2024 has been a pivotal year for Filecoin, with significant progress in the Filecoin Virtual Machine (FVM), Storage, Retrievals and Compute. In this blogpost, we’ll recap the key milestones of 2024 and take a look at the major growth drivers shaping Filecoin’s path into 2025.

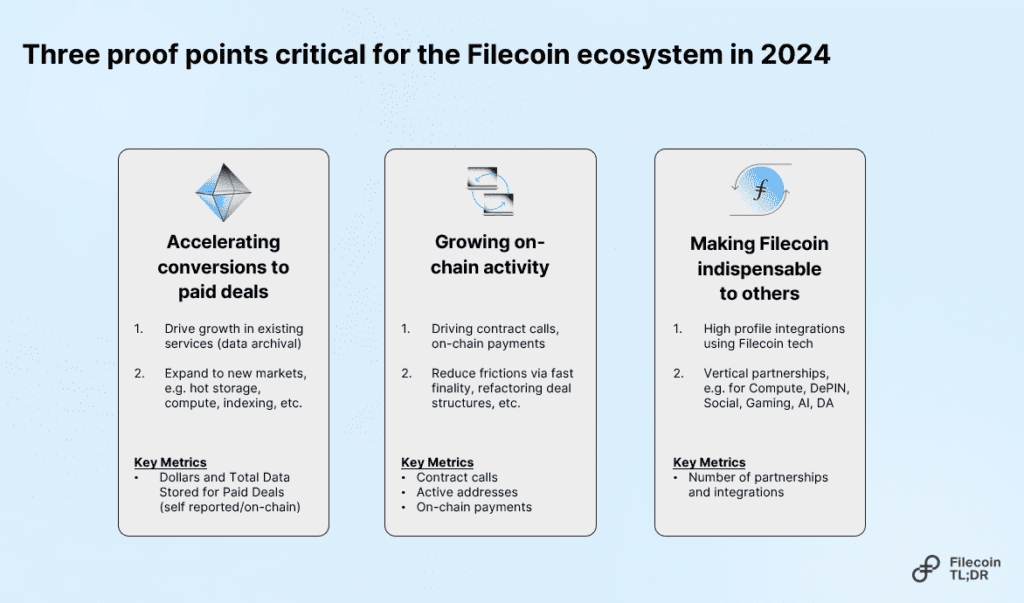

Accelerating Paid Deals: Boosting paid services (storage, retrieval, compute) on Filecoin to generate cashflow for service providers. This helps to support more sustainable hardware funding beyond token incentives.

Growing On-Chain Activity: Increasing activity through programmable services, DeFi, and new use cases.

Becoming Indispensable: Establishing Filecoin as an integral component of other projects and businesses.

These priorities are not mutually exclusive – they layer onto each other and are all signs that the Filecoin ecosystem is growing increasingly valuable.

So how did we fare across these priorities in 2024?

1. Accelerating Paid Deals

Paid Deals is an ecosystem-level metric that reflects the volume of paid services within the Filecoin network. FilecoinTLDR is currently tracking this metric here.

In 2024, Filecoin made significant strides in accelerating paid deals by reducing friction for businesses entering the ecosystem, with key advancements like the development of Proof of Data Possession (PDP) and the emergence of Layer 2 solutions.

Enabling Efficient Hot Storage with PDP

Projected for Q1 2025, Proof of Data Possession (PDP) introduces a new proof primitive to the Filecoin network, marking the first major proof development since Proof of Replication (PoRep) and Proof of Spacetime (PoSt). Unlike PoRep, which excels at cold storage through sealed sectors, PDP is designed for “hot data”, which is data that needs fast and frequent retrieval.

This new proof type enables cost-effective “cache” storage on Filecoin without sealing and unsealing, enabling rapid data onboarding and retrieval. PDP opens the door for a new class of storage providers focused on hot storage and fast retrievals, benefiting onramps like Basin, Akave, and Storacha.

Scaling Filecoin with L2s

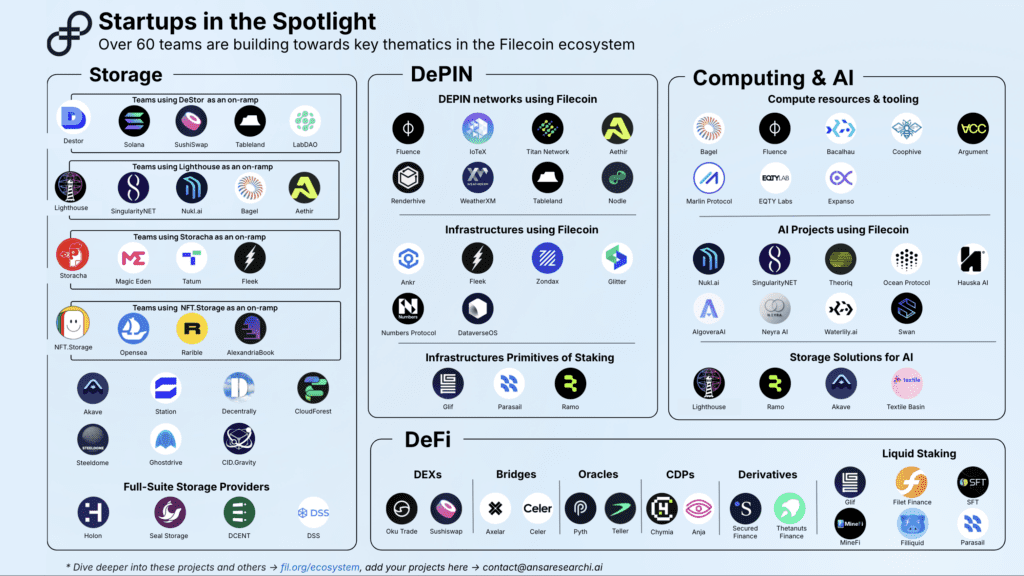

In 2024, we saw a rise in Layer 2 solutions built on top of Filecoin (We also covered this in our earlier blogpost “State of L2s on Filecoin”). L2s like Basin, Akave and Storacha enable both horizontal and vertical scaling with secure, customizable subnets. These L2s enhance Filecoin by unlocking new use cases: including managing data-intensive workloads, supporting AI and unstructured data, powering gaming and privacy-focused applications — all of which create more opportunities for paid deals.

2. Growing On-Chain Activity

Filecoin has made notable progress in accelerating on-chain activity through the FVM, which spurred growth in its DeFi economy. The proposed Filecoin Web Services (FWS) and launch of FIL-collateralized stablecoins are set to further boost this momentum.

