Editor’s Note: This blogpost is a repost of the original content published on 5 April 2024, by Turan VuralYuki Yuminaga from Fenbushi Capital. Established in 2015, Fenbushi Capital holds the distinction of being Asia’s pioneering blockchain-focused asset management firm with an AUM of $1.6 billion. Through research and investment, the firm aims to play a vital role in shaping the future of blockchain tech across diverse sectors.This blogpost is an example of these efforts, and represents the independent view of these authors, whom have given permission for this re-publication.

Data availability (DA) is a core technology in the scaling of Ethereum, allowing a node to efficiently verify that data is available to the network without having to host the data in question. This is essential for the efficient building of rollups and other forms of vertical scaling, allowing execution nodes to ensure that transaction data is available during the settlement period. This is also crucial for sharding and other forms of horizontal scaling, a planned future update to the Ethereum network, as nodes will need to prove that transaction data (or blobs) stored in network shards are indeed available to the network.

Several DA solutions have been discussed and released recently (e.g., Celestia, EigenDA, Avail), all with the intent of providing performant and secure infrastructure for applications to post DA.

The advantage of an external DA solution over an L1 such as Ethereum is that it provides an inexpensive and performant vehicle for on-chain data. DA solutions often consist of their own public chains built to enable cheap and permissionless storage. Even with modifications, the fact remains that hosting data natively from a blockchain is extremely inefficient.

Thus, we find that it is intuitive to explore a storage-optimized solution such as Filecoin for the basis of a DA layer. Filecoin uses its blockchain to coordinate storage deals between clients and storage providers but allows data to be stored off-chain.

In this post, we investigate the viability of a DA solution built on top of a Distributed Storage Network (DSN). We consider Filecoin specifically, as it is the most adopted DSN to date. We outline the opportunities that such a solution would offer, and the challenges that need to be overcome to build it.

A DA layer provides the following to services relying on it:

Client Safety: No node can be convinced that unavailable data is available.

Global Safety: The un/availability of data is agreed upon by all except at most a small minority of nodes.

Efficient data retrievability.

All of this needs to be done efficiently to enable scaling. A DA layer provides higher performance at a lower cost across the three points above. For example, any node can request a full copy of the data to prove custody, but this is inefficient. By having a system that provides all three of these, we achieve a DA layer that provides the security required for L2s to coordinate with an L1, along with stronger lower bounds in the presence of a malicious majority.

Custody of Data

Data posted to a DA solution has a useful lifetime: long enough to settle disputes or verify a state transition. Transaction data needs to be available only long enough to verify a correct state transition or to give validators enough opportunity to construct fraud proofs. As of writing, Ethereum calldata is the most common solution used by projects (rollups) requiring data availability.

Efficient Verification of Data

Data Availability Sampling (DAS) is the standard method of answering the question of DA. It comes with additional security benefits, strengthening network actors’ ability to verify state information from their peers. However, it relies on nodes to perform sampling: DAS requests must be answered to ensure mined transactions won’t be rejected, but there is no positive or negative incentive for a node to request samples. From the perspective of nodes that request samples, there is no negative penalty for not performing DAS. As an example, Celestia provides the first and only light client implementation to perform DAS, delivering stronger security assumptions to users and reducing the cost of data verification.

Efficient Access

A DA needs to provide efficient access to data to the projects using it. A slow DA may become the bottleneck for the services relying on it, causing inefficiencies at best and system failures at worst.

Decentralized Storage Network

A Decentralized Storage Network (DSN, as formalized in the Filecoin Whitepaper¹) is a permissionless network of storage providers that offer storage services for users of the network. Informally, it allows independent storage providers to coordinate storage deals with clients that need storage services and provides cheap and resilient data storage to clients seeking storage services at a low price. This is coordinated through a blockchain that records storage deals and enables the execution of smart contracts.

A DSN scheme is a tuple of three protocols: Put, Get, and Manage. This tuple comes with properties such as fault tolerance guarantees and participation incentives.

Put(data) → key Clients execute Put to store data under a unique key. This is achieved by specifying the duration for which data will be stored on the network, the number of replicas of the data that are to be stored for redundancy, and a negotiated price with storage providers.

Get(key) → data Clients execute Get to retrieve data that is being stored under a key.

Manage() The Manage protocol is called by network participants to coordinate the storage space and services made available by providers and repair faults. In the case of Filecoin, this is managed via a blockchain. This blockchain records data deals being made between clients and data providers and proofs of correctly stored data to ensure that data deals are being upheld. Correctly stored data is proved via the posting of proofs generated by data providers in response to challenges from the network. A storage fault occurs when a storage provider fails to generate a Proof-of-Replication or Proof-of-Spacetime promptly when requested by the Manage protocol, which results in the slashing of the storage provider’s stake. Deals can self-heal in the case of a storage fault if more than one provider is hosting a copy of the data on the network by finding a new storage provider to honor the storage deal.

DSN Opportunities

The work done thus far in DA projects has been to transform a blockchain into a platform for hot storage. Since a DSN is storage-optimized, rather than transforming a blockchain into a storage platform, we can simply transform a storage platform into one that provides data availability. The collateral of storage providers in the form of native FIL token can provide crypto-economic security that guarantees data is stored. Finally, the programmability of storage deals can provide flexibility around the terms of data availability.

The most compelling motivation to transform the capabilities of a DSN to solve DA is the cost reduction in the data storage under the DA solution. As we discuss below, the cost of storing data on Filecoin is significantly cheaper than storing data on Ethereum. Given current Ether/USD prices, it costs over 3 million USD to write 1 GB of calldata to Ethereum, only to be pruned after 21 days. This calldata expense can contribute to over half of the transaction cost of an Ethereum-based rollup. However, 1 GB of storage on Filecoin costs less than .0002 USD per month. Securing DA at this or any similar price would bring transaction costs down for users and contribute to the performance and scalability of Web3.

Economic Security

In Filecoin, collateral is required to make storage space available. This collateral is slashed when a provider fails to honor its deals or uphold network guarantees. A storage provider that fails to provide services faces losing both its posted collateral and any profit that would have been earned from providing storage.

Incentive Alignment

Many of Filecoin’s protocol incentives align with the goals of DA. Filecoin provides disincentives for malicious or lazy behavior: storage providers must actively provide proofs of storage during consensus in the form of Proof-of-Replicas and Proof-of-Spacetime, continuously proving that the storage exists without honest majority assumptions. Failure of a storage provider to provide proof results in stake slashing, and removal from consensus, among other penalties. Current DA solutions lack incentive for nodes to perform DAS, relying on ad-hoc altruistic behavior for proof of DA.

Programmability

The ability to customize data deals also makes a DSN an attractive platform for DA. Data deals can have varying durations, allowing users of a DSN-based DA to pay for only the DA that they need. Fault tolerance can also be tuned by setting the number of copies that are to be stored throughout the network. Further customization is supported via smart contracts on Filecoin (called Actors), which are executed on the FEVM. This leads to Filecoin’s growing ecosystem of DApps, from compute-over-storage solutions such as Bacalhau to DeFi and liquid staking solutions such as Glif. Retriev makes use of Filecoin Actors to provide incentive-aligned retrieval with permissioned referees. Filecoin’s programmability can be used to tailor DA requirements needed for different solutions, so that platforms that rely on DA are not paying for more DA than they need.

Challenges to a DSN-Based DA Architecture

In our investigation, we have identified significant challenges that need to be overcome before a DA service can be built on a DSN. As we now talk about the feasibility of implementation, we will use Filecoin as our main focus of the discussion.

Proof Latency

The cryptographic proofs that ensure the integrity of deals and stored data on Filecoin take time to prove. When data is committed to the network, it is partitioned into 32 gigabyte sectors and “sealed.” The sealing of data is the foundation of both the Proof-of-Replication (PoRep), which proves that a storage provider is storing one or more uniquecopies of the data, and Proof-of-Spacetime (PoST), which proves that a storage provider stored a unique copy continuously throughout the duration of the storage deal. Sealing has to be computationally expensive to ensure that storage providers aren’t sealing data on demand to undermine the required PoReP. When the protocol presents the periodic challenge to a storage provider to provide proof of unique and continuous storage, sealing has to safely take longer than the response window so that a storage provider can’t falsify proofs or replicas on the fly. For this reason, it can take providers approximately three hours to seal a sector of data.

Storage Threshold

Because of the computational expense of the sealing operation, the sector size of the data being sealed has to be economically worthwhile. The price of storage has to justify the cost of sealing to the storage provider, and likewise, the resulting cost of data being stored has to be low enough at scale (in this case, for an approximately 32GB chunk) for a client to want to store data on Filecoin. Although smaller sectors could be sealed, this would drive up the price of storage to compensate storage providers. To get around this, data aggregators collect smaller pieces of data from users to be committed to Filecoin as a chunk close to 32 GB. Data aggregators commit to user’s data via a Proof-of-Data-Segment-Inclusion (PoDSI), which guarantees the inclusion of a user’s data in a sector, and a sub-piece CID (pCID), which the user will be able to use to retrieve the data from the network.

Consensus Constraints

Filecoin’s consensus mechanism, Expected Consensus, has a block time of 30 seconds and finality within hours, which may improve in the near future (see FIP-0086 for fast finality on Filecoin). This is generally too slow to support the transaction throughput needed for a Layer 2 relying on DA for transaction data. Filecoin’s block time is lower-bounded by storage provider hardware; the lower the block time, the more difficult it is for storage providers to generate and provide proofs of storage, and the more storage providers will be falsely penalized for missing the proving window for the proper storage of data. To overcome this, InterPlanetary Consensus (IPC) subnets can be leveraged to take advantage of faster consensus times. IPC uses Tendermint-like consensus and DRAND for randomness: in the case that DRAND is the bottleneck, we would be able to achieve a 3-second block-time with an IPC subnet. In the case of a Tendermint bottleneck, PoCs such as Narwhal have achieved blocktimes in the hundreds of milliseconds.

Retrieval Speed

The final barrier-to-build is retrieval. From the constraints above, we can deduce that Filecoin is suitable for cold or lukewarm storage. However, the DA data is hot and needs to support performant applications. Incentive-aligned retrieval is difficult in Filecoin; data needs to be unsealed before it is served to clients, which adds latency. Currently, rapid retrieval is done via SLAs or the storage of un-sealed data alongside sealed sectors, neither of which can be relied on in the architecture of a secure and permissionless application on Filecoin. Especially with Retriev proving that retrieval can be guaranteed via the FVM, incentive-aligned rapid retrieval on Filecoin remains an area to be further explored.

Cost Analysis

In this section, we consider the cost that comes from these design considerations. We show the cost of storing 32GB as Ethereum calldata, Celestia blobdata, EigenDA blobdata, and as a sector on Filecoin using near-current market prices.

