waste of resources, we could do so while still reaping a cost advantage.

Architecture

In this section, we consider the technical architecture that can be achieved if we were to build this today. We will consider this architecture in the context of arbitrary L2 applications and an L1 chain that the L2 is serving. Since this solution is an external DA solution, like that of Celestia and EigenDA, we do not consider Filecoin as example L1.

Components

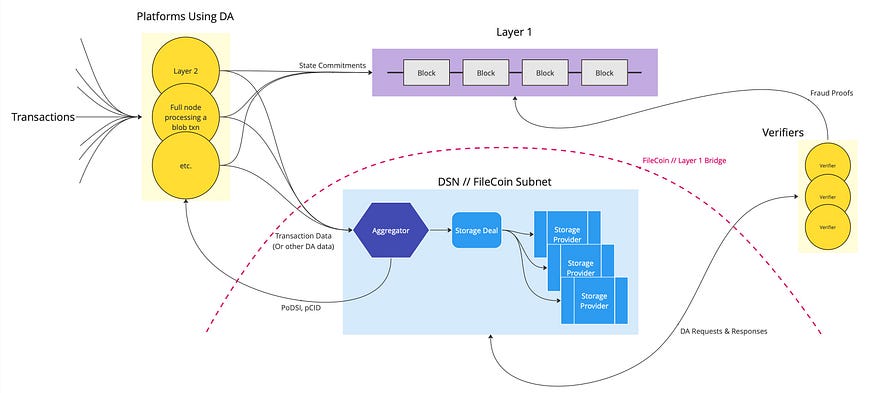

Even at a high-level, a DA on Filecoin will make use of many different features of the Filecoin ecosystem.

Transactions: Downstream users make transactions on a platform that requires DA. This could be an L2.

Platforms Using DA: These are the platforms that use DA as a service. This could be an L2 which posts transaction data to the Filecoin DA and commitments to an L1, such as Ethereum.

Layer 1: This is any L1 that contains commitments pointing to data on the DA solution. This could be Ethereum, supporting an L2 that leverages the Filecoin DA solution.

Aggregator: The frontend of Filecoin-based DA solution is an aggregator, a centralized component which receives transaction data from L2’s and other DA clients and aggregates them into 32 GB sectors suitable for sealing. Although a simple proof-of-concept would include a centralized aggregator, platforms using the DA solution could also run their own aggregator,for example as a sidecar to an L2 sequencer. The centralization of the aggregator can be seen as similar to that of an L2 sequencer or EigenDA’s disperser. Once the aggregator has compiled a payload near 32GB, it makes a storage deal with storage providers to store the data. Clients are given a guarantee that their data will be included in the sector in the form of a PoDSI (Proof of Data Segment Inclusion), and a pCID to identify their data once it is on the network. This pCID is what would be included in the state commitments on the L1 to reference supporting transaction data.

Verifiers: Verifiers request the data from the storage providers to ensure the integrity of state commitments and build fraud proofs, which are committed to the L1 in the case of provable fraud.

Storage Deal: Once the aggregator has compiled a payload near 32GB, the aggregator makes a storage deal with storage providers to store the data.

Posting blobs (Put): To initiate a put, a DA client will submit their blob containing transaction data to the aggregator. This can be done in an off-chain manner, or an on-chain manner via an on-chain aggregator oracle. To confirm receipt of the blob, the aggregator returns a PoDSI to the client to prove that their blob is included in the aggregated sector that will be committed to the subnet. A pCID (sub-piece Content IDentifier) is also returned. This is what the client and any other interested party will use to reference the blob once it is being served on Filecoin.