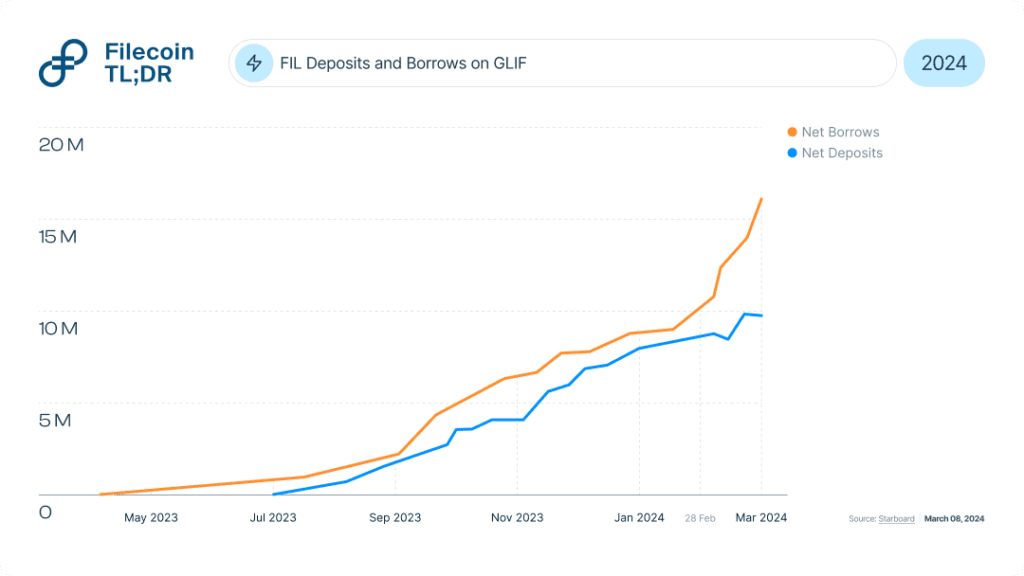

As of December 16 2024, more than 4,700 unique contracts have been deployed on FVM, enabling over 3 million transactions. DeFi activity on FVM saw average net deposits exceeding 30M FIL ($200M), driven by staking, liquid staking, and DEXs, with GLIF leading at 62%, followed by FilFi (10%) and SFT Protocol (9%). Net borrows averaged 26M FIL ($173M), highlighting strong growth in Filecoin’s DeFi ecosystem.

FIL-Collateralized Stablecoin for the Filecoin Ecosystem

USDFC is a FIL-backed stablecoin launched by Secured Finance in Q4 2024 to address key challenges in the Filecoin ecosystem. It introduces stability to a network previously lacking stablecoin options, reducing volatility and enhancing value storage, much like DAI did for Ethereum.

By allowing FIL holders and SPs to collateralize their assets for USD, USDFC helps cover operational costs without selling FIL, preserving asset value and network support. It also boosts liquidity in lending markets by providing FIL-backed stablecoin liquidity, driving more efficient capital flows within the Filecoin ecosystem.

3. Becoming Indispensable

DePIN gained prominence, with Filecoin strengthening its position through key partnerships with AI and compute projects. Meanwhile, on-chain archival received significant recognition through major on-ramp partnerships.

“…thanks to Filecoin for building an awesome decentralized archive layer. “ –Anatoly (Solana Co-Founder)

Notable On-Ramps of 2024

At Solana Breakpoint this year, Filecoin founder Juan Benet highlighted how Filecoin’s zero-knowledge (ZK) storage is securing the entire Solana ledger.

Similarly, Cardano apps now have the opportunity to boost data redundancy and decentralization through the Blockfrost integration with Filecoin.

SingularityNET’s integration with Filecoin (via Lighthouse) emphasizes the growing need for scalable and cost-effective storage in the AI-driven era, where managing vast amounts of data efficiently is critical.

These meaningful partnerships help signal Filecoin as a key player in both the Chain Archival and AI narratives.

This year, Filecoin has positioned itself as a key player in the growing field of Decentralized AI. The onset of projects within the ecosystem like Ramo (network participation), Bagel (AI & cryptography research), Swan Chain (AI training and development), and Lilypad (distributed compute for AI) highlight Filecoin’s expanding role in powering AI innovation.

2024 Filecoin Challenges

Despite the immense progress, we noted some challenges that the community faced. Though bearing in mind that Web3 products are still very early, and the problem statement of forming a credible alternative to the centralized cloud is a huge one.

Product Market Fit:

Roadblocks like limited retrievability and high costs (driven by data replication), challenge the efficiency of the Filecoin network.

There is a need to make payments easier by allowing transactions directly on the Filecoin network, using methods like stablecoins or flexible payment options.

Improving visibility into the onboarding process and using customer data can help refine strategies and boost performance in key areas.

Building a Sustainable Economic Model + Stronger Economic Loops:

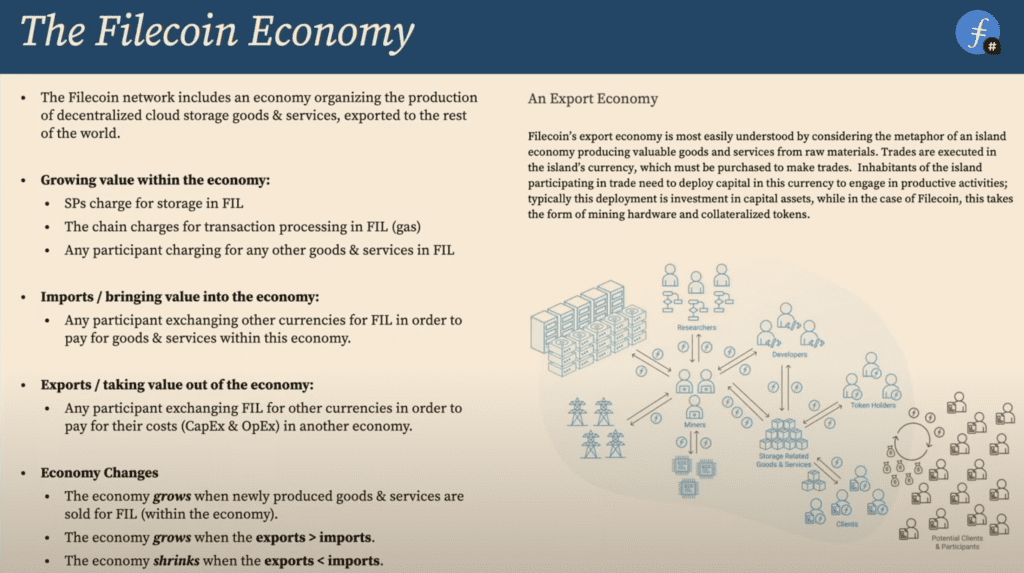

Viewing Filecoin as an island economy highlights its focus on accruing value by exporting goods and services while also keeping as much value as possible within the network by minimizing outflows.

A key challenge lies in reducing external outflows while finding ways to boost exports and capture more demand within the ecosystem.

Ensuring that transactions remain on-chain is equally crucial to strengthening this economic model and creating stronger economic loops.

Filecoin’s 2025 Outlook

Looking ahead to 2025, Filecoin’s evolution continues. Here are three key themes that could drive transformative growth for the network while addressing the 2024 challenges outlined above.