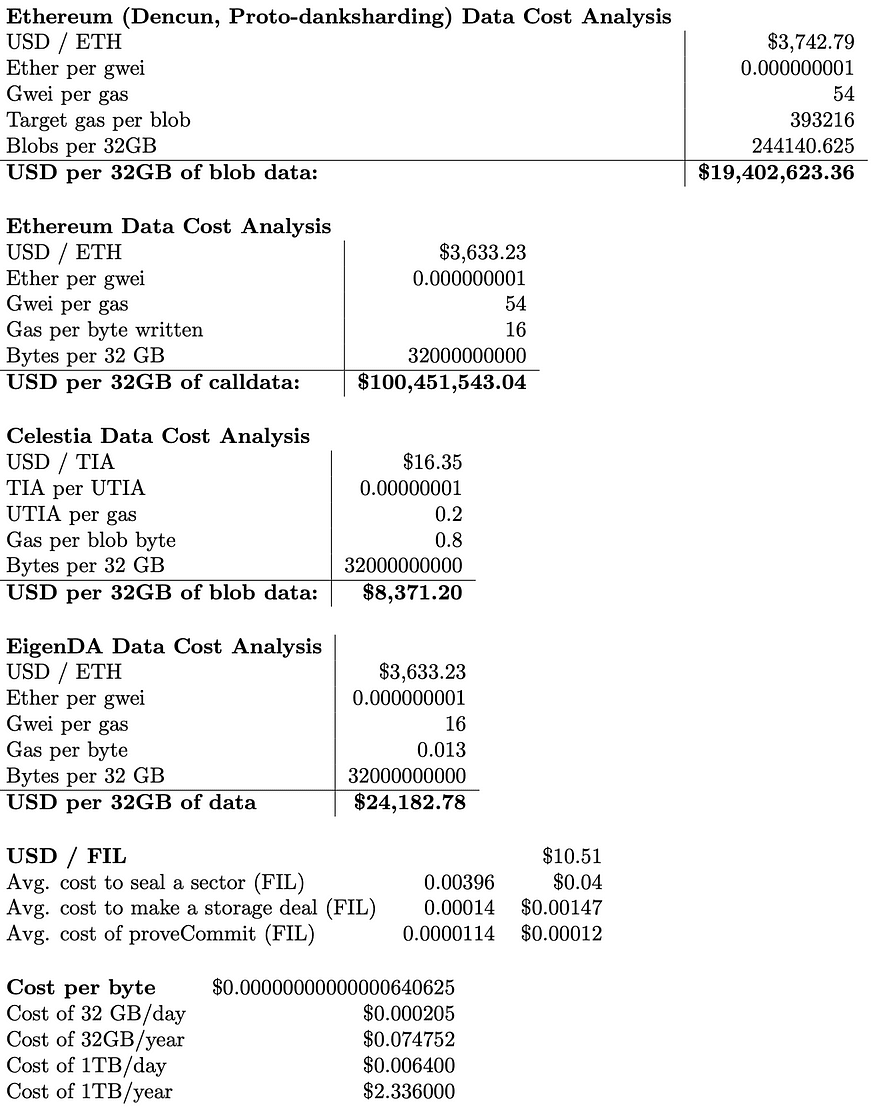

The analysis highlights the price of Ethereum calldata: 100 million USD for 32 GB of data. This price showcases the cost of security behind Ethereum’s consensus, and is subject to the volatility of Ether and gas prices. The Dencun upgrade, which introduced Proto-Danksharding (EIP-4844), introduced blob transactions with a target of 3 blobs per block of approximately 125 KB each, and variable gas blob pricing to maintain the target amount of blobs per block. This upgrade cut the cost of Ethereum DA by ⅕: 20 million USD for 32 GB of blob data.

Celestia and EigenDA provide significant improvements: 8,000 and 26,000 USD for 32 GB of data, respectively. Both are subject to the volatility of market prices and reflect to some extent the cost of consensus securing their data: Celestia with its native TIA token, and EigenDA with Ether.

In all of the above cases, the data stored is not permanent. Ethereum calldata is stored for 3 weeks, with blobs stored for 18 days. EigenDA stores blobs for a default of 14 days. As of the current Celestia implementation, blob data is stored indefinitely by archival nodes but only sampled by light nodes for a maximum of 30 days.

The final two tables are direct comparisons between Filecoin and current DA solutions. Cost equivalence first lists the cost of a single byte of data on the given platform. The amount of Filecoin bytes that can be stored for the same amount of time for the same cost is then shown.

This shows that Filecoin is orders of magnitude cheaper than current DA solutions, costing fractions of a cent to store the same amount of data for the same amount of time. Unlike Ethereum nodes and that of other DA solutions, Filecoin’s nodes are optimized to provide storage services, and its proof system allows nodes to prove storage, rather than replicate storage across every node in the network. Without accounting for the economics of storage providers (such as the energy cost to seal data), it shows that the basic overhead of the storage process on Filecoin is negligible. This shows a market opportunity in the millions of USD per gigabyte compared to Ethereum for a system that can provide secure and performant DA services on Filecoin.

Throughput

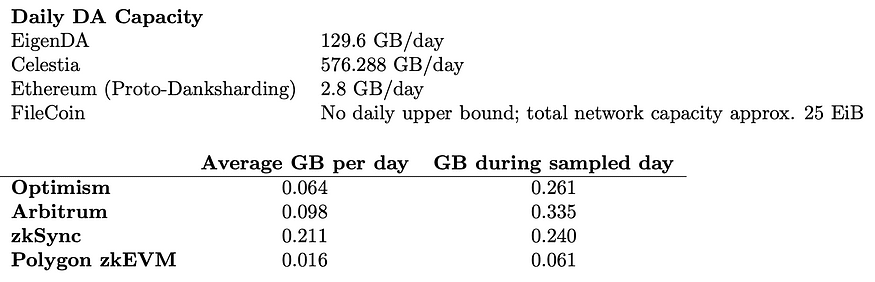

Below, we consider the capacity of DA solutions and the demand that is generated by major layer 2 rollups.

Because Filecoin’s blockchain is organized in tipsets with multiple blocks at every block-height, the number of deals that can be done is not restricted by consensus or block size. The strict data constraint of Filecoin is that of its network-wide storage capacity, not what is allowed via consensus.

For daily DA demand, we pull data from Rollups DA and Execution from Terry Chung and Wei Dai, which includes a daily average across 30 days and a singular sampled day. This allows us to consider average demand while not overlooking aberrations from the average (for example, Optimism’s demand on 8/15/2023 of approximately 261,000,000 bytes was over 4x its 30 day average of 64,000,000 bytes).

From this selection, we see that despite the opportunity of lower DA cost, we would need a dramatic increase in DA demand to make efficient use of the 32 GB sector size of Filecoin. Although sealing 32 GB sectors with less than 32 GB of data would be a waste of resources, we could do so while still reaping a cost advantage.

Architecture

In this section, we consider the technical architecture that can be achieved if we were to build this today. We will consider this architecture in the context of arbitrary L2 applications and an L1 chain that the L2 is serving. Since this solution is an external DA solution, like that of Celestia and EigenDA, we do not consider Filecoin as example L1.

Components

Even at a high-level, a DA on Filecoin will make use of many different features of the Filecoin ecosystem.

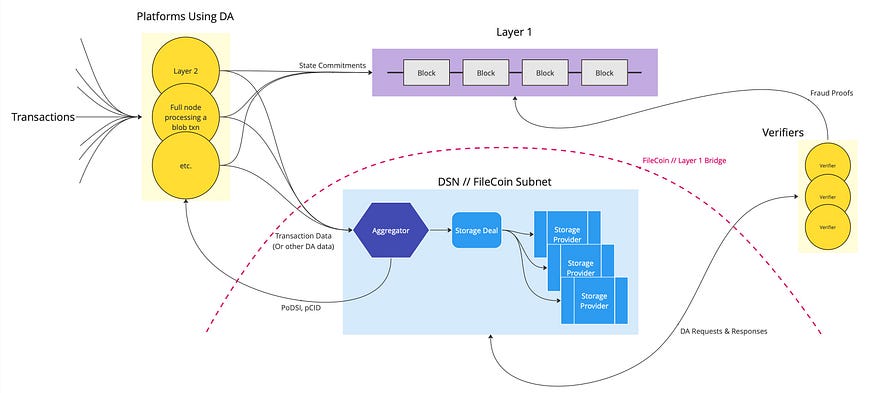

Transactions: Downstream users make transactions on a platform that requires DA. This could be an L2.

Platforms Using DA: These are the platforms that use DA as a service. This could be an L2 which posts transaction data to the Filecoin DA and commitments to an L1, such as Ethereum.

Layer 1: This is any L1 that contains commitments pointing to data on the DA solution. This could be Ethereum, supporting an L2 that leverages the Filecoin DA solution.

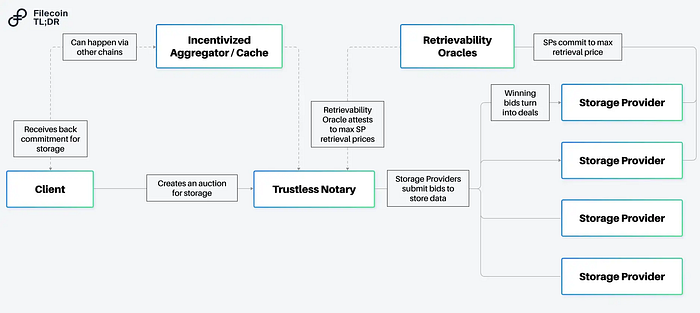

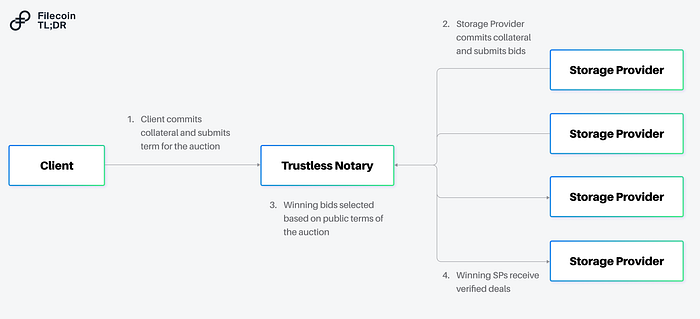

Aggregator: The frontend of Filecoin-based DA solution is an aggregator, a centralized component which receives transaction data from L2’s and other DA clients and aggregates them into 32 GB sectors suitable for sealing. Although a simple proof-of-concept would include a centralized aggregator, platforms using the DA solution could also run their own aggregator,for example as a sidecar to an L2 sequencer. The centralization of the aggregator can be seen as similar to that of an L2 sequencer or EigenDA’s disperser. Once the aggregator has compiled a payload near 32GB, it makes a storage deal with storage providers to store the data. Clients are given a guarantee that their data will be included in the sector in the form of a PoDSI (Proof of Data Segment Inclusion), and a pCID to identify their data once it is on the network. This pCID is what would be included in the state commitments on the L1 to reference supporting transaction data.

Verifiers: Verifiers request the data from the storage providers to ensure the integrity of state commitments and build fraud proofs, which are committed to the L1 in the case of provable fraud.

Storage Deal: Once the aggregator has compiled a payload near 32GB, the aggregator makes a storage deal with storage providers to store the data.

Posting blobs (Put): To initiate a put, a DA client will submit their blob containing transaction data to the aggregator. This can be done in an off-chain manner, or an on-chain manner via an on-chain aggregator oracle. To confirm receipt of the blob, the aggregator returns a PoDSI to the client to prove that their blob is included in the aggregated sector that will be committed to the subnet. A pCID (sub-piece Content IDentifier) is also returned. This is what the client and any other interested party will use to reference the blob once it is being served on Filecoin.

Data deals would appear on-chain within minutes of the deal being made. The largest barrier to latency is the sealing time, which can take 3 hours. This means that although the deal has been made, and the client can be confident that the data will appear in the network, the data cannot be guaranteed to be queryable until the sealing process is complete. The Lotus client has a fast-retrieval feature in which an unsealed copy of the data is stored alongside the sealed copy that may be able to be served as soon as the unsealed data is transferred to the data storage provider, as long as a retrieval deal does not depend on the proof of sealed data to appear on the network. However, this functionality is at the discretion of the data provider, and is not cryptographically guaranteed as part of the protocol. If a fast-retrieval guarantee is to be provided, there would need to be changes to consensus and dis/incentive mechanisms in place to enforce it.

Retrieving blobs (Get): Retrieval is similar to a put operation. A retrieval deal needs to be made, which will appear on-chain within minutes. Retrieval latency will depend on the terms of the deal and whether an unsealed copy of data is stored for fast retrieval. In the fast retrieval case, the latency will depend on network conditions. Without fast retrieval, data will need to be unsealed before being served to the client, which takes the same amount of time as sealing, on the order of 3 hours. Thus without optimizations we have a maximum round-trip of 6 hours, major improvement in data serving would need to be made before this becomes a viable system for DA or fraud proofs.

Proof of DA: proof of DA can be considered in two steps; via the PoDSI that is given when the data is committed to the aggregator while the deal is being made and then the continued commitment of PoRep and PoST that storage providers provide via Filecoin’s consensus mechanism. As discussed above, the PoRep and PoST give scheduled and provable guarantees of data custody and persistence.

This solution will make heavy use of bridging, as any client that relies on DA (regardless of the construction of proofs) will need to be able to interact with Filecoin. In the case of the pCID included in the state transition that is posted to the L1, a verifier can make an initial check to make sure that a bogus pCID wasn’t committed. There are several ways that this could be done, for example, via an oracle that posts Filecoin data on the L1 or via verifiers that verifies the existence of a data deal or sector that corresponds to the pCID. Likewise, the verification of validity or fraud proofs that get posted to the L1 may need to make use of a bridge to be convinced of a proof. Current available bridges are Axelar and Celer.