Data deals would appear on-chain within minutes of the deal being made. The largest barrier to latency is the sealing time, which can take 3 hours. This means that although the deal has been made, and the client can be confident that the data will appear in the network, the data cannot be guaranteed to be queryable until the sealing process is complete. The Lotus client has a fast-retrieval feature in which an unsealed copy of the data is stored alongside the sealed copy that may be able to be served as soon as the unsealed data is transferred to the data storage provider, as long as a retrieval deal does not depend on the proof of sealed data to appear on the network. However, this functionality is at the discretion of the data provider, and is not cryptographically guaranteed as part of the protocol. If a fast-retrieval guarantee is to be provided, there would need to be changes to consensus and dis/incentive mechanisms in place to enforce it.

Retrieving blobs (Get): Retrieval is similar to a put operation. A retrieval deal needs to be made, which will appear on-chain within minutes. Retrieval latency will depend on the terms of the deal and whether an unsealed copy of data is stored for fast retrieval. In the fast retrieval case, the latency will depend on network conditions. Without fast retrieval, data will need to be unsealed before being served to the client, which takes the same amount of time as sealing, on the order of 3 hours. Thus without optimizations we have a maximum round-trip of 6 hours, major improvement in data serving would need to be made before this becomes a viable system for DA or fraud proofs.

Proof of DA: proof of DA can be considered in two steps; via the PoDSI that is given when the data is committed to the aggregator while the deal is being made and then the continued commitment of PoRep and PoST that storage providers provide via Filecoin’s consensus mechanism. As discussed above, the PoRep and PoST give scheduled and provable guarantees of data custody and persistence.

This solution will make heavy use of bridging, as any client that relies on DA (regardless of the construction of proofs) will need to be able to interact with Filecoin. In the case of the pCID included in the state transition that is posted to the L1, a verifier can make an initial check to make sure that a bogus pCID wasn’t committed. There are several ways that this could be done, for example, via an oracle that posts Filecoin data on the L1 or via verifiers that verifies the existence of a data deal or sector that corresponds to the pCID. Likewise, the verification of validity or fraud proofs that get posted to the L1 may need to make use of a bridge to be convinced of a proof. Current available bridges are Axelar and Celer.

Security Analysis

Filecoin’s integrity is enforced through the slashing of collateral. Collateral can be slashed in two cases: storage faults or consensus faults. A storage fault corresponds to a storage provider not being able to provide proof of stored data (either PoRep or PoST), which would correlate to a lack of data availability in our model. A consensus fault corresponds to malicious action in consensus, the protocol that manages the transaction ledger from which the FEVM is abstracted.

A Sector Fault refers to the penalty incurred from the failure to post proof of continuous storage. Storage providers are allowed a one-day grace period during which a penalty is not incurred for faulty storage. After 42 days from a sector becoming faulty, the sector is terminated. Incurred fees are burnt.

A Sector Termination occurs after a sector has been faulty for 42 days or a storage provider purposefully terminates a deal. Termination fees are equivalent to the maximum amount that a sector has earned up to termination, with an upper bound of 90 days’ worth of earning. Unpaid deal fees are returned to the client. Incurred fees are burnt.

Storage Market Actor Slashing occurs in the event of a terminated deal. This is the slashing of the collateral that the storage provider puts up behind the deal.

The security provided by Filecoin is very different from that of other blockchains. Whereas blockchain data is typically secured via consensus, Filecoin’s consensus only secures the transaction ledger, not the data referred to by the transaction. The data that is stored on Filecoin has only enough security to incentive-align storage providers to provide storage. This means that the data stored on Filecoin is secured via fault penalties and business incentives such as reputation with clients. In other words, a data fault on a blockchain is equivalent to a breach of consensus, and breaks the safety of the chain or its notion of the validity of transactions. Filecoin is designed to be fault tolerant when it comes to data storage, and therefore only uses its consensus to secure its dealbook and deal-related activities. The cost of a storage miner not fulfilling its data deal has a maximum of 90 days worth of storage reward in penalties, and the loss of the collateral put up by the miner to secure the deal.

Therefore, the cost of a data withholding attack being launched from Filecoin providers simply the opportunity cost a retrieval deal. Data retrieval on Filecoin relies on the storage miner being incentivized by a fee paid for by the client. However, there is no negative impact to a miner for not responding to a data retrieval request. To mitigate the risk of a single storage miner ignoring or refusing data retrieval deals, data on Filecoin can be stored by multiple miners.