1. Accelerating Filecoin by 450x with Fast Finality (F3)

Fast Finality (F3), is one of the most impactful upgrades to Filecoin’s consensus layer since the launch of its mainnet. By drastically reducing transaction finality times, F3 overcomes a key limitation of the network’s original consensus mechanism. This enhancement is scheduled to go live on the mainnet in Q1 2025.

Old vs. New Finality:

Before F3, Filecoin’s consensus mechanism ensured secure block validation but required 7.5 hours (900 epochs) to finalize transactions, which was too slow for applications like smart contracts or cross-chain bridges.

With F3, transactions can now optimistically finalize in minutes—a 450X improvement.

What this means for Filecoin:

Enhanced Speed & UX: Transactions finalize within minutes, enabling low-latency applications and eliminating the long waits previously experienced.

Expanded Use Cases & Accessibility: L2 subnets like Interplanetary Consensus (IPC), Efficient smart contracts and decentralized applications, Blockchain bridges for interoperability with other chains.

Ultimately, this allows Filecoin to improve its usability across a wider variety of applications.

2. Moving Beyond Storage with FWS

Filecoin Web Services (FWS), emerged this year as a pivotal concept. It represents a strategic shift for Filecoin, expanding its scope from primarily a decentralized storage network to a broader marketplace for blockchain-based cloud services. This diversification can attract a wider range of users and use cases, potentially creating more positive economic loops within the network. Here are some pointers on why FWS should be on your radar:

Strengthening Filecoin’s Competitive Edge: FWS will introduce features like Programmatic SLAs (which automate and enforce service agreements through smart contracts, ensuring clear performance expectations and penalties) and Verifiable Proofs(which provide cryptographic evidence of service delivery, allowing clients to independently verify service execution).

Expands Filecoin’s Capabilities: Goes beyond Proof of Replication (PoRep) by adding Proof of Data Possession (PDP), enabling robust hot storage use cases. PDP will help improve data retrievability, a crucial factor in achieving product-market fit that has been widely discussed within the Filecoin community this year.

Positions Filecoin as a leading platform in the decentralized web: FWS will facilitate the integration of multiple networks and protocols, creating a cohesive marketplace for storage, compute, bandwidth, and other services. This could make Filecoin a key player in the growth of the decentralized web.

FWS is currently a concept in development, with a new storage service featuring PDP (v0) underway. Following this milestone, the development of the FWS marketplace will begin with its expected launch in Q1 2025.

3. Unlocking new value streams in Filecoin

As a Layer 1 blockchain, Filecoin primarily generates revenue through gas fee burns (which happen when chain resources are used or when faults arise). However, relying on gas fee burns as a main source of revenue is not scalable and more importantly increases operational expense costs as well as service costs.

A sustainable approach involves value returning to the Filecoin economy through the use of services in the FWS marketplace, fostering a more scalable and balanced revenue model. A proposed value accrual mechanisms includes:

FWS Fees: Commission (%) charged based on the transaction volume in the marketplace.

Service Fees: Applied when a user accesses a service or a vendor provides one

SLA Penalties: Imposed on service providers who fail to meet agreed-upon performance standards

This shift promises a more robust and diversified revenue stream, ensuring Filecoin’s continued relevance and profitability in the evolving market.

Final Thoughts

As data grows in value, we expect advancements in privacy-preserving machine learning, data-driven business models, and the increasing role of AI agents in unlocking decentralized storage’s potential.

Looking towards 2025, with the upcoming Fast Finality (F3) launch on the mainnet and the continued development of Filecoin Web Services, Filecoin is set to play a central role in shaping the future of data and AI within decentralized ecosystems. We expect to see these advancements positioning Filecoin beyond storage and unlocking a sustainable economic model through new revenue streams generated by FWS.

To stay updated on the latest in the Filecoin ecosystem, follow the @Filecointldr handle or join us on Discord.

Many thanks to HQ Han and Jonathan Victor for reviewing and providing valuable insights to this piece.

Disclaimer: This information is for informational purposes only and is not intended to constitute investment, financial, legal, or other advice. This information is not an endorsement, offer, or recommendation to use any particular service, product, or application.

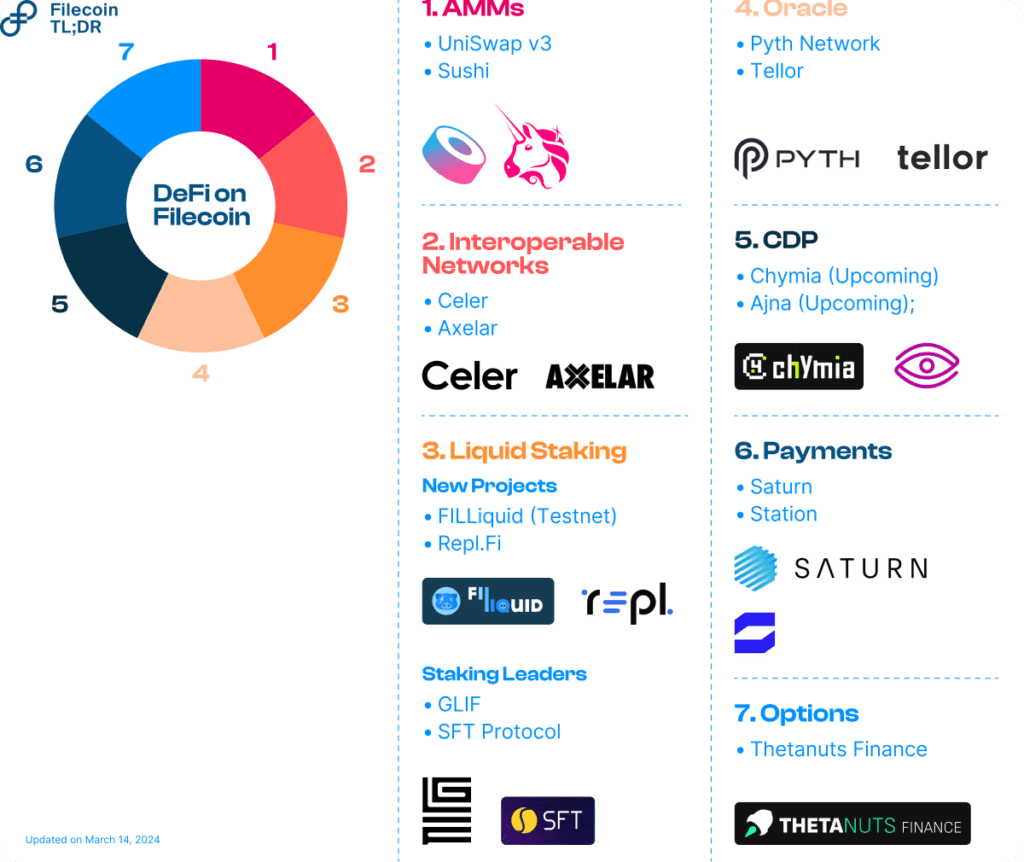

The Filecoin community celebrated the first anniversary of the Filecoin Virtual Machine (FVM) launch on March 14, 2024. The FVM has brought programmability to Filecoin’s verifiable storage and opened up a unique DeFi ecosystem anchored around improving on-chain collateral markets. Liquid Staking, for example, as a subset of Filecoin DeFi, has hit over $500 million in TVL. As the network grows, several critical infrastructures across AMMs, Bridges, Oracles, and Collateral Debt Positions (CDPs) are coming together to propel DeFi expansion in 2024.