Security Analysis

Filecoin’s integrity is enforced through the slashing of collateral. Collateral can be slashed in two cases: storage faults or consensus faults. A storage fault corresponds to a storage provider not being able to provide proof of stored data (either PoRep or PoST), which would correlate to a lack of data availability in our model. A consensus fault corresponds to malicious action in consensus, the protocol that manages the transaction ledger from which the FEVM is abstracted.

A Sector Fault refers to the penalty incurred from the failure to post proof of continuous storage. Storage providers are allowed a one-day grace period during which a penalty is not incurred for faulty storage. After 42 days from a sector becoming faulty, the sector is terminated. Incurred fees are burnt.

A Sector Termination occurs after a sector has been faulty for 42 days or a storage provider purposefully terminates a deal. Termination fees are equivalent to the maximum amount that a sector has earned up to termination, with an upper bound of 90 days’ worth of earning. Unpaid deal fees are returned to the client. Incurred fees are burnt.

Storage Market Actor Slashing occurs in the event of a terminated deal. This is the slashing of the collateral that the storage provider puts up behind the deal.

The security provided by Filecoin is very different from that of other blockchains. Whereas blockchain data is typically secured via consensus, Filecoin’s consensus only secures the transaction ledger, not the data referred to by the transaction. The data that is stored on Filecoin has only enough security to incentive-align storage providers to provide storage. This means that the data stored on Filecoin is secured via fault penalties and business incentives such as reputation with clients. In other words, a data fault on a blockchain is equivalent to a breach of consensus, and breaks the safety of the chain or its notion of the validity of transactions. Filecoin is designed to be fault tolerant when it comes to data storage, and therefore only uses its consensus to secure its dealbook and deal-related activities. The cost of a storage miner not fulfilling its data deal has a maximum of 90 days worth of storage reward in penalties, and the loss of the collateral put up by the miner to secure the deal.

Therefore, the cost of a data withholding attack being launched from Filecoin providers simply the opportunity cost a retrieval deal. Data retrieval on Filecoin relies on the storage miner being incentivized by a fee paid for by the client. However, there is no negative impact to a miner for not responding to a data retrieval request. To mitigate the risk of a single storage miner ignoring or refusing data retrieval deals, data on Filecoin can be stored by multiple miners.

Since the economic security behind the data being stored on Filecoin is considerably less than that of blockchain based solutions, the prevention of data manipulation must also be considered. Data manipulation is protected via Filecoin’s proof system. Data is referred to via CIDs, through which data corruption is immediately detectable. A provider therefore cannot serve corrupt data, as it is easy to verify whether the fetched data matches the requested CID. Data providers cannot store corrupted data in the place of uncorrupted data. Upon the receipt of client data, providers must provide proof of a correctly sealed data sector to initiate the data deal (check this). Therefore, a storage deal cannot be started with corrupt data. During the lifetime of the storage deal, PoSTs are provided to prove custody (recall that this proves both custody of the sealed data sector and custody since the last PoST). Since the PoST is reliant on the sealed sector at the time of proof generation, a corrupt sector would result in a bogus PoST, resulting in a sector failure. Therefore, a storage provider can neither store nor serve corrupted data, cannot claim reward for services provided for uncorrupted data, and cannot avoid being penalized for tampering with a client’s data.

Security can be strengthened through increasing the collateral committed by the storage provider to the Storage Market Actor, which is currently decided by the storage provider and the client. If we assume that this was sufficiently high enough (for example, the same stake as an Ethereum validator) to incentivize a provider not to default, we can think of what is left to secure (even though this would be extremely capital-inefficient, as this stake would be needed to secure each transaction blob or sector with aggregated blobs). Now, a data provider could choose to make data unavailable for maximums of 41-day chunks before the storage deal is terminated by the Storage Market Actor. Assuming a shorter data deal, we could assume that the data can be made unavailable until the last day of the deal. In the absence of coordinated malicious actors, this can be mitigated via replication on multiple storage providers so that the data can continue being served.

We can consider the cost of an attacker overriding consensus to either accept a bogus proof or rewrite ledger history to remove a deal from the orderbook without penalizing the responsible storage provider. It is worth noting however that in the case of such a safety violation, an attacker would be able to manipulate Filecoin’s ledger however they want. In order for an attacker to commit such an attack, they would need at least a majority stake in the Filecoin chain. Stake is related to storage provided to the network; with a current 25 EiB (10¹⁶ bytes) of data securing the Filecoin chain, at least 12.5 EiB would be needed for a malicious actor to offer its own chain that would win the fork-choice rule. This is further mitigated by slashing related to consensus faults, for which the penalty is the loss of all pledged collateral and block rewards and all suspension from participation in consensus.

Aside: Withholding attacks on other DA solutions Although the above shows that Filecoin is lacking in protecting data from withholding attacks, it is not alone.

Ethereum: In general, the only way to guarantee that a request to the Ethereum network is answered is to run a full node. Full nodes have no requirements to fulfill data retrieval requests outside of consensus — and therefore. Constructs such as PeerDAS introduce a peer scoring system for a node’s responses to data retrieval in which a node with a low enough score (essentially a DA reputation) could be isolated from the network.

Celestia: Even though Celestia has much stronger security per-byte against withholding attacks in comparison to our Filecoin construction, the only way to take advantage of this security is to host your own full node. Requests to Celestia infrastructure that are not owned and operated in-house can be censored without penalty.

EigenDA: Similar to Celestia, any service can run an EigenDA Operator node to ensure retrieval of their own data. As such, any out protocol data retrieval request can be censored. Also note that EigenDA has a centralized and trusted dispenser in charge of data encoding, KZG commitment, and data dispersal, similar to our aggregator.

Retrieval Security

Retrievability is necessary for DA. Ideally, market forces motivate economically rational miners to accept retrieval deals, and compete with other miners to keep prices for clients low. It is assumed that this is enough for data providers to provide retrieval services, however given the importance of DA, it is reasonable to require more security.

Retrieval is currently not guaranteed via the economic security stipulated above. This is because it is cryptographically difficult to prove that data wasn’t received by a client (in the case where a client needs to refute a storage miner’s claim of sending data) in a trust-minimized manner. A protocol-native retrieval guarantee would be required in order for retrieval to be secured through the Filecoin’s economic security. With minimal changes to the protocol, this means that retrieval would need to be associated with a sector fault or deal termination. Retriev is a proof-of-concept which was able to provide data retrieval guarantees by using trusted “referees” to mediate data retrieval disputes.

Aside: Retrieval on other DA solutions As can be seen above, Filecoin lacks the protocol-native retrieval guarantees necessary to keep storage (or retrieval providers) from acting selfishly. In the case of Ethereum and Celestia, the only way to guarantee that data from the protocol can be read is to self-host a full node, or trust a SLA from an infrastructure provider. It is not trivial to guarantee retrieval as a Filecoin storage provider; the analogous setting in Filecoin would be to become a storage provider (requiring significant infrastructure cost) and successfully accept the same storage deal as a storage provider that was posted as a user, at which point one would be paying themselves to provide storage to themselves.

Latency Analysis

Latency on Filecoin is determined by several factors, such as network, topology, storage mining client configuration, and hardware capabilities. We provide a theoretical analysis which discusses these factors, and the performance that can be expected by our construct.

Due to the design of Filecoin’s proof system and lack of retrieval incentives, Filecoin is not optimized to provide high-performance round trip latency from the initial posting of data to the initial retrieval of data. High performance retrieval on Filecoin is an active area of research that is constantly changing as storage providers increase their capabilities and as Filecoin introduces new features. We define a “round trip” as the time from the submission of a data deal to the the earliest moment the data submitted to Filecoin can be downloaded.

Block Time In Filecoin’s Expected Consensus, data deals can be included within the block-time of 30 seconds. 1 hour is the typical time for confirmation of sensitive on-chain data (such as coin transfers).

Data Processing Data processing time varies widely between storage providers and configurations. The sealing process is designed to take 3 hours with standard storage mining hardware. Miners often outperform this 3 hour threshold via special client configurations, parallelization, and investing in more capable hardware. This variation also affects the duration of sector un-sealing, which can be circumvented altogether by quick retrieval options in Filecoin client implementations such as Lotus. The quick retrieval setting stores an unsealed copy of data alongside sealed data, significantly speeding up retrieval time. Based on this, we can assume a worst-case delay of three hours from the acceptance of a data deal to when the data is available on-chain.

Conclusion and Future Directions

This article explores building a DA by leveraging an existing DSN, Filecoin. We consider the requirements of a DA with respect to its role as a critical element of scaling infrastructure in Ethereum. We consider building on top of Filecoin for the viability of DA on a DSN, and use it to consider the opportunities that a solution on Filecoin would provide to the Ethereum ecosystem, or any that would benefit from a cost-effective DA layer.

Filecoin proves that a DSN can dramatically improve the efficiency of data storage in a distributed, blockchain-based system, with a proven saving of 100 million USD per 32 GB written at current market prices. Even though the demand for DA is not yet high enough to fill 32 GB sectors, the cost advantage of a DA still holds if empty sectors are sealed. Although current latency of storage and retrieval on Filecoin is not appropriate for the hot storage needs, storage miner-specific implementations can provide reasonable performance with data being available in under 3 hours.

The increased trust in Filecoin storage providers can be tuned via variable collateral, such as in EigenDA. Filecoin extends this tunabel security to allow for a number of replicas to be stored across the network, adding tunable byzantine tolerance. Guaranteed and performant data retrieval would need to be solved in order to robustly deter data withholding attacks, however like any other solution, the only way to truly guarantee retrievability is to self-host a node or trust infrastructure providers.

We see opportunities for DA in the further development of PoDSI, which could be used (alongside Filecoin’s current proofs) in place of DAS to guarantee data inclusion in a larger sealed sector. Depending on how this looks, this may make slow turnaround of data tolerable, as fraud proofs could be posted in a window of 1 day to 1 week, while DA could be guaranteed on demand. PoDSIs are still new and under heavy development, and so we make no implication yet on what an efficient PoDSI could look like, or the machinery needed to build a system around it. As there are solutions for compute on top of Filecoin data, the idea of a solution that computes a PoDSI on sealed or unsealed data may not be out of the realm of near-future possibilities.

As both the field of DA and Filecoin grows, new combinations of solutions and enabling technologies may enable new proof of concepts. As Solana’s integration with the Filecoin network shows, DSNs hold potential as a scaling technology. The cost of data storage on Filecoin provides an open opportunity with a large window of optimization. Although the challenges discussed in this article are presented in the context of enabling DA, their eventual solution will open a plethora of new tools and systems to be built beyond DA.

¹ Although this isn’t the construction of Filecoin, it is useful for those who are unfamiliar with programmable decentralized storage.

For more research pieces from Fenbushi Capital, check out their Medium page here.

To stay updated on the latest Filecoin happenings, follow the @Filecointldr handle.

Disclaimer: This information is for informational purposes only and is not intended to constitute investment, financial, legal, or other advice. This information is not an endorsement, offer, or recommendation to use any particular service, product, or application.