Since the economic security behind the data being stored on Filecoin is considerably less than that of blockchain based solutions, the prevention of data manipulation must also be considered. Data manipulation is protected via Filecoin’s proof system. Data is referred to via CIDs, through which data corruption is immediately detectable. A provider therefore cannot serve corrupt data, as it is easy to verify whether the fetched data matches the requested CID. Data providers cannot store corrupted data in the place of uncorrupted data. Upon the receipt of client data, providers must provide proof of a correctly sealed data sector to initiate the data deal (check this). Therefore, a storage deal cannot be started with corrupt data. During the lifetime of the storage deal, PoSTs are provided to prove custody (recall that this proves both custody of the sealed data sector and custody since the last PoST). Since the PoST is reliant on the sealed sector at the time of proof generation, a corrupt sector would result in a bogus PoST, resulting in a sector failure. Therefore, a storage provider can neither store nor serve corrupted data, cannot claim reward for services provided for uncorrupted data, and cannot avoid being penalized for tampering with a client’s data.

Security can be strengthened through increasing the collateral committed by the storage provider to the Storage Market Actor, which is currently decided by the storage provider and the client. If we assume that this was sufficiently high enough (for example, the same stake as an Ethereum validator) to incentivize a provider not to default, we can think of what is left to secure (even though this would be extremely capital-inefficient, as this stake would be needed to secure each transaction blob or sector with aggregated blobs). Now, a data provider could choose to make data unavailable for maximums of 41-day chunks before the storage deal is terminated by the Storage Market Actor. Assuming a shorter data deal, we could assume that the data can be made unavailable until the last day of the deal. In the absence of coordinated malicious actors, this can be mitigated via replication on multiple storage providers so that the data can continue being served.

We can consider the cost of an attacker overriding consensus to either accept a bogus proof or rewrite ledger history to remove a deal from the orderbook without penalizing the responsible storage provider. It is worth noting however that in the case of such a safety violation, an attacker would be able to manipulate Filecoin’s ledger however they want. In order for an attacker to commit such an attack, they would need at least a majority stake in the Filecoin chain. Stake is related to storage provided to the network; with a current 25 EiB (10¹⁶ bytes) of data securing the Filecoin chain, at least 12.5 EiB would be needed for a malicious actor to offer its own chain that would win the fork-choice rule. This is further mitigated by slashing related to consensus faults, for which the penalty is the loss of all pledged collateral and block rewards and all suspension from participation in consensus.

Aside: Withholding attacks on other DA solutions Although the above shows that Filecoin is lacking in protecting data from withholding attacks, it is not alone.

Ethereum: In general, the only way to guarantee that a request to the Ethereum network is answered is to run a full node. Full nodes have no requirements to fulfill data retrieval requests outside of consensus — and therefore. Constructs such as PeerDAS introduce a peer scoring system for a node’s responses to data retrieval in which a node with a low enough score (essentially a DA reputation) could be isolated from the network.

Celestia: Even though Celestia has much stronger security per-byte against withholding attacks in comparison to our Filecoin construction, the only way to take advantage of this security is to host your own full node. Requests to Celestia infrastructure that are not owned and operated in-house can be censored without penalty.

EigenDA: Similar to Celestia, any service can run an EigenDA Operator node to ensure retrieval of their own data. As such, any out protocol data retrieval request can be censored. Also note that EigenDA has a centralized and trusted dispenser in charge of data encoding, KZG commitment, and data dispersal, similar to our aggregator.

Retrieval Security

Retrievability is necessary for DA. Ideally, market forces motivate economically rational miners to accept retrieval deals, and compete with other miners to keep prices for clients low. It is assumed that this is enough for data providers to provide retrieval services, however given the importance of DA, it is reasonable to require more security.