In this blog post, let’s take a look at the latest DeFi projects launched on top of FVM and provide a view into future areas of activity.

DeFi Developments on FVM

Automated Market Makers

Automated Market Makers (AMMs) connect Filecoin with other Web3 ecosystems, enabling on-chain swaps, deeper liquidity, and fresh LP opportunities.

Decentralized Exchanges: ✅

Recently, leading Decentralized Exchanges Uniswap v3 (via Oku.trade) and Sushi integrated with Filecoin by deploying on the FVM. Oku Trade’s interface enables Uniswap users to easily exchange assets and provide liquidity on Filecoin. With this, FVM developers can effortlessly access bridged USDC and ETH assets natively on the Filecoin network, broadening Filecoin’s reach. As a foundational DeFi primitive, DEXes also opens the floodgates for non-native applications to leverage Filecoin’s robust storage and compute hardware.

Interoperability Networks

Bridges: ✅

Bridges help bring liquidity into DEXs and AMMs on FVM. For developers building on FVM, Bridges connects Filecoin’s verifiable data with tokens, users, and applications on any chain, ensuring maximum composability for DeFi protocols. For this purpose, messaging, and token bridging solutions by Axelar and Celer were added to the Filecoin network immediately post-FVM launch.

Today, AMMs Uniswap v3 and Sushi along with several other DeFi applications are natively bridged to Filecoin with the help of cross-chain infrastructure enabled by Axelar and Celer.

Liquid Staking

Liquid Staking protocols have been the prime mover within Filecoin DeFi. They’ve played a vital role in growing and improving on-chain collateral markets. Today, nearly 17% of the total locked collateral (approx. 30 million FIL) by storage providers comes from FVM-based protocols such as GLIF (52%), SFT Protocol (10%), Repl (9%) and the rest (29%). These protocols have increased capital access to storage providers while simultaneously enabling better yield access to token holders. Read more to learn how Filecoin staking works.

GLIF Points: 🔜

GLIF, the leading protocol on Filecoin, has a TVL of over $250 million. To put this into context, this surpasses the largest Liquid Staking protocols on L1 chains like Avalanche. As of writing this (March 06, 2024), 32% of all FIL stakes into GLIF liquidity pools were deposited shortly after its announcement to launch GLIF points (on Feb. 28, 2024), a likely precursor to a governance token.

Typically, to participate in the rewards program, GLIF users will have to deposit FIL and mint GLIF’s native token, iFIL. Similarly, the SFT protocollaunched a points program in 2023 based on its governance token to incentivize community participation.

Overall, we look forward to how the gameplay of points, popular among DApps in Web3 ecosystems, will act as a catalyst to decentralize governance and incentivize participation for Filecoin’s DeFi DApps.

New Staking Models: 👀

The influx of protocols experimenting with new models to inject liquidity into the ecosystem hasn’t slowed down. Two projects worth mentioning are Repl and FILLiquid.

Repl.fiintroduces the concept of “repledging.” Under repledging, SP’s pledged FIL are tokenized into pFIL, Repl’s native token, and used for other purposes including earning rewards. Repleding essentially increases the utility of locked assets thereby reducing opportunity costs for SPs. In just a few months after launch, Repl’s TVL has soared past $30 million.

FILLiquid, currently on testnet, models the business of FIL lending for SPs on algorithm-based fixed fees instead of traditional interest rates. The separation of payouts from the duration of deposits is expected to nudge long-term pledging and borrowing activities from token holders and SPs respectively, saving costs and increasing efficiency.

Price Oracles

Oracles, services that feed external data to smart contracts, are critical blockchain infrastructure essential for DeFi applications to grow and interact with the real world.

Pyth Network: ✅

Pyth recently launched its Price Feeds on the FVM. The integration allows FVM developers to access more than 400 real-time market data feeds while exploring opportunities to build on top of Filecoin’s storage layer. DeFi apps benefit from Pyth’s low-latency, high-fidelity financial data coming directly from global institutional participants such as exchanges, market makers, and trading firms.

Filecoin is also supported by Tellor, an optimistic oracle that gives FVM-based applications access to price feed data.

Collateralized Debt Positions

As DeFi activity on Filecoin is climbing, Collateralized Debt Positions (CDPs) will add more dimensions for other decentralized applications to build on FVM.

Chymia.Finance: 🔜

Chymia is an upcoming DeFi protocol on FVM. With a growing number of Liquid Staking Tokens (LST) on Filecoin, CDPs will extend the utility of locked tokens by generating stablecoins. Through Chymia, holders of LST can generate higher yields while using it as collateral for deeper liquidity.

Ajna: 🔜

Ajna is a noncustodial, peer-to-pool, permissionless lending, borrowing, and trading system requiring no governance or external price feed to function. As a result, any ERC20 on the FVM will be able to set up its own borrow or lend pools, making it easier for new developers to build a utility for their protocols.

Payments

Adjacent to storage offering on Filecoin, the FVM allows developers to bind DeFi payments to real-world primitives on the network. Built intuitively, Filecoin’s core economic flows enable paid services to settle on-chain. Station and Saturn are two notable Filecoin services to have successfully leveraged FVM for payments.

Filecoin Station: ✅

Station is a downloadable desktop application that uses idle computing resources on Station’s DePIN network to run small jobs. Participants in the network are rewarded with FIL earnings. Currently, Station operates the Spark and the Voyager modules, both aimed at improving retrievability on the network. In February, roughly 1,900 Station operators were rewarded with FIL for their participation.