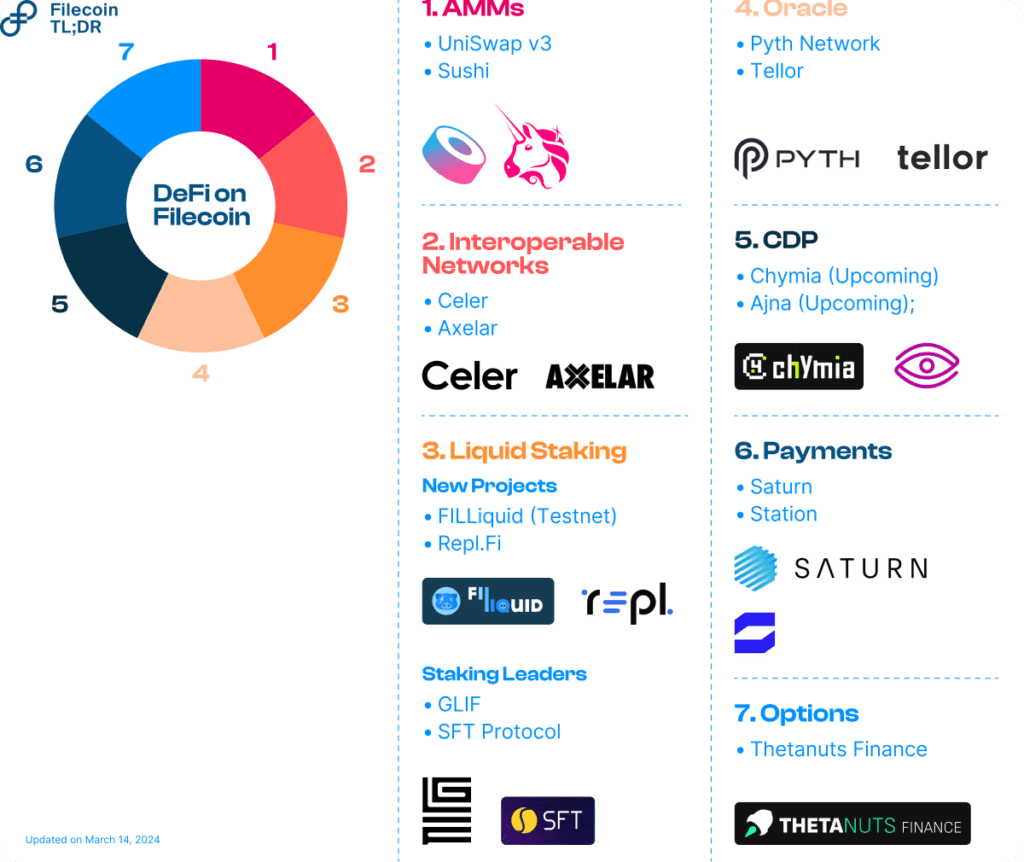

The Filecoin community celebrated the first anniversary of the Filecoin Virtual Machine (FVM) launch on March 14, 2024. The FVM has brought programmability to Filecoin’s verifiable storage and opened up a unique DeFi ecosystem anchored around improving on-chain collateral markets. Liquid Staking, for example, as a subset of Filecoin DeFi, has hit over $500 million in TVL. As the network grows, several critical infrastructures across AMMs, Bridges, Oracles, and Collateral Debt Positions (CDPs) are coming together to propel DeFi expansion in 2024.

In this blog post, let’s take a look at the latest DeFi projects launched on top of FVM and provide a view into future areas of activity.

DeFi Developments on FVM

Automated Market Makers

Automated Market Makers (AMMs) connect Filecoin with other Web3 ecosystems, enabling on-chain swaps, deeper liquidity, and fresh LP opportunities.

Decentralized Exchanges: ✅

Recently, leading Decentralized Exchanges Uniswap v3 (via Oku.trade) and Sushi integrated with Filecoin by deploying on the FVM. Oku Trade’s interface enables Uniswap users to easily exchange assets and provide liquidity on Filecoin. With this, FVM developers can effortlessly access bridged USDC and ETH assets natively on the Filecoin network, broadening Filecoin’s reach. As a foundational DeFi primitive, DEXes also opens the floodgates for non-native applications to leverage Filecoin’s robust storage and compute hardware.

Interoperability Networks

Bridges: ✅

Bridges help bring liquidity into DEXs and AMMs on FVM. For developers building on FVM, Bridges connects Filecoin’s verifiable data with tokens, users, and applications on any chain, ensuring maximum composability for DeFi protocols. For this purpose, messaging, and token bridging solutions by Axelar and Celer were added to the Filecoin network immediately post-FVM launch.

Today, AMMs Uniswap v3 and Sushi along with several other DeFi applications are natively bridged to Filecoin with the help of cross-chain infrastructure enabled by Axelar and Celer.

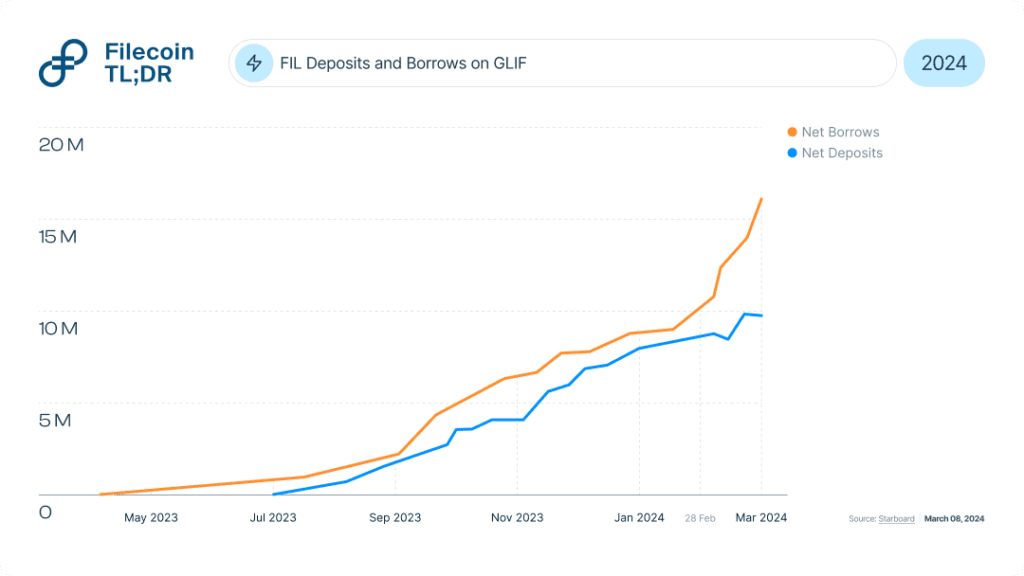

Liquid Staking

Liquid Staking protocols have been the prime mover within Filecoin DeFi. They’ve played a vital role in growing and improving on-chain collateral markets. Today, nearly 17% of the total locked collateral (approx. 30 million FIL) by storage providers comes from FVM-based protocols such as GLIF (52%), SFT Protocol (10%), Repl (9%) and the rest (29%). These protocols have increased capital access to storage providers while simultaneously enabling better yield access to token holders. Read more to learn how Filecoin staking works.

GLIF Points: 🔜

GLIF, the leading protocol on Filecoin, has a TVL of over $250 million. To put this into context, this surpasses the largest Liquid Staking protocols on L1 chains like Avalanche. As of writing this (March 06, 2024), 32% of all FIL stakes into GLIF liquidity pools were deposited shortly after its announcement to launch GLIF points (on Feb. 28, 2024), a likely precursor to a governance token.

Typically, to participate in the rewards program, GLIF users will have to deposit FIL and mint GLIF’s native token, iFIL. Similarly, the SFT protocollaunched a points program in 2023 based on its governance token to incentivize community participation.

Overall, we look forward to how the gameplay of points, popular among DApps in Web3 ecosystems, will act as a catalyst to decentralize governance and incentivize participation for Filecoin’s DeFi DApps.

New Staking Models: 👀

The influx of protocols experimenting with new models to inject liquidity into the ecosystem hasn’t slowed down. Two projects worth mentioning are Repl and FILLiquid.

Repl.fiintroduces the concept of “repledging.” Under repledging, SP’s pledged FIL are tokenized into pFIL, Repl’s native token, and used for other purposes including earning rewards. Repleding essentially increases the utility of locked assets thereby reducing opportunity costs for SPs. In just a few months after launch, Repl’s TVL has soared past $30 million.

FILLiquid, currently on testnet, models the business of FIL lending for SPs on algorithm-based fixed fees instead of traditional interest rates. The separation of payouts from the duration of deposits is expected to nudge long-term pledging and borrowing activities from token holders and SPs respectively, saving costs and increasing efficiency.

Price Oracles

Oracles, services that feed external data to smart contracts, are critical blockchain infrastructure essential for DeFi applications to grow and interact with the real world.

Pyth Network: ✅

Pyth recently launched its Price Feeds on the FVM. The integration allows FVM developers to access more than 400 real-time market data feeds while exploring opportunities to build on top of Filecoin’s storage layer. DeFi apps benefit from Pyth’s low-latency, high-fidelity financial data coming directly from global institutional participants such as exchanges, market makers, and trading firms.

Filecoin is also supported by Tellor, an optimistic oracle that gives FVM-based applications access to price feed data.

Collateralized Debt Positions

As DeFi activity on Filecoin is climbing, Collateralized Debt Positions (CDPs) will add more dimensions for other decentralized applications to build on FVM.

Chymia.Finance: 🔜

Chymia is an upcoming DeFi protocol on FVM. With a growing number of Liquid Staking Tokens (LST) on Filecoin, CDPs will extend the utility of locked tokens by generating stablecoins. Through Chymia, holders of LST can generate higher yields while using it as collateral for deeper liquidity.

Ajna: 🔜

Ajna is a noncustodial, peer-to-pool, permissionless lending, borrowing, and trading system requiring no governance or external price feed to function. As a result, any ERC20 on the FVM will be able to set up its own borrow or lend pools, making it easier for new developers to build a utility for their protocols.

Payments

Adjacent to storage offering on Filecoin, the FVM allows developers to bind DeFi payments to real-world primitives on the network. Built intuitively, Filecoin’s core economic flows enable paid services to settle on-chain. Station and Saturn are two notable Filecoin services to have successfully leveraged FVM for payments.

Filecoin Station: ✅

Station is a downloadable desktop application that uses idle computing resources on Station’s DePIN network to run small jobs. Participants in the network are rewarded with FIL earnings. Currently, Station operates the Spark and the Voyager modules, both aimed at improving retrievability on the network. In February, roughly 1,900 Station operators were rewarded with FIL for their participation.

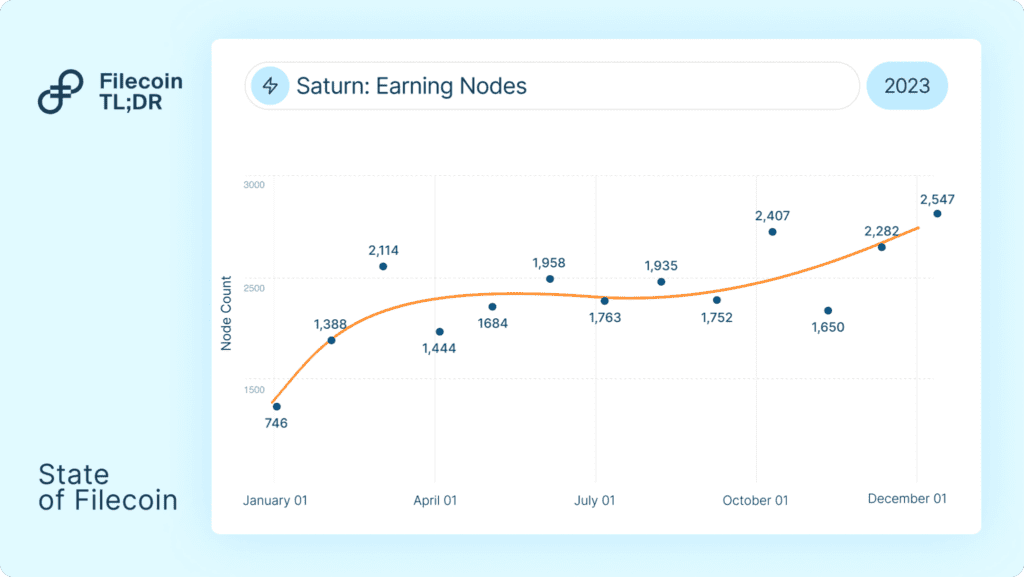

Filecoin Saturn: ✅

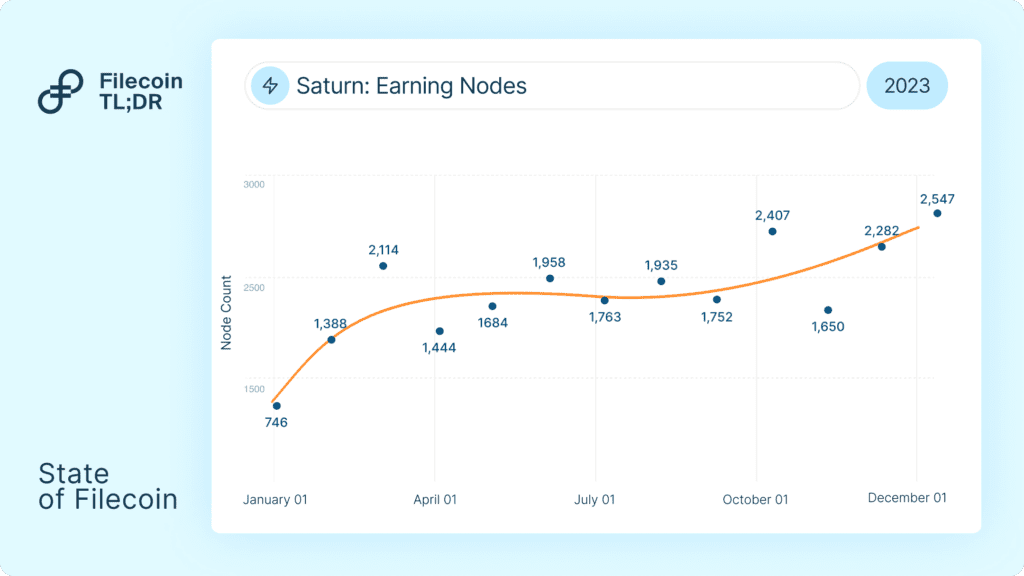

Saturn, a decentralized CDN network built on Filecoin, also leverages FVM for disbursing FIL payments to retrieval nodes on the network. In 2023, Saturn averaged over 2,000 earning nodes (retrieval providers on the network receiving FIL) for their services.