Retrieval is currently not guaranteed via the economic security stipulated above. This is because it is cryptographically difficult to prove that data wasn’t received by a client (in the case where a client needs to refute a storage miner’s claim of sending data) in a trust-minimized manner. A protocol-native retrieval guarantee would be required in order for retrieval to be secured through the Filecoin’s economic security. With minimal changes to the protocol, this means that retrieval would need to be associated with a sector fault or deal termination. Retriev is a proof-of-concept which was able to provide data retrieval guarantees by using trusted “referees” to mediate data retrieval disputes.

Aside: Retrieval on other DA solutions As can be seen above, Filecoin lacks the protocol-native retrieval guarantees necessary to keep storage (or retrieval providers) from acting selfishly. In the case of Ethereum and Celestia, the only way to guarantee that data from the protocol can be read is to self-host a full node, or trust a SLA from an infrastructure provider. It is not trivial to guarantee retrieval as a Filecoin storage provider; the analogous setting in Filecoin would be to become a storage provider (requiring significant infrastructure cost) and successfully accept the same storage deal as a storage provider that was posted as a user, at which point one would be paying themselves to provide storage to themselves.

Latency Analysis

Latency on Filecoin is determined by several factors, such as network, topology, storage mining client configuration, and hardware capabilities. We provide a theoretical analysis which discusses these factors, and the performance that can be expected by our construct.

Due to the design of Filecoin’s proof system and lack of retrieval incentives, Filecoin is not optimized to provide high-performance round trip latency from the initial posting of data to the initial retrieval of data. High performance retrieval on Filecoin is an active area of research that is constantly changing as storage providers increase their capabilities and as Filecoin introduces new features. We define a “round trip” as the time from the submission of a data deal to the the earliest moment the data submitted to Filecoin can be downloaded.

Block Time In Filecoin’s Expected Consensus, data deals can be included within the block-time of 30 seconds. 1 hour is the typical time for confirmation of sensitive on-chain data (such as coin transfers).

Data Processing Data processing time varies widely between storage providers and configurations. The sealing process is designed to take 3 hours with standard storage mining hardware. Miners often outperform this 3 hour threshold via special client configurations, parallelization, and investing in more capable hardware. This variation also affects the duration of sector un-sealing, which can be circumvented altogether by quick retrieval options in Filecoin client implementations such as Lotus. The quick retrieval setting stores an unsealed copy of data alongside sealed data, significantly speeding up retrieval time. Based on this, we can assume a worst-case delay of three hours from the acceptance of a data deal to when the data is available on-chain.

Conclusion and Future Directions

This article explores building a DA by leveraging an existing DSN, Filecoin. We consider the requirements of a DA with respect to its role as a critical element of scaling infrastructure in Ethereum. We consider building on top of Filecoin for the viability of DA on a DSN, and use it to consider the opportunities that a solution on Filecoin would provide to the Ethereum ecosystem, or any that would benefit from a cost-effective DA layer.

Filecoin proves that a DSN can dramatically improve the efficiency of data storage in a distributed, blockchain-based system, with a proven saving of 100 million USD per 32 GB written at current market prices. Even though the demand for DA is not yet high enough to fill 32 GB sectors, the cost advantage of a DA still holds if empty sectors are sealed. Although current latency of storage and retrieval on Filecoin is not appropriate for the hot storage needs, storage miner-specific implementations can provide reasonable performance with data being available in under 3 hours.

The increased trust in Filecoin storage providers can be tuned via variable collateral, such as in EigenDA. Filecoin extends this tunabel security to allow for a number of replicas to be stored across the network, adding tunable byzantine tolerance. Guaranteed and performant data retrieval would need to be solved in order to robustly deter data withholding attacks, however like any other solution, the only way to truly guarantee retrievability is to self-host a node or trust infrastructure providers.