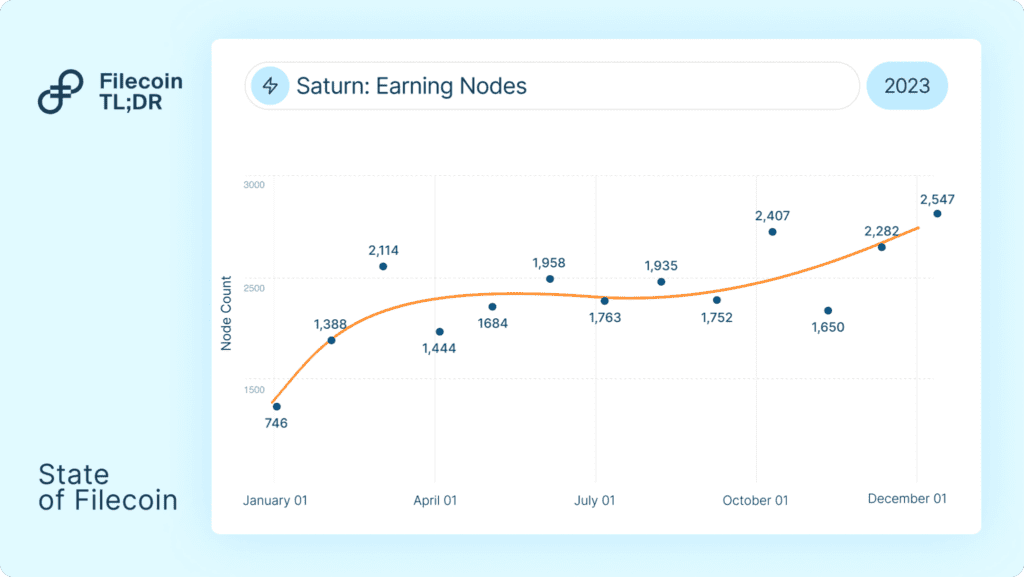

Filecoin Saturn: ✅

Saturn, a decentralized CDN network built on Filecoin, also leverages FVM for disbursing FIL payments to retrieval nodes on the network. In 2023, Saturn averaged over 2,000 earning nodes (retrieval providers on the network receiving FIL) for their services.

Decentralized Options

With growing liquidity, options are yet another emerging product in DeFi. Options facilitate the buying or selling of assets at a predetermined price on a future date, giving token holders protection against price volatility and an opportunity to speculate on market moves.

Thetanuts:✅

Currently, Thetanuts Finance, a decentralized on-chain options protocol supports Filecoin. The platform allows FIL holders to earn yield on their holdings via the covered call strategy. Thetanuts FIL-covered call vaults are cash-settled and work on a bi-weekly tenor.

Wallets

To use dApps on the FVM, users would be required to hold FIL in a f410 or 0x type wallet address. Over time, many Web3 wallets such as MetaMask, FoxWallet, and Brave have started supporting 0x/f410 addresses. MetaMask also supports Ledger. With this, it is possible to hold funds in a Ledger wallet and interact with FVM directly.

In addition, exchanges like Binance natively supporting the FEVM drastically reduce complexities for FVM builders. To learn more about the most recent wallet upgrades, visit the Filecoin TLDR webpage.

What’s Next?

The obvious near-term impact of various integrations across AMMs, Bridges, and CDPs is a fresh influx of liquidity into the Filecoin ecosystem. Liquidity begets deeper liquidity with an increase in the number and diversity of DeFi protocols on Filecoin. DeFi’s growing economy clubbed with more services coming on-chain and utilizing FVM for payments will overall increase the revenue and utility of the network. We expect this strong DeFi traction to scale Filecoin as an L1 ecosystem, with core services of storage and compute becoming the backbone of the decentralized internet.

To stay updated on the latest Filecoin happenings, follow the @Filecointldr handle.

Many thanks to HQ Han and Jonathan Victor for reviewing and providing valuable insights and to all the ecosystem partners and teams for their timely input.

Disclaimer: This information is for informational purposes only and is not intended to constitute investment, financial, legal, or other advice. This information is not an endorsement, offer, or recommendation to use any particular service, product, or application.

Editor’s Note: This blog is a repost of original content from IOSG Ventures. IOSG Ventures is a community-friendly and research-driven early-stage venture firm. This blog post represents the independent views of the author, who has given permission for re-publication.

The programmable layer on FIL, the FVM, allows for trustless marketplaces to be built

This calls for a need for a marketplace that currently exists off-chain, i.e. FIL borrowing to be brought on-chain, where FIL token holders lease their FIL to Storage Providers (which some call “miners”) who borrow FIL from the pool(s)

FIL borrowing is essentially taking cash forward on the future block rewards accrued by the Storage Providers, and this makes FIL block rewards from data storage more capital-efficient

There are obvious trade-offs to be made between centralization-capital efficiency- and security in protocol design

The market size for borrowing FIL is reducing over time but the introduction of stablecoins, etc. Can unlock unique projects to be built on top of these protocols

The launch of a programmability layer on a seasoned blockchain generally comes with a lot of excitement. The launch of Stacks (STX) on the Bitcoin blockchain brought a new paradigm of thinking amongst the community built around it.

A very similar narrative happened with the launch of the FVM on Filecoin. The robust Filecoin community now has to see its vision through a completely different lens. A lot of open problems that the ecosystem had could now be addressed. Creating trustless marketplaces via programmability was a key piece of the puzzle.

Liquid staking on Filecoin was the first “Request-for-build” from the Filecoin ecosystem during the launch of FVM and was given high importance. To understand why this is, let us first understand how the economics of Filecoin work.

How Filecoin Incentives Work

Unlike an Ethereum validator, there is no one-time staking in Filecoin. Every time a Storage Provider (SP) provides services, they need to put up a pledge amount in FIL. This pledge is required to seal the sectors and store the sealed sector in the SP. Such a structure ensures that the SP is going to store data for their clients for the period of the deal that they agree to, in exchange for rewards. Rewards are distributed via PoSt (Proof of Space-Time), where the SPs are rewarded for proving that they have the right client data stored.

SPs are selected via a leader selection mechanism called DRAND. DRAND chooses the leader with some initial requirements and also the % of raw byte power of the network controlled by the SPs.

SPs will have to keep ramping up raw byte power (RBP) to be chosen as the leader to “mine” a block and receive incentives. This helps the SP subsidize their storage costs.

Although there are many more factors that govern the supply rate of these incentives, the baseline is that for storage providers/miners, to maximize their bottom line will have to try to maximize RBP and onboard (and renew) more deals.

This creates a positive loop for the Filecoin network

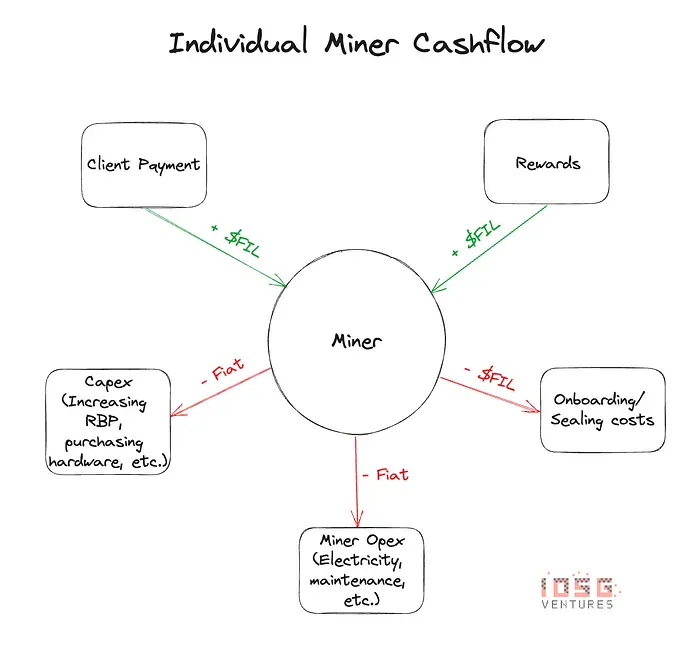

Economics of a Storage Provider

When an SP receives block rewards, these rewards are not liquid. Only 25% of the rewards are liquid, and the remaining 75% of the block rewards vest linearly over 180 days (~ 6 months). This poses a problem for SPs. The rewards, which are supposed to be an SP’s operating income, are now delayed payments for as long as the SP onboards/renews deals.