Decentralized Options

With growing liquidity, options are yet another emerging product in DeFi. Options facilitate the buying or selling of assets at a predetermined price on a future date, giving token holders protection against price volatility and an opportunity to speculate on market moves.

Thetanuts:✅

Currently, Thetanuts Finance, a decentralized on-chain options protocol supports Filecoin. The platform allows FIL holders to earn yield on their holdings via the covered call strategy. Thetanuts FIL-covered call vaults are cash-settled and work on a bi-weekly tenor.

Wallets

To use dApps on the FVM, users would be required to hold FIL in a f410 or 0x type wallet address. Over time, many Web3 wallets such as MetaMask, FoxWallet, and Brave have started supporting 0x/f410 addresses. MetaMask also supports Ledger. With this, it is possible to hold funds in a Ledger wallet and interact with FVM directly.

In addition, exchanges like Binance natively supporting the FEVM drastically reduce complexities for FVM builders. To learn more about the most recent wallet upgrades, visit the Filecoin TLDR webpage.

What’s Next?

The obvious near-term impact of various integrations across AMMs, Bridges, and CDPs is a fresh influx of liquidity into the Filecoin ecosystem. Liquidity begets deeper liquidity with an increase in the number and diversity of DeFi protocols on Filecoin. DeFi’s growing economy clubbed with more services coming on-chain and utilizing FVM for payments will overall increase the revenue and utility of the network. We expect this strong DeFi traction to scale Filecoin as an L1 ecosystem, with core services of storage and compute becoming the backbone of the decentralized internet.

To stay updated on the latest Filecoin happenings, follow the @Filecointldr handle.

Many thanks to HQ Han and Jonathan Victor for reviewing and providing valuable insights and to all the ecosystem partners and teams for their timely input.

Disclaimer: This information is for informational purposes only and is not intended to constitute investment, financial, legal, or other advice. This information is not an endorsement, offer, or recommendation to use any particular service, product, or application.

2023 marked significant shifts in technology and adoption for the Filecoin network. From the launch of the Filecoin Virtual Machine, to other developments across Retrievals and Compute, 2023 lay the foundation for Filecoin’s continued expansion. This blogpost will provide a summary of the notable milestones the Filecoin ecosystem reached in 2023, and in the later portion, growth drivers to watch for 2024.

TL;DR

2023 Retrospective:

Storage: Active deals reached 1,800 PiB, and storage utilization grew to 20%

FVM: FVM launch in March 2023 enabled FIL Lending (Staking) which supplied 11% of total collateral locked by Storage Providers; TVL broke USD 200M

Retrievals: Retrievability of Filecoin data improved, alongside notable releases from Saturn (3,000+ nodes, sub 60ms TTFB) and Station

Compute, AI and DePIN networks: Synergistic growth of Filecoin together with physical resource & compute networks

Web2 Enterprise Data Storage: Led by strengthened offerings by teams such as Banyan, Seal Storage, and Steeldome

Continued DeFi growth: DEXes, Oracles, CDPs, spurred by service revenue coming on-chain

2023 Retrospective

To recap, Filecoin enables open services for data, built on top of IPFS. While Filecoin initially focused on storage, its vision includes the infrastructure to store, distribute, and transform data. The State & Direction of Filecoin, Summarized blog post shared an initial framework for Filecoin’s key components. This framework will serve as an anchor for discussing 2023’s traction.

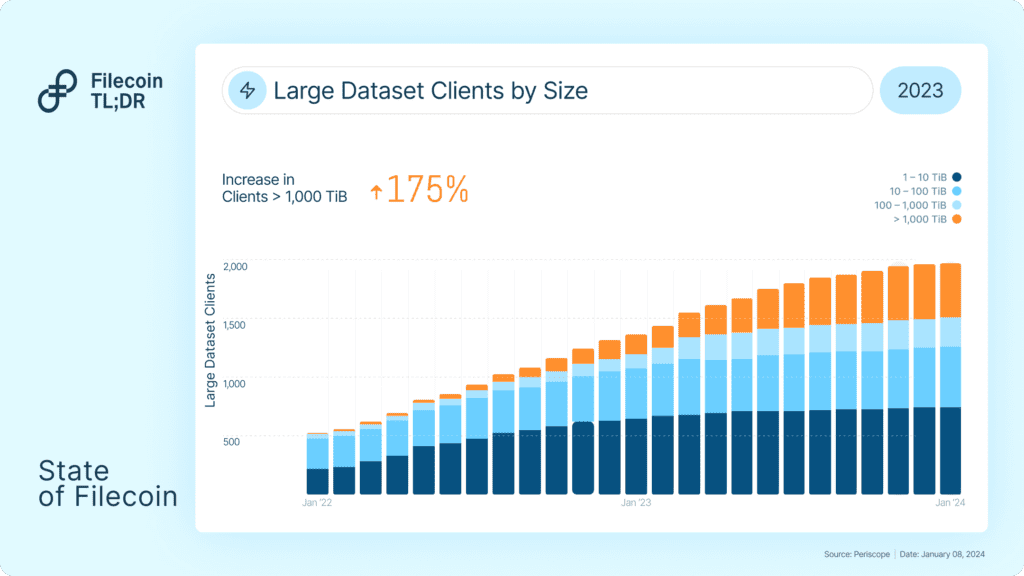

1) Storage Markets: Active storage deals reached 1,800 PiB with storage utilization of 20%

In 2023, Filecoin’s stored data volume grew dramatically to 1,800 PiB, marking a 3.8x increase from the start of the year. Storage utilization grew to 20% from 3%. Currently, Filecoin represents 99% market share of total data stored across decentralized storage protocols (Filecoin, Storj, Sia, and Arweave).

Growth in Active Storage Deals was driven by two factors:

1) Storing data was easier in 2023. Continued development across on-ramps such as Singularity.Storage, NFT.Storage, and Web3.Storage increased Web3 adoption. Singularity alone onboarded 180 plus clients and 270 PiB of data. This growth was enabled by advances in its S3 compatibility, data preparation, and deal making.

2) Large dataset clients grew exponentially in 2023. Over 1,800 large dataset clients onboarded datasets by the end of 2023, from an initial base of 500 plus clients. 37% of these clients onboarded datasets exceeding 100 TiB in storage size.

2) Retrievals: Greater reliability for Filecoin Retrievals, alongside releases from Saturn & Station

Filecoin’s retrieval capabilities were bolstered by improvements both in its tooling and offerings. Several teams, such as Titan, Banyan, Saturn and Station, are laying the groundwork for new use cases to be anchored into the Filecoin economy, including decentralized CDNs and hot storage.

Saturn: A Decentralized CDN

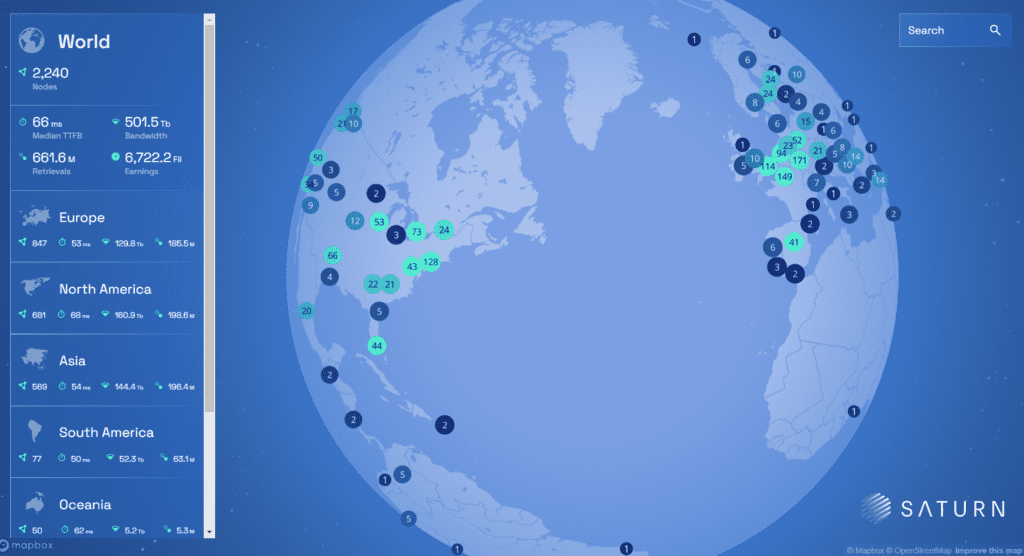

Saturn is a decentralized CDN network built on Filecoin, that seeks to address the need for application-level retrievals. The Saturn network currently has over 3,000 nodes distributed across the globe, enabling low-latency content regardless of location.

Distribution of Nodes: 35% in North America, 34% in Europe, 24% in Asia, 7% RoW Source: Saturn Explorer as of January 08, 2024

Across 2023, Saturn reduced its effective Time-to-First-Byte (median TTFB) to 60 milliseconds. This makes Saturn the fastest dCDN for content-addressable data, with TTFB remaining consistent across all geographies. Saturn was also capable of supporting 400 million retrieval requests on its busiest day of the year.

At the end of 2023, Saturn launched a private beta for customers (clients include Solana-based NFT platform Metaplex).

Station: A Deploy Target for Protocols (Enabling Spark Retrieval Checks)

Station, a desktop app for Filecoin, was launched in July 2023. Station is a deployment target for other protocols allowing DePIN networks, DA layers, and others to run on a distributed network of providers.

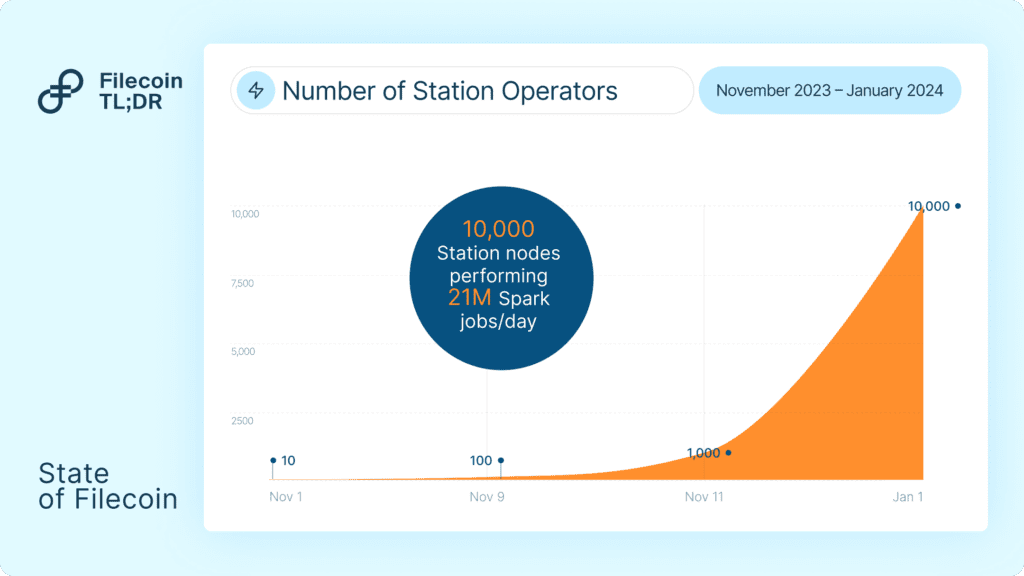

Station’s first module, Spark, is a protocol for performing retrieval checks on Storage Providers (SPs). Spark helps establish a reputational base for SP data retrievability, and supports teams looking to provide a hot storage cache for Filecoin. Since launch in Nov 2023, Spark has grown to 21 million daily jobs on 10,000 active nodes as of January 2024.