We see opportunities for DA in the further development of PoDSI, which could be used (alongside Filecoin’s current proofs) in place of DAS to guarantee data inclusion in a larger sealed sector. Depending on how this looks, this may make slow turnaround of data tolerable, as fraud proofs could be posted in a window of 1 day to 1 week, while DA could be guaranteed on demand. PoDSIs are still new and under heavy development, and so we make no implication yet on what an efficient PoDSI could look like, or the machinery needed to build a system around it. As there are solutions for compute on top of Filecoin data, the idea of a solution that computes a PoDSI on sealed or unsealed data may not be out of the realm of near-future possibilities.

As both the field of DA and Filecoin grows, new combinations of solutions and enabling technologies may enable new proof of concepts. As Solana’s integration with the Filecoin network shows, DSNs hold potential as a scaling technology. The cost of data storage on Filecoin provides an open opportunity with a large window of optimization. Although the challenges discussed in this article are presented in the context of enabling DA, their eventual solution will open a plethora of new tools and systems to be built beyond DA.

¹ Although this isn’t the construction of Filecoin, it is useful for those who are unfamiliar with programmable decentralized storage.

For more research pieces from Fenbushi Capital, check out their Medium page here.

To stay updated on the latest Filecoin happenings, follow the @Filecointldr handle.

Disclaimer: This information is for informational purposes only and is not intended to constitute investment, financial, legal, or other advice. This information is not an endorsement, offer, or recommendation to use any particular service, product, or application.