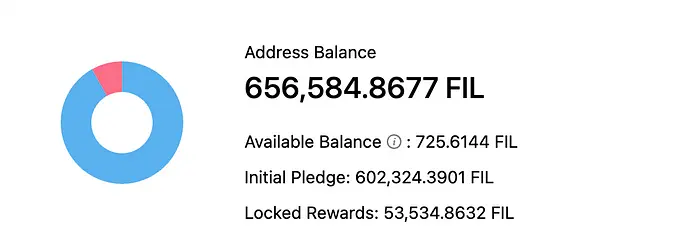

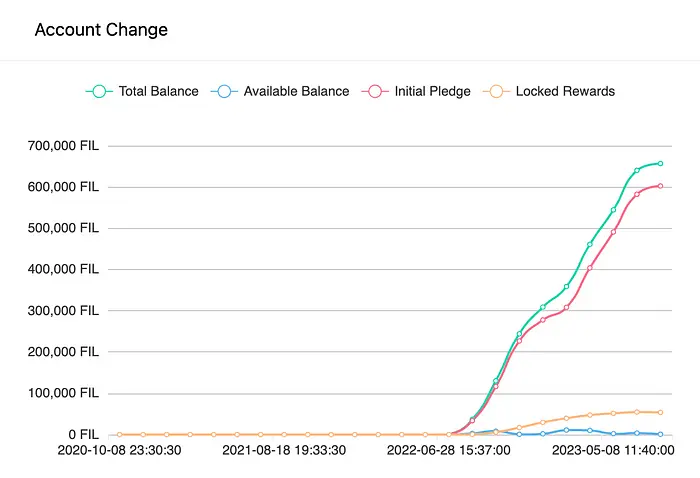

Let us look at the SP balance of the top miner in the network (as of 6th August 2023)

When you look at the graph, one can see that only about 1% of the rewards (or operating income) of the SP is actually liquid. If this SP now wants to either:

Pay for operating income

Upgrade hardware

Pay for maintenance

Or onboard/ renew deals

The SP will have to either borrow fiat currency or borrow FIL from third parties just to make up for these “delayed” payments.

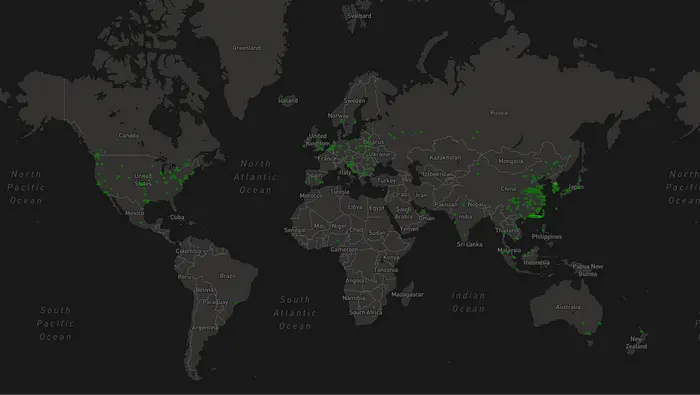

At the moment many storage providers (miners) in the network rely on CeFi lenders such as DARMA Capital, Coinlist, and a few others. As these are loan products, storage providers will have to go through KYC and a strict audit process to be able to borrow FIL. When we look at the map below, we can see a very high concentration of Filecoin SPs in Asia, and with centralized providers being mostly in the West, it is very hard for them to underwrite FIL loans to Asian miners with favorable terms, and most Asian miners/ SPs don’t have access to such providers.

This becomes a hindrance for new SPs to come in and participate in the system, and existing SPs can scale their business only as much as the total FIL pool size of these CeFi lenders

So why not just borrow fiat currency from a bank? With FIL being a volatile asset, it will pose additional capital management challenges for SPs who borrow.

To solve this problem, there needs to be a marketplace for FIL lenders (who could be holders of FIL) and FIL borrowers (SPs)

Filecoin Staking

With the launch of the FVM, this marketplace idea can come to fruition. FIL lenders/stakers can now put their FIL to work and SPs can borrow from this pool (either in a permissioned or permissionless manner) all governed by smart contracts.

There are many players in the ecosystem who are already building this and waiting to launch in the coming months.

More than calling such marketplaces staking protocols, it is a lot closer to a lending protocol by the nature of this business.

Some base features of such a FIL lending product would be:

Lenders deposit idle FIL and receive a “liquid staking” token

Borrowers (SPs) can borrow from the pool against collateral that exists in the SP actor (Essentially Initial Pledge + Locked Rewards)

Borrowers will make interest payments every week, or any specified time period, by signing over the “OwnerID” of the SP to a smart contract

Lenders receive the interest (minus protocol fees) as APY either via a rebase token or a value accrual token

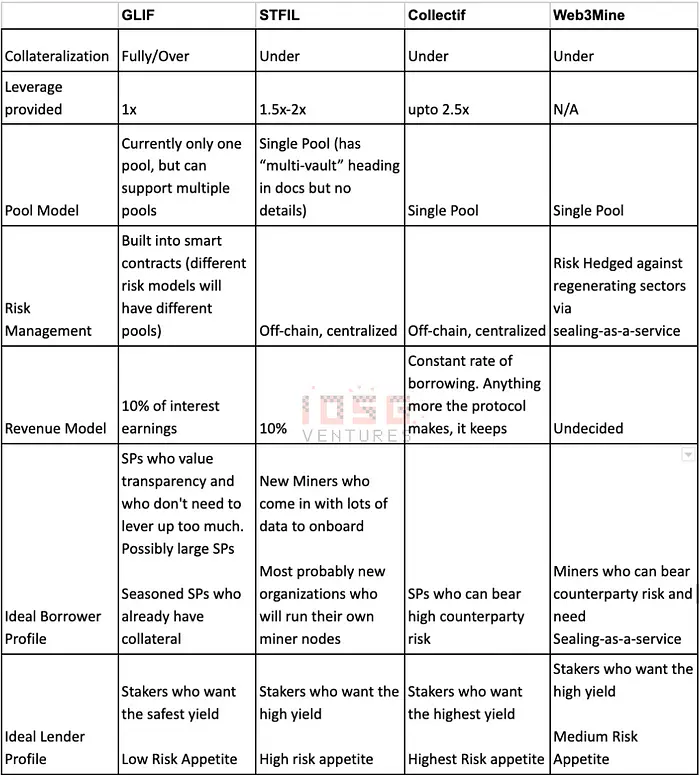

Different liquid staking protocols have different schools of thought when it comes to borrowing:

Over/ Fully collateralized vs. Undercollateralized

In Over-collateralized or fully collateralized models, the debt-to-equity ratio is always going to be less than or equal to 100%. This means that if my SP balance is say 1000 FIL, I can only borrow up to 1000 FIL (depending on the protocol rules as well). This can easily be coded into smart contracts and default risk is built in. This allows for greater transparency and also security to the stakers (lenders). Another advantage of such a model is that it allows for permissionless borrowing as well. This is where the product blocks more like Aave/ Compound rather than a Lido or RocketPool.