3) Filecoin Virtual Machine: The FVM launch introduced a new class of use cases for the Filecoin Network. Early DeFi adoption broke $200 million in TVL.

The Filecoin Virtual Machine (FVM) launched in March 2023 with the EVM being the first supported VM deployed on top. FVM brought Ethereum-style smart contracts to Filecoin, broadening the slate of services anchoring into Filecoin’s block space. Two areas of early adoption have been in liquid staking services (led by GLIF and other DeFi protocols) and micropayments via the FVM.

Liquid Staking

One of the core economic loops in the Filecoin economy is the process of pledging, where SPs put up collateral to secure capacity and data on the network. Prior to the FVM, borrowed Filecoin collateral was sourced through managed offerings from operators like Darma Capital, Anchorage, and CoinList. Post-FVM, roughly a dozen staking protocols have launched to grow Filecoin’s on-chain capital markets.

In aggregate, FVM-based protocols supply almost 11% of the total locked collateral (approx. 19 million FIL) on the network, giving yield access to token holders, and increasing the access to capital for hundreds of Filecoin SPs. From Filecoin’s collateral markets alone, the ecosystem has broken past 200 million in TVL.

Payments

Adjacent to the core storage offering on Filecoin, new services are being built that anchor into Filecoin’s block space. As mentioned in the Retrieval Markets section, two notable services (Station and Saturn) have actually started leveraging FVM for payments in 2023.

To date, Station users have completed 161 million jobs with more than 400 addresses receiving FIL rewards. Saturn averaged over 2,000 earning nodes in 2023 with 448,905 FIL disbursed to date.

4) Compute: Traction for Decentralized Compute Networks

Filecoin’s design enables compute networks to run synergistically on Filecoin’s Storage Providers. Sharing hardware with compute networks is also valuable to the Filecoin network: (1) sharing allows Filecoin to offer the cheapest storage by running side-by-side with compute operations, and (2) it brings additional revenue streams into the Filecoin economy.

Two key developments made running compute jobs on Filecoin nodes:

Sealing-as-a-service: Sealing-as-a-service is the process by which Storage Providers (SPs) can outsource production of sealed sectors to third-party marketplaces. This gives SPs greater flexibility in operations and reduces costs of sector production. One marketplace, Web3mine, has thousands of machines participating in its protocol offering cost savings to SPs of up to 70%. On top of the cost savings, the infrastructure built may also eventually benefit SPs by allowing them to leverage their GPUs for synergistic workloads (e.g. compute jobs)

Reduced Onboarding Costs:Supranational shipped proof optimizations reducing sealing server cost by 90% and overall cost of storage by 40%

On top of these developments, 2023 saw emerging compute protocols building in the Filecoin ecosystem. Two notable examples:

Distributed compute platform Bacalhau demonstrated real-world utility among Web2 and DeSci clients. Most recently, the U.S. Navy chose Bacalhau to assist them in deploying AI capabilities in undersea operations. Bacalhau is a platform agnostic compute platform intended to run on Web3 and Web2 infrastructure alike. Launched in November 2022, Bacalhau’s public network surpassed 1.5 million jobs and in some cases slashed compute costs by up to 99%

Source: Bacalhau

Up-and-coming compute networks likeIo.net allow ML engineers to access a distributed network of GPUs at a fractional cost of individual cloud providers. Io.net recently incorporated 1,500 GPUs from Filecoin SPs — positioning Filecoin providers to offer their services to Io.net’s customer base. Io.net has over 7,400 users since its launch in November 2023, serving 15,000 hours of compute to users.

2024 will be a critical growth year for Filecoin as groundwork laid in 2023 comes to fruition. Native improvements to storage markets, greater speed of retrievals, new levels of customizability & scalability brought by FVM and Interplanetary Consensus (IPC), all expand the universe of use cases that Filecoin can address.

In a Web3 climate where there is substantial attention on DePIN (and the tying of real world services with Web3 capabilities) these changes will be critical building blocks for even better services. Here are three themes to look for in 2024:

1) Synergies with Compute, AI and other DePIN networks

In 2024, foundational improvements to the network will substantially improve Filecoin’s ability to compose with other ecosystems.

Fast finality allows better cross-network interactions with app chains in other ecosystems (e.g. Cosmos, Ethereum, Solana).

Customizable subnets allow for novel types of networks to form on top of Filecoin such as general purpose compute subnets (e.g. Fluence) and storage pools (e.g. Seal Storage).

Hot storage allows for broader use case support including serving data assets for physical resource networks (e.g. WeatherXM/Tableland), caching data for compute networks (e.g. Bacalhau), and more.

This is all scratching the surface. As the Web3 space and DePIN category grows, Filecoin is well positioned to support new communities that form given its 9 EiB of network capacity and flexibility. There exists a sizable opportunity within physical resource networks producing high amounts of data, such as Hivemapper (over 100M km mapped), and Helium (1 million hotspots globally). Compute networks are also a likely growth area, given the backdrop of a GPU shortage (particularly for AI purposes) in traditional cloud markets.

Source: Messari

2) Focused Growth in Web2 Enterprise Data Storage

Web2 enterprise storage is a unique challenge for decentralized networks – requirements from these customers are not easily supported by most networks. Typical requirements from enterprise clients can include end-to-end encryption, certification for data centers, fast retrievals, access controls, S3 compatibility, and data provenance/compliance. Crucially, these requirements tend to differ across segments and verticals, which means that a level of adaptability is required. Filecoin’s architecture enables it to layer on support for the features these customers need.

A few teams worth keeping an eye on:

Banyan: Banyan simplifies how enterprise clients integrate with decentralized infrastructure by bundling hot storage, end-to-end encryption, and access controls, on top of a pool of high-performing storage providers. With the Filecoin network, Banyan provides content-addressable storage, which it plans to complement with hot storage proofs by utilizing FVM. This implementation makes Banyan compatible not only for enterprise, but DePIN and compute networks.

Seal: Seal has established itself as one of the best storage onramps in the Filecoin ecosystem, and is responsible for onboarding several key clients onto the network, such as UC Berkeley, Starling Labs, the Atlas Experiment, and the Casper Network. The team has been one of the driving forces in enterprise adoption to date, and most recently has achieved SOC 2 Compliance. In 2024, they plan on launching a subnet to enable a market for enterprise deals. On the back of their enterprise deal flow, they are positioned to bring petabytes of data into the network over the coming year via their new market.

Steeldome: Steeldome offers enterprise clients seeking data archival, backup and recovery with an alternative that is cost-competitive, efficiently deployed and scalable. It does so by combining Filecoin in its stack with Web2 technologies, allowing a fuller feature set to complement Filecoin’s cost-effective and secure archival storage. The Steeldome team has succeeded in onboarding clients across insurance, manufacturing, and media. In 2024, they plan to continue that trajectory, while offering a managed service for Storage Providers.

3) Greater On-chain DeFi activity

There is likely to be continued activity in the on-chain economy with an increase in the number and type of DeFi protocols on Filecoin.

The first protocols will increase service revenues (from Storage, to Retrievals, and Compute) coming on-chain. As previously described, more services are coming online in the Filecoin network, and are utilizing FVM for payments (e.g. Saturn, Station).

Key releases in 2023, including SushiSwap going live in Nov 2023, and the UniSwap community’s approval of integrating on FVM will lead to more diverse DeFi services coming on-chain. This will include CDPs (Collateralized Debt Positions), and Price Oracles (e.g. Pyth), among others.

Final Thoughts

In 2024, the Filecoin network will experience greater adoption, particularly by Compute, AI and DePIN networks, as well as targeted enterprise verticals. This adoption brings on-chain service revenue and supports the growth of DeFi activity beyond collateral markets. Continued improvements on storage markets, retrievability driven by hot storage proofs and CDN networks, as well as releases by FVM and IPC will enable the teams building on Filecoin to drive this next stage of growth.

To stay updated on the latest in DePIN and the Filecoin ecosystem, follow the @Filecointldr handle.

This blogpost is co-authored by Savan Chokkalingam and Nathaniel Kok on behalf of FilecoinTLDR. Many thanks to HQ Han and Jonathan Victor for reviewing and providing valuable insights and to all the ecosystem partners and teams for their timely input.

Disclaimer: This information is for informational purposes only and is not intended to constitute investment, financial, legal, or other advice. This information is not an endorsement, offer, or recommendation to use any particular service, product, or application.

Filecoin’s larger roadmap aims to turn cloud services into permissionless markets on which any provider can offer their services. The network started with Storage markets, with the Mainnet launch in October 2022. More recently, the Filecoin Virtual Machine (FVM) was introduced to bring smart contract functionality onto the network. This allows for user programmability around key services on the Filecoin network: which includes Large-scale Storage, and soon, Retrievals.

In this post, we dive into the Retrieval markets that Filecoin is developing and one of its lighthouse projects. We will cover the following topics:

Filecoin’s Retrieval Markets and the Retrieval Markets Working Group (RMWG)

Content Delivery Networks (CDNs) and the role of Project Saturn

Saturn’s approach to a decentralized CDN and its traction to date

What’s next for Saturn

Filecoin’s Retrieval Markets and the RMWG

As covered earlier in our previous post, Filecoin seeks to build open services for data, which consists of three main pillars (Storage, Retrieval, and Compute-over-Data). Storage has been a key emphasis for Filecoin from 2020 to 2022 — it has emerged as the largest decentralized storage network to date, with over 1,170 PiB of data stored, and 200,000+ users ranging from Opensea to the Internet Archive. The remaining pillars of Retrieval and Compute-over-Data have been in development since 2022, with working groups (open for any individual or entity to join) organized around building these markets. The working groups encourage modularity and often consist of different teams that tackle different pieces of the puzzle.

Key components of Filecoin’s roadmap for open data services

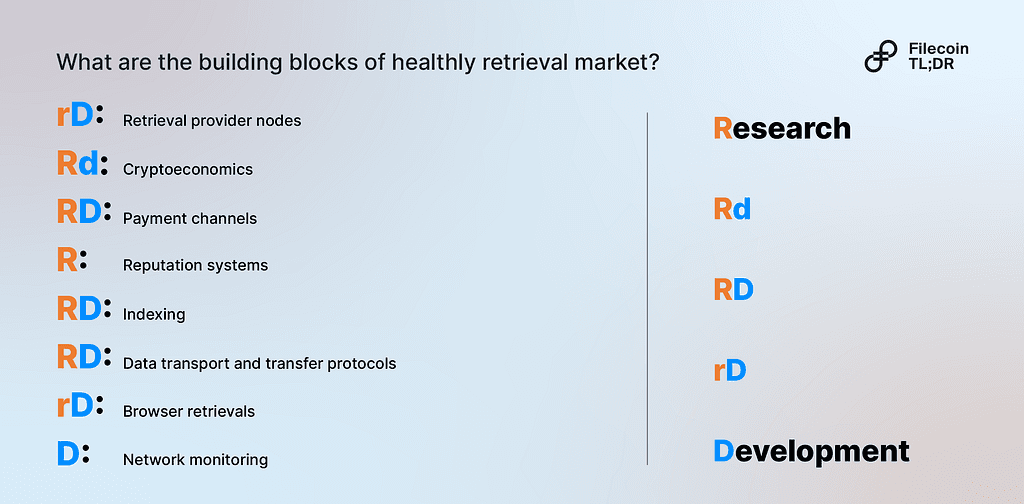

The Retrieval Market Working Group (RMWG) is centered around building a decentralized CDN (Content Delivery Network) for the Filecoin ecosystem. Over 15 teams (such as Magmo, Ken Labs, Protocol Labs, and more) are contributing to tackling technical challenges in the space, from enabling ultra-fast payments to data transfer protocol enhancements to crypto-economic models for data retrieval. The following are building blocks the RMWG has been organizing itself around since H1 2022 and is built off an envisioned retrieval flow that can interact freely with Filecoin’s storage markets.