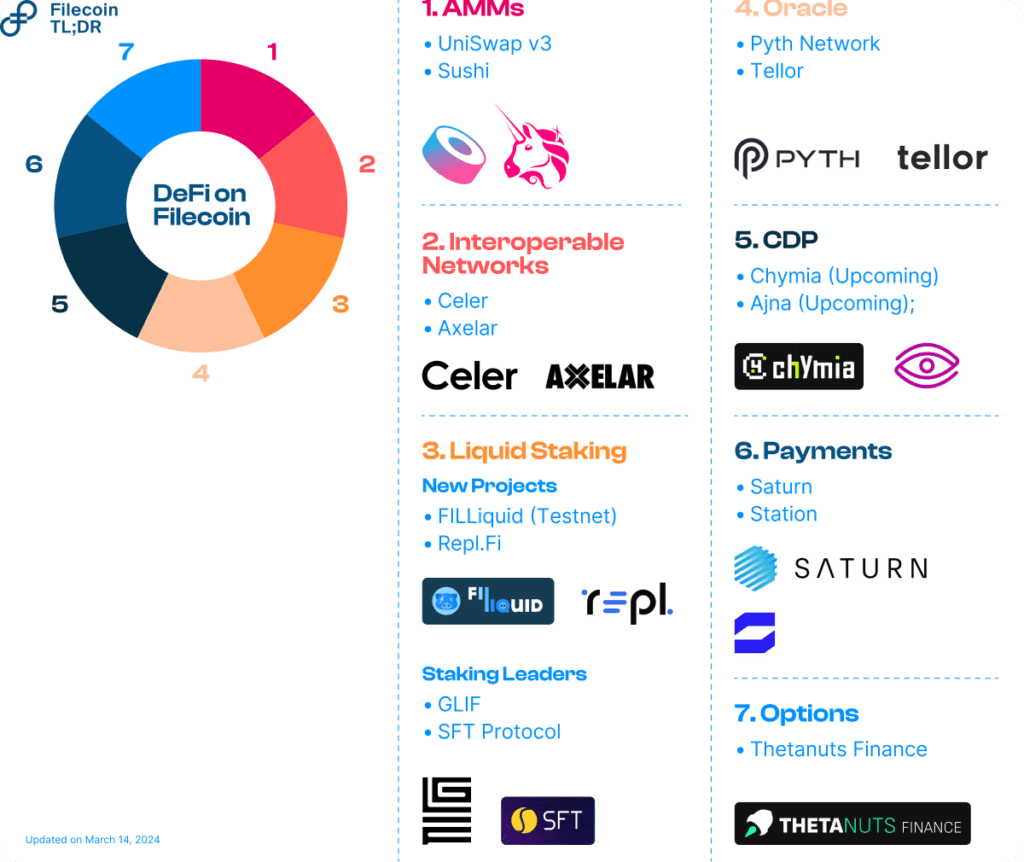

The Filecoin community celebrated the first anniversary of the Filecoin Virtual Machine (FVM) launch on March 14, 2024. The FVM has brought programmability to Filecoin’s verifiable storage and opened up a unique DeFi ecosystem anchored around improving on-chain collateral markets. Liquid Staking, for example, as a subset of Filecoin DeFi, has hit over $500 million in TVL. As the network grows, several critical infrastructures across AMMs, Bridges, Oracles, and Collateral Debt Positions (CDPs) are coming together to propel DeFi expansion in 2024.

In this blog post, let’s take a look at the latest DeFi projects launched on top of FVM and provide a view into future areas of activity.

DeFi Developments on FVM

Automated Market Makers

Automated Market Makers (AMMs) connect Filecoin with other Web3 ecosystems, enabling on-chain swaps, deeper liquidity, and fresh LP opportunities.

Decentralized Exchanges: ✅

Recently, leading Decentralized Exchanges Uniswap v3 (via Oku.trade) and Sushi integrated with Filecoin by deploying on the FVM. Oku Trade’s interface enables Uniswap users to easily exchange assets and provide liquidity on Filecoin. With this, FVM developers can effortlessly access bridged USDC and ETH assets natively on the Filecoin network, broadening Filecoin’s reach. As a foundational DeFi primitive, DEXes also opens the floodgates for non-native applications to leverage Filecoin’s robust storage and compute hardware.

Interoperability Networks

Bridges: ✅

Bridges help bring liquidity into DEXs and AMMs on FVM. For developers building on FVM, Bridges connects Filecoin’s verifiable data with tokens, users, and applications on any chain, ensuring maximum composability for DeFi protocols. For this purpose, messaging, and token bridging solutions by Axelar and Celer were added to the Filecoin network immediately post-FVM launch.

Today, AMMs Uniswap v3 and Sushi along with several other DeFi applications are natively bridged to Filecoin with the help of cross-chain infrastructure enabled by Axelar and Celer.

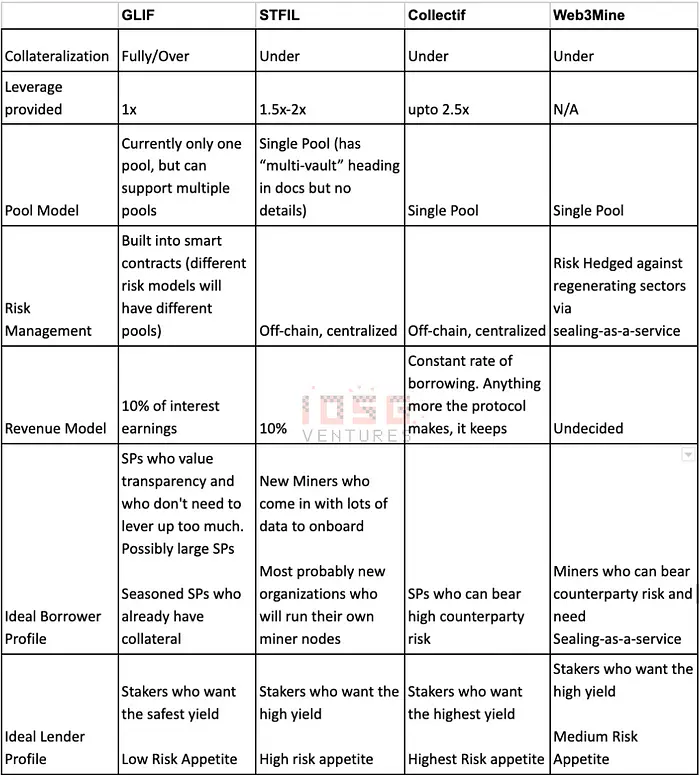

Liquid Staking