In an uncollateralized model, the lenders are bearing risk while the risk is being managed by the protocol. In such a model, risk modeling is complex math that cannot be baked into smart contracts, and needs to be off-chain which sacrifices transparency. But, since there is leverage involved, it makes the system a lot more capital-efficient for the borrower. The more permissionless a leveraged system will get, the more risk the lenders bear and this would call for a very robust and dynamic risk management model that is run by the protocol developers

The trade-offs being made are:

Capital efficiency vs. staker risk

Capital efficiency vs. transparency

Lender risk vs. borrower entry to the system

Single Pool vs Multi-Pool

Protocols can also opt to build a multi-pool model where lenders can choose to stake FIL in different pools with different risk parameters. This allows for risk to be managed on-chain, but liquidity will be fragmented. In a single-pool model, risk will have to be maintained off-chain. Overall the trade-offs will still remain the same as the ones mentioned above.

Trade-off: Liquidity fragmentation vs Risk management transparency

Risks

In an overcollateralized model, even if the miner gets slashed multiple times, as soon as the Debt-to-equity ratio hits 100% the miner will get liquidated and the stakers will be comparatively safe

In an undercollateralized model, the borrowers can be penalized for failing to prove sectors. There are many more faults in failing to prove data storage rather faults in the consensus itself. This is more common in Filecoin than in other general-purpose blockchains because there is an actual commodity that is being stored from an off-chain entity. This will affect the collateral value and lever the borrower more. Liquidation thresholds will have to be set very carefully in such a model.

What about Ethereum Staking/Lending protocols entering the market?

In the Filecoin ecosystem, unlike the Ethereum ecosystem, the nodes (Miners/Validators/SPs) are responsible for much more than general uptime. They are supposed to market themselves to be chosen as SPs, and regularly upgrade their hardware to support more storage, seal, store, maintain, and retrieve data. Filecoin storage and reward mining for SPs is a full-time job.

Unlike an Ethereum validator, there is no one-time staking in Filecoin. Every time an SP provides storage to a client, they need to put up a pledge. This pledge is required to seal the sectors and store the sealed sector in the SP. Storage provision on Filecoin is a very capital-intensive process and this discourages many new SPs from participating in the network and existing SPs from staying and contributing to the network.

Since the participants on the borrow side are SPs only it is also going to be intensive for newcomers in the Filecoin ecosystem to bootstrap borrower trust.

The mechanics of Filecoin alone don’t allow Ethereum staking or even lending protocols to deploy easily on the FVM.

Economics of the Protocol

Is there enough FIL in the market to supply for lending?

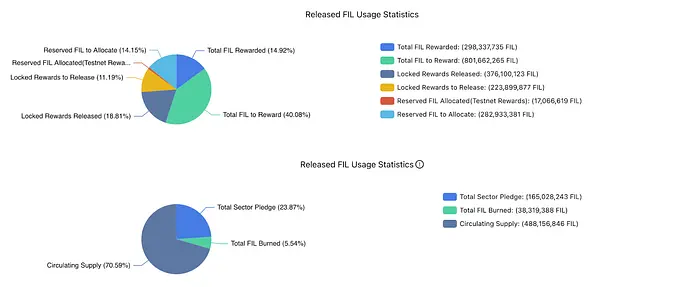

As of August 6th, 2023, there are about 264.2 million FIL circulating that are not committed as sector pledges or rewards that are to be released. This can be counted as the total amount of FIL that can be staked by the lenders into the pool

While FIL borrowing is essential to SPs, what are they actually borrowing? They are taking a forward payment on their locked-up rewards in an overcollateralized model, and in the undercollateralized model, they are taking a forward payment on future rewards.

Looking at the graphs above, we can see that the total locked rewards are about 223M FIL, and the supply can match the demand. The demand-to-supply ratio is almost 84%. This shows even power dynamics on either side, and either side cannot squeeze the other on interest rates/ APY.

What does the future look like?

Estimating the market for future demand of FIL for borrowing is essentially the amount of FIL that will be released in the future as rewards.

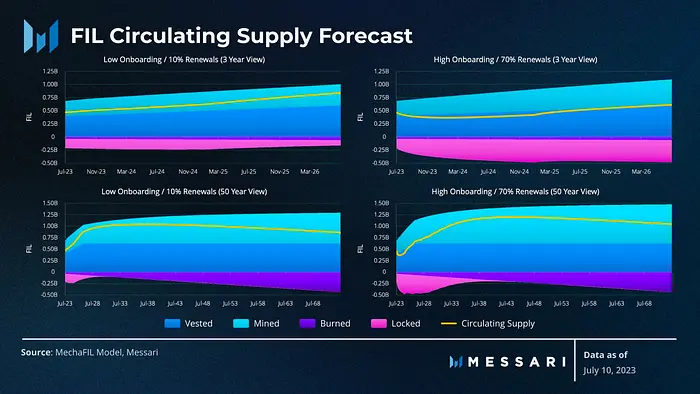

The good folks at Messari ran a simulation of FIL circulating supply with a 3-year and a 50-year forecast using different cases.

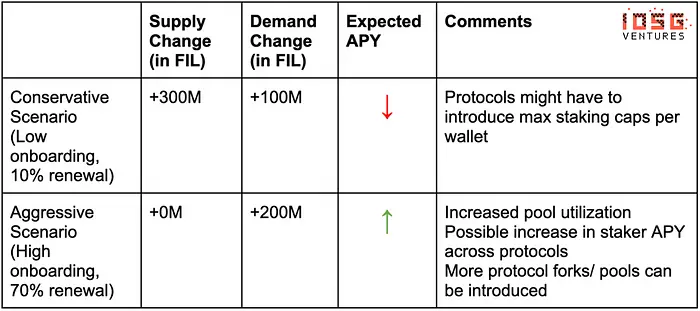

According to the top left graph, considering a conservative scenario where there is low onboarding of data and only 10% of the total deals are renewed, the new reward emissions over 3 years are close to around 100M FIL and in an aggressive scenario where there is a high amount of data onboarding and 70% of existing deals renewed, the extra rewards come to about 200M FIL

So one can expect a market size of somewhere between 100M — 200M FIL over the next 3 years. At the current price of FIL (Aug 6th), which is $4.16, there could be a borrowing TAM of about $400M — $800M. This could be counted as the TAM of the product’s borrow side.