Building blocks of a functional retrieval markets identified by the RMWG

Even in its R&D stage, projects in the RMWG are already serving 160 million daily retrieval requests and more than 2 PB of data per month. Collectively, these projects will seek to enable a decentralized CDN that can serve not just the web3 space, but the web2 market as well.

CDNs and the role of Project Saturn

Content delivery networks are a key part of the Internet’s infrastructure. Groups of servers work together to provide fast delivery of internet content, from static web pages to YouTube videos. Incumbent CDN providers include players such as Cloudflare, Akamai, and Fastfly. Businesses pay for these services instead of the end-user, which means that service consistency, coverage, and pricing are critical.

Content Delivery Networks today are highly centralized and dominated by big players

The CDN market today is highly centralized and dominated by a few big players. Only 7 CDN providers serve over 80% of market needs. This brings about sizable concentration risk in the event of network failures (e.g. CloudFlare outage in 2022), and higher latencies in regions far remote from the closest data centers (e.g. Africa).

A distributed model of smaller CDNs in various regions could effectively solve these problems, but economies of scale have prevented smaller, distributed CDNs from challenging incumbent providers (capital outlay could reach up to billions per year). Delivering web content better than incumbent providers will open up a significant commercial opportunity. The global CDN market size accounts for US 20Bn in 2022 and is expected to reach around 100Bn by 2032 (not counting new web3-based use cases such as NFTs). This is where Project Saturn comes in.

A web3 CDN can potentially overcome this challenge by allowing anyone to contribute resources for content retrieval (provided they fulfill minimum criteria) in a network. This shifts the burden from a single company to thousands (or more) of companies supporting the network, reducing barriers to entry. This is where Project Saturn comes in. Project Saturn is a decentralized CDN network built on Filecoin, that seeks to enable reliable, performant, and economic retrieval of content on the Internet. It is one of the key projects in the RMWG, with a public launch in November 2022. Saturn seeks to achieve the following:

Democratize the CDN market, by allowing anyone to serve as a Saturn node operator in return for crypto-incentives. Nodes can join in a permissionless manner, allowing for multiple companies or individuals to contribute towards a retrieval network (think franchising), which leads to a wider and more distributed footprint

Performant retrievals, with under 100ms TTFB, high network bandwidth, and low latency across all geographies, owing to a high density of nodes being distributed across each continent. While this does not exist today, it can potentially be achieved given a wider geographic distribution of nodes

No single point of failure unlike traditional CDN networks

Data integrity and authenticity by leveraging content-addressability. Project Saturn is the only decentralized CDN that is natively compatible with content-addressing

Saturn approach and traction to date (Aug 2023)

The data below is accurate as of August 2023, unless otherwise stated. Data for number of Active Nodes are accurate as of November 2023, owing to a upgrade in October 2023 that removed multi-noding behavior in the network, while keeping TTFB performance stable.

While Saturn’s ambition is to serve as a credible alternative to traditional CDN networks, its near-term goal is to effectively fulfill the billions of requests received each week for content-addressed data on Filecoin and IPFS. This is currently being fulfilled by IPFS Gateway, which serves as a key benchmark for Saturn as it improves its network capacity and performance.

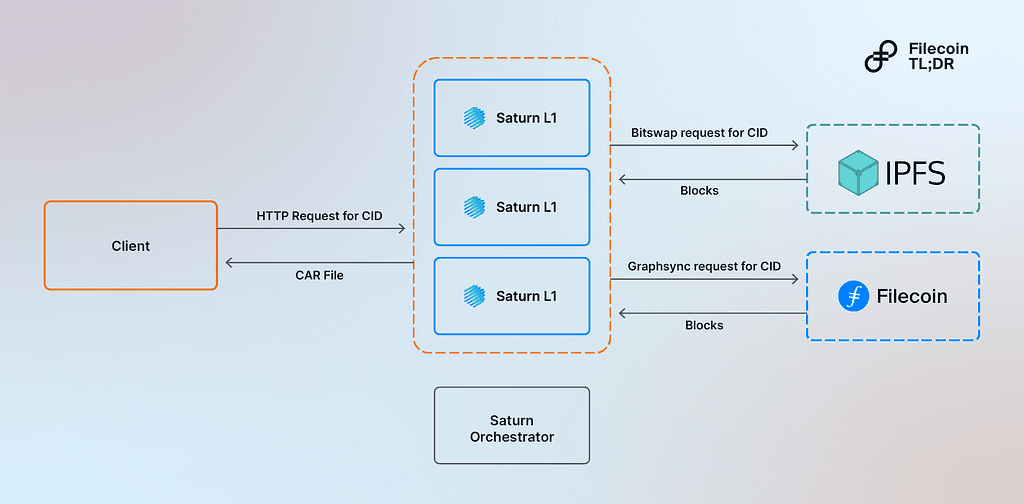

Flow chart for how network actors in Saturn enable retrievals from Filecoin and IPFS

Saturn’s approach involves four main network actors in enabling retrievals from Filecoin and IPFS:

Node operators offer their hardware and resources to the Saturn network by running Saturn nodes in different geo-locations around the world. They are rewarded based on how many bytes they serve to clients over each payment epoch. Saturn nodes join the network by registering with the Saturn Orchestrator. The network of Saturn L1s provides a huge geographically distributed cache of content-addressed data for Saturn clients

Saturn Orchestrator manages the membership of node operators in the Saturn Network and facilitates the payment process to these nodes. This is a key function in democratizing data retrievals while ensuring that qualified participants enter the market. Over time, the aim is for the orchestrator to run entirely on theFilecoin Virtual Machine (FVM)

Clients: Network users make requests for content from the Saturn network. The Client is the device used to make the request. Clients make HTTP requests to the Saturn network and get back CAR files, allowing clients to verify the file incrementally. When a Saturn L1 doesn’t have a file in its cache, it “cache-misses” to wherever the file is stored in either the IPFS Network or the Filecoin network, and returns it to the client

Customers use the Saturn Network as a CDN to accelerate their content to their users. Saturn customers can accelerate their content to a large number of Saturn nodes around the world to create a performant experience for end users

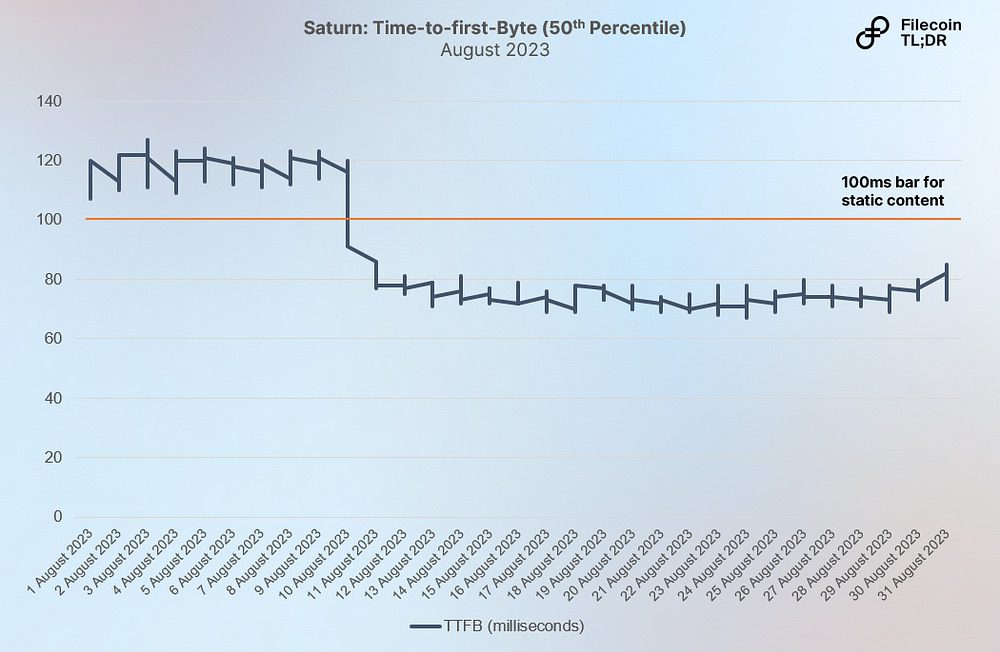

Significant developments have been made on Project Saturn to date. Following its public launch in November 2022, Saturn now has 80ms Time-to-first-byte (TTFB) at the 50th percentile, serves 30% of mirrored traffic from IPFS.io via the Bifrost Gateway, and has launched a verifiable node reward payout system on FVM.

It also has made significant headway in developing a network that is geographically diverse, capable of handling high-volume requests, and able to deliver content in a performant manner (low time-to-first byte). Since its public launch (just 8 months), Saturn has achieved:

Over 2,000 global points of presence (across 59 countries)

Capacity to serve 478 Million requests each day (in July 2023)

80 milliseconds time-to-first-byte (TTFB) for IPFS content

1) Over 2,200 retrieval providers worldwide (comparably distributed to traditional CDN providers)

Over 2,200 retrieval providers are currently on Saturn contributing to network bandwidth. This is a strong 11.8% MoM (month-on-month) growth, starting with only 662 nodes at the end of 2022. As a point of comparison, Filecoin’s storage markets grew by 21% MoM in its first 6 months, with approximately 3,500 storage providers on the network today (the largest in the web3 storage space)

This is comparably distributed to traditional CDN providers today. Akamai, the largest CDN globally, with a 35% market share, also has over 4,000 points of presence globally, while the next closest player (Alibaba) has only an estimated 2,800 points of presence (with the majority in China).

This speed of growth attests to the accessibility of serving as a retrieval provider on the Saturn network. It takes only 4 terabytes (TB) of storage and Saturn’s open-source software to run a Saturn CDN node (considerably less resource-intensive than being a storage provider on Filecoin). Saturn will allow more individuals to participate in Filecoin’s decentralized markets for data services.

Source: Saturn Explorer Nov 2023 (Explore Project Saturn’s live representation of nodes here)

Participation across geographies remains diverse: with the most nodes in Europe (800+), followed by North America (600+), and Asia (500+). Median TTFB remains consistently low across all continents, with Europe, Asia, Oceania, and South America experiencing sub-100 ms TTFB.

Distribution of these nodes is important, as it allows for the lowest possible distance between clients and nodes, translating to low latency for end-users (overcoming the speed of light problem experienced with traditional CDN providers). Saturn’s permissionless and crypto-incentivized attributes allow for a more ‘elastic’ supply to match with fast demand growth in developing regions like Asia and Africa, which are currently experiencing those latency issues today.

2) Saturn served an average of ~10.3 Billion requests monthly across 2023

Saturn has a network capacity of around 25+ terabits per second (approximately 10% of the network capacity of Cloudflare). An average of 10.3 Billion requests are served monthly across 2023, with 3.7 Million Gigabytes of monthly bandwidth served. Over 478 million daily requests were being handled as of the end of July 2023, which is close to 50% of IPFS Gateway’s daily requests in the same time frame. Despite its progress thus far, there remains room for stabilization in Saturn’s network capacity.

Source: Project Saturn data

3) Time-to-first-Byte is already under 80 milliseconds

Speed is an area where Saturn has shown significant results; the median TTFB (time-to-first-byte) is already under 80 milliseconds. Typically, a good TTFB lies below 100 ms for static content, and 200–500 ms for dynamic content. Saturn today is already the fastest content-addressable CDN globally with 80 ms TTFB and has further headroom for improvement as the network continues to become denser. Aside from Saturn, there also exist parallel developments to drive improved retrieval performance in the Filecoin network. This includes projects such as Rhea, which is seeking to optimize IPFS Gateway performance.