On the supply side, in the conservative estimate, there can be about 300M FIL that will be emitted, and in a more aggressive scenario, the circulating supply is simulated to be around the same as it is today. Why? It is because if more deals are being onboarded and renewed, there will be a lot more FIL locked-in sector pledges.

In the more aggressive scenario, the demand is going to outweigh the supply and the interest charged can be higher in this competitive market.

Where I think this can go

Amongst the different designs, there need not be a winner-takes-all type of model. Intuitively, the long-term winner (by TVL) is generally the protocol that is built most safely. Very much like Lido in the Ethereum ecosystem. I for one am biased towards safer structures more than optimizing for 2–3% more yield, and I think FIL whales would also prioritize capital safety over a slightly higher yield.

This is after considering the amount of penalties miners pay for not being able to prove space-time.

From the borrower (SP) end, the SP could borrow from different protocols for different purposes. If the SP already has a lot of collateral and doesn’t need to lever up to pay for opex, then the safer, overcollateralized model will work better, since it is safer. Whereas if I am a newer SP with a lot of sectors to be pledged I would borrow with leverage from an undercollateralized pool.

After studying the above models, we can see:

Staking in Filecoin is important to bridge the supply and demand for FIL in the ecosystem. The FVM has recently been released allowing for a lending marketplace to exist. Although the problem is real, the FVM release was probably too late for most FIL staking/lending protocols as the pie (mining rewards) is decreasing over time making it a niche market.

However, a few fascinating use cases can emerge on top of these staking protocols. With the introduction of stablecoins, the rewards can be taken as cash forwards. Something similar to what Alkimiya is building on Ethereum. This can result in the injection of new capital into the Filecoin ecosystem and also increase the TVL in these protocols.

Ethereum’s and Filecoin’s tech is different, their miners are different, their developers are different, their apps are different, and hence their communities. And for staking in particular, with every miner being “non-fungible” bootstrapping the demand side becomes a BD exercise and the success of it is directly proportional to the protocol’s reputation in the community.

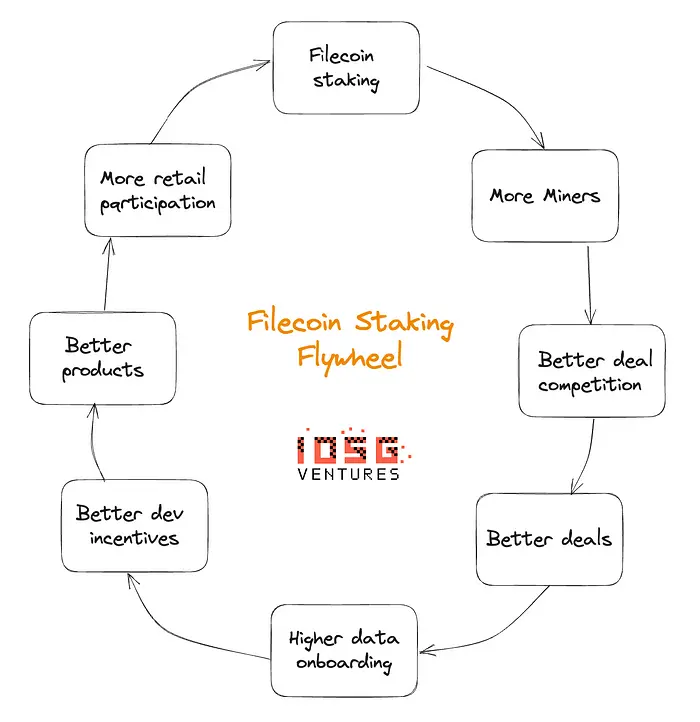

Filecoin staking is a critical solution that needs to be built to get more SPs in the system, for retail to put their capital to work, create greater economic incentives as an ecosystem to attract more developers, and build useful products to build a positive flywheel. To know more beyond staking in the Filecoin ecosystem and the criticality of the FVM you can read this previous piece we published.

There are many more open problems to be solved in the Filecoin ecosystem, but we are positive that the Filecoin Ecosystem is working in the right direction to achieve its vision of storing humanity’s data in an efficient system.

Unlike proof-of-stake cryptocurrency protocols that directly provide rewards for locking staked tokens, “staking” FIL is much more akin to a lease.

You may have heard of services or applications that enable “Filecoin staking.” However, “staking” on the Filecoin network is different from proof-of-stake cryptocurrency protocols like Ethereum. Filecoin “staking” allows storage providers (SPs) to borrow FIL which they use as collateral to provide storage on the Filecoin network.

Unlike proof-of-stake cryptocurrency protocols that directly provide rewards for locking staked tokens, “staking” FIL is much more akin to a lease. SPs borrow FIL to use as collateral and may pay a fee. Applications facilitating this may also take a fee.

You can think of a FIL lease to a storage provider like a car being leased to an Uber driver who makes money providing rides through the Uber platform. During the lease term, the car owner receives lease payments from the Uber driver; when the lease is over, the car is returned to the owner.

Why do storage providers need FIL collateral?

Filecoin storage providers (SPs) contribute data storage capacity to the Filecoin network.

In order to ensure that files are stored reliably over time, SPs are required to post FIL as collateral. If an SP fails to meet their responsibilities (perhaps they go offline or stop storing certain files) their collateral is slashed, meaning that they lose a portion of the FIL they posted as collateral.

A storage provider can buy or earn FIL to provide the collateral they need to run their data storage business, or they might borrow/lease FIL from existing token holders.

Centralized vs decentralized applications

Third-party centralized programs enable storage providers to borrow FIL to use as collateral. In the centralized model, token holders transfer custody of their FIL to centralized intermediaries for set periods of time. These intermediaries allow SPs to borrow FIL, and distribute fees collected to token holders.

This model requires that token holders trust the centralized intermediary with custody of their FIL. Some centralized programs rely on multi-sig transactions. Multi-sig is short for ‘multi-signature’, which means a transaction has two, or more, signatures before it is executed. However, multi-sigs still rely on human intervention.

Using any third-party application carries risks, and it is critical to thoroughly research any application to understand all these risks. Some areas to consider are:

Audits: Has a third-party audited the code and are the results published publicly?

Open Source: Is the code available to inspect publicly?

Bug Bounty: Does the program provide a bug bounty to incentivize anyone to report/fix possible vulnerabilities?

Trustless: Can you use the application without relying on an intermediary; is there a single point of failure?

Disclaimer: This information is for informational purposes only and does not constitute investment, financial, legal, or other advice. This information is not an endorsement, offer, or recommendation to use any particular service, product, or application.