Source: Project Saturn data

What’s next for Saturn

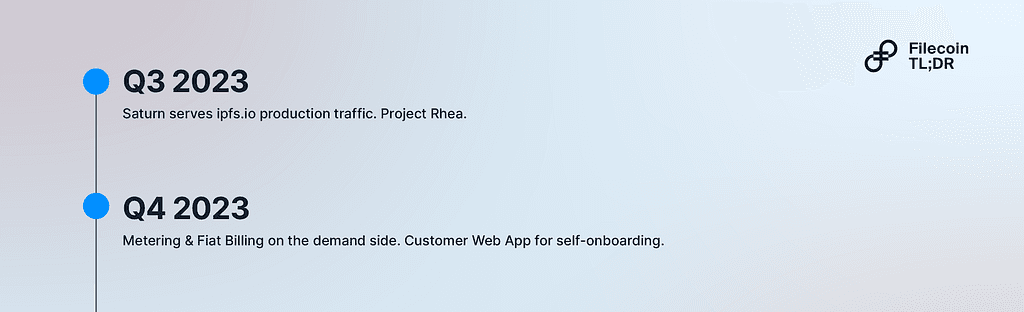

Since its public launch, Saturn has achieved significant progress as an open-source, community-run CDN network. Moving forward, the team looks to continue pushing towards better TTFB speeds, while improving performance correctness and latency. Towards the end of 2023, Saturn looks to achieve further milestones. These include serving 100% of IPFS.io traffic, implementing metering and billing on the customer demand side, and launching a web app to enable customer self-onboarding who want to accelerate content with Saturn.

Upcoming milestones in Project Saturn’s roadmap

You can keep up to date with Project Saturn, and other projects within the RMWG here. Data in this post is accurate as of 31st August 2023 unless otherwise stated.

Many thanks to the amazing HQ Han, Jonathan Victor, Alexander Kintsler, and the Project Saturn team for their input in publishing this piece.

Disclaimer: This information is for informational purposes only and is not intended to constitute investment, financial, legal, or other advice. This information is not an endorsement, offer, or recommendation to use any particular service, product, or application.

Editor’s Note: This blog is a repost of original content from IOSG Ventures. IOSG Ventures is a community-friendly and research-driven early-stage venture firm. This blog post represents the independent views of the author, who has given permission for re-publication.

The programmable layer on FIL, the FVM, allows for trustless marketplaces to be built

This calls for a need for a marketplace that currently exists off-chain, i.e. FIL borrowing to be brought on-chain, where FIL token holders lease their FIL to Storage Providers (which some call “miners”) who borrow FIL from the pool(s)

FIL borrowing is essentially taking cash forward on the future block rewards accrued by the Storage Providers, and this makes FIL block rewards from data storage more capital-efficient

There are obvious trade-offs to be made between centralization-capital efficiency- and security in protocol design

The market size for borrowing FIL is reducing over time but the introduction of stablecoins, etc. Can unlock unique projects to be built on top of these protocols

The launch of a programmability layer on a seasoned blockchain generally comes with a lot of excitement. The launch of Stacks (STX) on the Bitcoin blockchain brought a new paradigm of thinking amongst the community built around it.

A very similar narrative happened with the launch of the FVM on Filecoin. The robust Filecoin community now has to see its vision through a completely different lens. A lot of open problems that the ecosystem had could now be addressed. Creating trustless marketplaces via programmability was a key piece of the puzzle.

Liquid staking on Filecoin was the first “Request-for-build” from the Filecoin ecosystem during the launch of FVM and was given high importance. To understand why this is, let us first understand how the economics of Filecoin work.

How Filecoin Incentives Work

Unlike an Ethereum validator, there is no one-time staking in Filecoin. Every time a Storage Provider (SP) provides services, they need to put up a pledge amount in FIL. This pledge is required to seal the sectors and store the sealed sector in the SP. Such a structure ensures that the SP is going to store data for their clients for the period of the deal that they agree to, in exchange for rewards. Rewards are distributed via PoSt (Proof of Space-Time), where the SPs are rewarded for proving that they have the right client data stored.

SPs are selected via a leader selection mechanism called DRAND. DRAND chooses the leader with some initial requirements and also the % of raw byte power of the network controlled by the SPs.

SPs will have to keep ramping up raw byte power (RBP) to be chosen as the leader to “mine” a block and receive incentives. This helps the SP subsidize their storage costs.

Although there are many more factors that govern the supply rate of these incentives, the baseline is that for storage providers/miners, to maximize their bottom line will have to try to maximize RBP and onboard (and renew) more deals.

This creates a positive loop for the Filecoin network

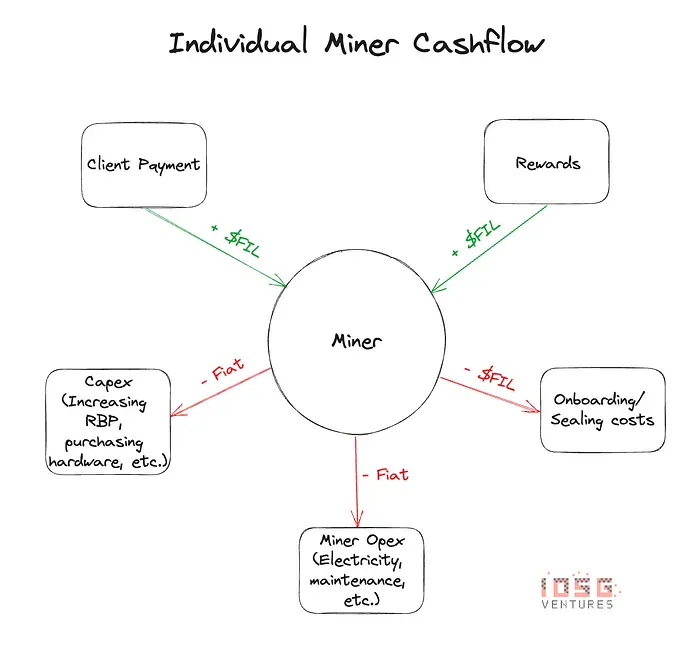

Economics of a Storage Provider

When an SP receives block rewards, these rewards are not liquid. Only 25% of the rewards are liquid, and the remaining 75% of the block rewards vest linearly over 180 days (~ 6 months). This poses a problem for SPs. The rewards, which are supposed to be an SP’s operating income, are now delayed payments for as long as the SP onboards/renews deals.

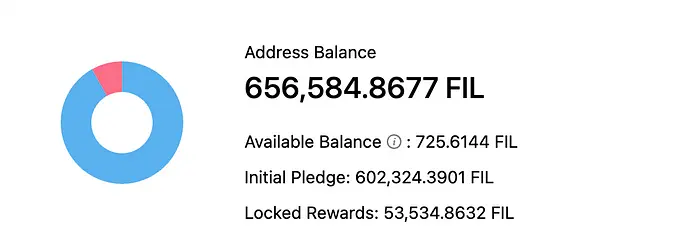

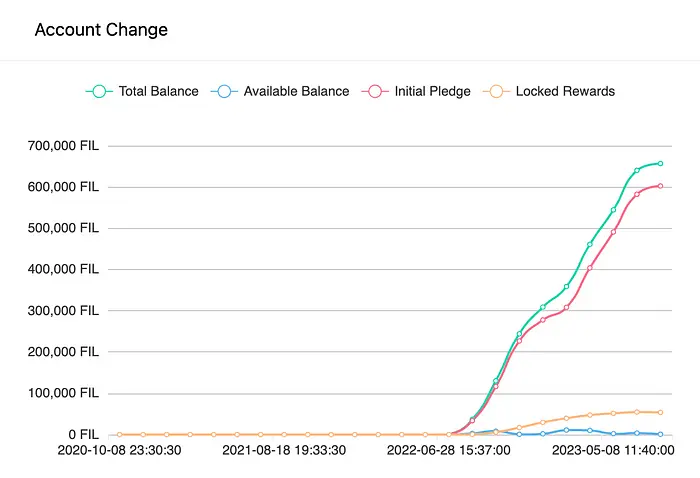

Let us look at the SP balance of the top miner in the network (as of 6th August 2023)

When you look at the graph, one can see that only about 1% of the rewards (or operating income) of the SP is actually liquid. If this SP now wants to either:

Pay for operating income

Upgrade hardware

Pay for maintenance

Or onboard/ renew deals

The SP will have to either borrow fiat currency or borrow FIL from third parties just to make up for these “delayed” payments.

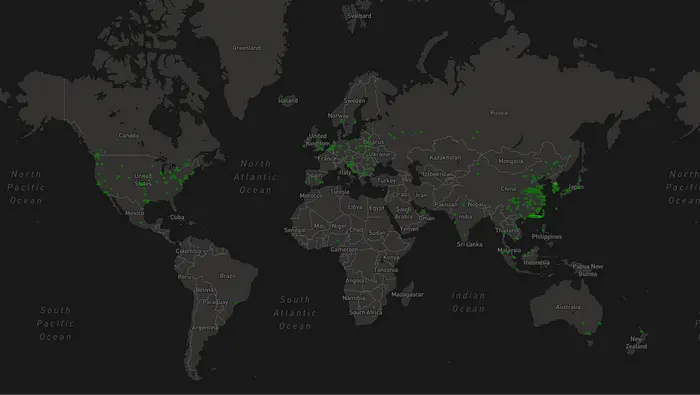

At the moment many storage providers (miners) in the network rely on CeFi lenders such as DARMA Capital, Coinlist, and a few others. As these are loan products, storage providers will have to go through KYC and a strict audit process to be able to borrow FIL. When we look at the map below, we can see a very high concentration of Filecoin SPs in Asia, and with centralized providers being mostly in the West, it is very hard for them to underwrite FIL loans to Asian miners with favorable terms, and most Asian miners/ SPs don’t have access to such providers.

This becomes a hindrance for new SPs to come in and participate in the system, and existing SPs can scale their business only as much as the total FIL pool size of these CeFi lenders

So why not just borrow fiat currency from a bank? With FIL being a volatile asset, it will pose additional capital management challenges for SPs who borrow.

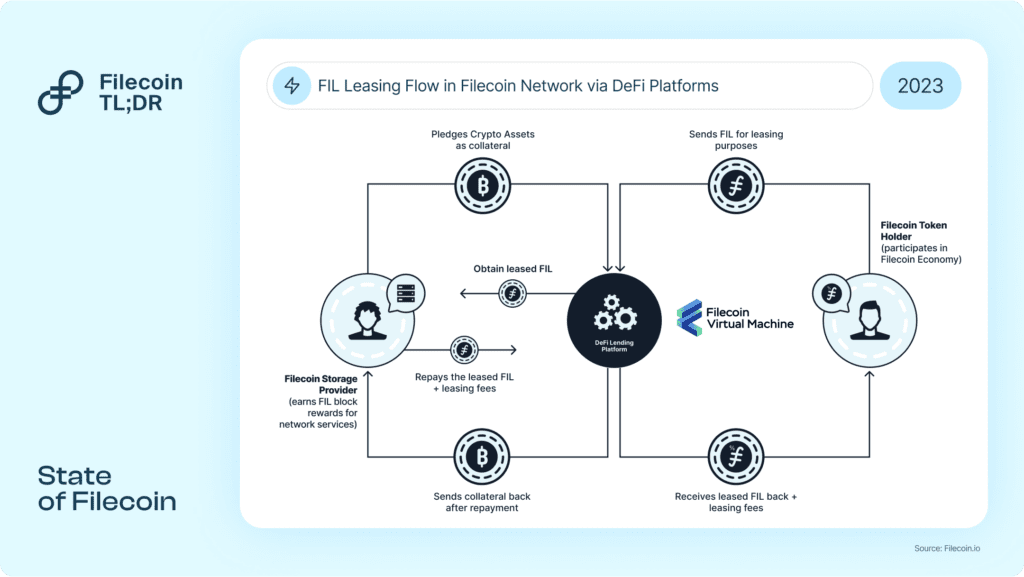

To solve this problem, there needs to be a marketplace for FIL lenders (who could be holders of FIL) and FIL borrowers (SPs)

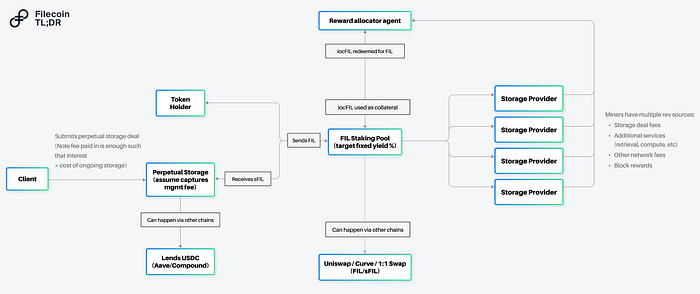

Filecoin Staking